|

|

|

|

|||||

|

|

|

Realty Income O has long been a cornerstone in the real estate investment trust (REIT) sector, known for its resilience and firm commitment to dividend growth. With a portfolio of more than 15,600 properties spanning the United States and Europe, the company has built a reputation as “The Monthly Dividend Company”. For income-focused investors, Realty Income often represents stability in an uncertain world.

Moreover, after holding the interest rates at the current level for several months, of late, there are anticipations in the market for a rate cut in the upcoming September FOMC meeting, with risks to the labor market increasing versus inflation. This shift has prompted a renewed focus on income-generating assets such as REITs, which tend to benefit from lower borrowing costs and improved relative yield appeal when Treasury rates decline.

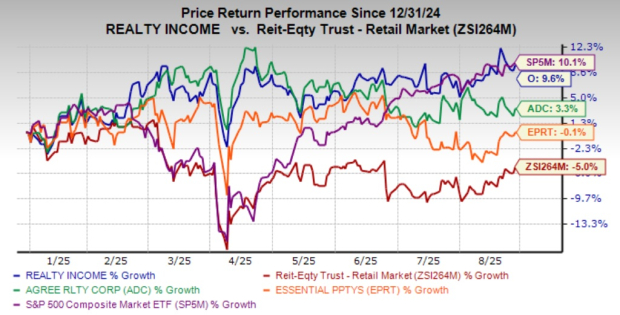

With a current yield of 5.51%, Realty Income outpaces peers like Agree Realty Corporation ADC at 4.22% and Essential Properties Realty Trust, Inc. EPRT at 3.84%. Check Realty Income’s dividend history here.

Year to date, Realty Income stock has climbed more than 9%, outperforming stocks like Agree Realty and Essential Properties Realty Trust, as well as the Zacks REIT and Equity Trust - Retail industry. However, it slightly trailed the broader S&P 500 composite.

Yet, the question remains: amid macroeconomic headwinds, is Realty Income stock best positioned as a buy, hold or sell? To answer that, let us weigh its second-quarter 2025 results, dividend reliability and growth strategy against the broader interest rate environment.

For the second quarter of 2025, Realty Income delivered steady results despite a challenging economic backdrop. Portfolio occupancy held firm at 98.6%, a testament to the defensive nature of its triple net lease model. AFFO per share covered the dividend comfortably, and management reaffirmed its full-year outlook. Leasing activity remained solid, underpinned by essential retail categories such as convenience, grocery and discount stores.

The company also emphasized its disciplined capital allocation, selectively pursuing acquisitions while maintaining balance sheet strength. With single-A credit ratings (A3/A-), net debt-to-EBITDA of 5.5X and an average debt maturity of 6.4 years, Realty Income has ample flexibility to weather the current environment and capitalize on opportunities once borrowing costs ease.

Realty Income has expanded far beyond its traditional retail roots. In recent years, it has entered industrial, gaming and data centers while expanding internationally into the U.K. and continental Europe. These moves have significantly widened its addressable market to roughly $14 trillion, leaving substantial room for growth.

Notable investments like Encore Boston Harbor and Bellagio Las Vegas, along with its collaboration with Digital Realty to invest in data centers, signal the company’s intent to tap into sectors with strong long-term growth potential. The company achieved record sourcing activity in the second quarter at $43 billion, matching all of 2024’s total volume. Despite the surge, Realty Income remained highly selective, closing on just 2.7% of deals.

The most compelling reason investors hold Realty Income remains its dividend. The company has paid 661 consecutive monthly dividends and increased its payout for 30 straight years, cementing its status as an S&P 500 Dividend Aristocrat. The current annualized dividend of $3.228 per share equates to a yield of around 5.5%.

Even more impressive is Realty Income’s consistency through cycles. From the dot-com bust and global financial crisis to the pandemic, the company has maintained positive operational returns each year since going public in 1994. This resilience reflects both the stability of its tenants and the strength of its long-term lease structure. Its compound annual dividend growth rate since its NYSE Listing is 4.2%.

As with most REITs, interest rates are the critical swing factor for Realty Income. Rising rates diminish the relative appeal of its dividend yield. Now, with the Fed Chair opening doors for rate cuts, sentiment toward REITs seems to be improving.

Lower borrowing costs benefit Realty Income by making acquisitions more accretive and enhancing dividend sustainability. At the same time, a lower-rate environment would make its dividend yield more attractive compared to Treasuries.

That said, investors must temper expectations. While rate cuts are a tailwind, they may not spark outsized near-term AFFO growth, given economic uncertainty and tight acquisition spreads.

Moreover, while management has increased its 2025 investment volume guidance to approximately $5 billion and raised the low end of its AFFO per share guidance ($4.24-$4.28 compared with $4.22-$4.28 guided earlier), its outlook incorporates 75 basis points of potential rent loss, higher than its historical experience. A significant portion of this credit loss stems from tenants brought in through M&A deals the company has completed in recent years.

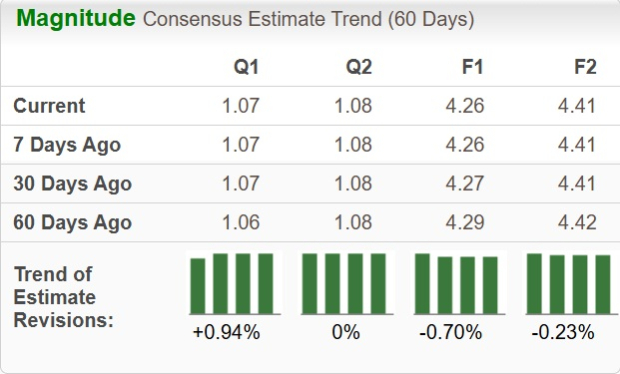

Estimate revisions reflect a somewhat mixed trend. While consensus estimates for the third-quarter adjusted funds from operations (AFFO) per share have climbed up marginally over the past two months, the same for full-year 2025 and 2026 have declined marginally over the same time frame.

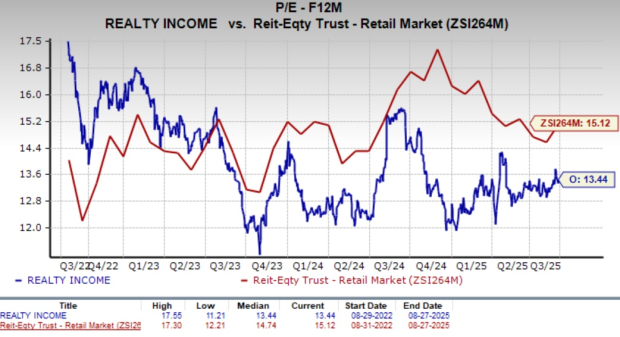

Realty Income stock is trading at a forward 12-month price-to-FFO of 13.44X, below the retail REIT industry average of 15.12X and on par with its three-year median. O stock is also currently trading at a reasonable discount compared to its industry peers, Agree Realty Corporation and Essential Properties Realty Trust. This valuation disparity might not be as favorable as it seems. Agree Realty is trading at a forward 12-month price-to-FFO of 16.43X, while EPRT is trading at 15.62X.

Realty Income’s appeal rests on three pillars: stability, income and disciplined growth. With a diversified tenant base, fortress balance sheet and solid track record of monthly dividends, it remains one of the most dependable REITs in the market. Its exposure to essential service tenants and investment-grade balance sheet offers a solid foundation for long-term income stability. Expansion into new sectors and geographies broadens its long-term growth runway, while potential Fed rate cuts provide a near-term catalyst.

However, given its fair valuation and moderate growth outlook, Realty Income does not currently stand out as a strong buy opportunity, nor does its consistent dividend and defensive profile make it a sell candidate. As such, Realty Income is best viewed as a hold — an anchor for income-oriented portfolios but not a source of outsized capital gains in the near term.

At present, Realty Income carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-07 | |

| Jul-01 | |

| Jul-01 | |

| Jun-30 | |

| Jun-30 | |

| Jun-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite