|

|

|

|

|||||

|

|

|

Investors are showing growing interest in the rapidly expanding structural heart device market, which is expected to witness a compound annual growth rate (CAGR) of 13.5% between 2025 and 2033, according to Grand View Research. Abbott Laboratories ABT and Edwards Lifesciences EW are two key players with significant presence in this sector.

Abbott’s Structural Heart segment focuses on delivering transcatheter and surgical devices like MitraClip for mitral regurgitation, TriClip for tricuspid regurgitation, and the Amplatzer portfolio for congenital heart defects and left atrial appendage closure. Edwards specializes in structural heart therapies, with a primary focus on transcatheter and surgical heart valve solutions like SAPIEN 3 Ultra RESILIA, Pascal and EVOQUE systems.

Given market growth driven by sedentary lifestyles, rising obesity, and the increasing prevalence of valvular heart diseases, which of these two stocks is the better investment opportunity right now? Let us dive into the details.

Abbott’s Structural Heart second-quarter sales grew 12% year over year, led by a combination of continued share gains in TAVR and strong adoption of TriClip. Amulet and MitraClip also contributed to this growth. The company is currently pursuing a label expansion to increase the addressable market. Accordingly, it launched a next-gen version of MitraClip that further enhances the procedure with improved deployment and deliverability. Furthermore, the company achieved FDA approval for the Tendyne mitral replacement valve, which offers a new treatment option for those who are not candidates for open-heart surgery or a mitral valve repair procedure.

Beyond structural heart, Abbott’s Nutrition business has consistently demonstrated strong growth and market share gains. The segment benefits from strong demand for Ensure and Glucerna, its market-leading brands that support complete and balanced nutrition and help manage dietary requirements for people with diabetes. Within Pediatric Nutrition, Abbott enjoyed continued strength in the United States, where the Similac brand remains the top choice for American parents.

Operationally, the company experienced a gross profit increase of 8.9% year over year, despite a 5.4% increase in the cost of products sold, further leading to a gross margin expansion of 79 bps. Also, from a solvency viewpoint, Abbott looks quite comfortable. It ended the second quarter with cash and cash equivalents of $7.28 billion, much higher than the short-term debt of $507 million. The debt to capital ratio was 20.9%, down 0.3% sequentially, highlighting the company’s financial stability.

Edwards’ structural heart segment benefits from strong clinical evidence, ongoing innovation and increasing adoption of minimally invasive procedures worldwide. The adoption of differentiated PASCAL technology (for patients with degenerative mitral regurgitation) is expanding in both new and existing sites worldwide. Meanwhile, the company is making strides with the EVOQUE (first transcatheter tricuspid valve replacement system) commercial rollout, successfully activating new sites in both the United States and Europe. Recently, at the New York valve conference, results from a real-world 176-patient study in Europe demonstrated excellent clinical outcomes for the EVOQUE system.

Per the latest development, in May, the company received FDA approval for its SAPIEN 3 platform for severe aortic stenosis (AS) patients without symptoms, marking the first FDA approval for TAVR in asymptomatic patients. Following the CE Mark for Alterra system for congenital heart patients, Edwards is rolling out this therapy in Europe, and initial feedback from clinicians has been positive.

In the second quarter, the surgical structure heart segment grew 7.7% from the prior-year level, driven by strong global adoption of Edwards’ premium resilient technologies, including INSPIRIS, MITRIS and KONECT. Edwards has been continuously generating evidence to expand the RESILIA portfolio. In line with this, in April, the company shared eight-year data, demonstrating the durability of the RESILIA tissue bioprosthetic valves at the Heart Valve Society meeting.

Operationally, the company experienced both gross and operating margin contraction during the quarter, due to dull macroeconomic trends worldwide. However, Edwards had a solid balance sheet position with cash and cash equivalents of $3.00 billion, which remained flat sequentially. Total debt amounted to $600 million, in line with the previous quarter’s level.

Year to date, Abbott’s shares have risen 16.1%. Meanwhile, Edwards has seen a much slower uptick, with shares gaining 9.8%.

Image Source: Zacks Investment Research

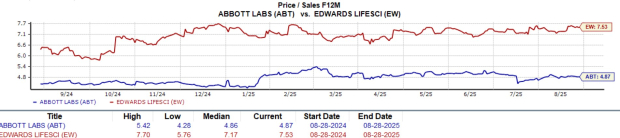

In terms of forward five-year price-to-sales (P/S), Abbott stock is trading at 4.87X, lower than Edwards’ P/S of 7.53X. When compared to the broader Medical sector average of 5.04X, Abbott appears to be appealing, and it has a Value score of C at present. Edwards, meanwhile, carries a Value Score of D.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Abbott’s 2025 EPS has remained unchanged in the past 30 days. The consensus mark implies 10.3% year-over-year growth.

Image Source: Zacks Investment Research

Meanwhile, Edwards' 2025 EPS has also remained unchanged in the past 30 days. The consensus mark implies 2.5% year-over-year growth.

Image Source: Zacks Investment Research

Abbott, carrying a Zacks Rank #3 (Hold) at present, continues to drive growth through expanding global adoption of MitraClip and new product launches addressing unmet clinical needs in complex structural heart interventions. Additionally, it benefits from the Nutrition business, with the adult segment leading growth. Despite mounting costs, its strong operational results reflect confidence in sustained growth.

Meanwhile, Edwards, carrying a Zacks Rank #3 at present, benefits from strong clinical evidence, ongoing innovation and increasing adoption of minimally invasive procedures worldwide. However, the company faced macroeconomic pressure, which caused its margins to contract. On a positive note, it has a strong solvency.

Although both Abbott and Edwards’ earnings estimates have remained unchanged, ABT stock has fared comparatively better than EW in the year-to-date period. This supports the case for retaining ABT stock in one’s portfolio. ABT’s discounted P/S relative to both EW and the industry point may continue to attract value-focused investors.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-07 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite