|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Avis Budget Group CAR shares have risen more than +20% over the last week as President Trump’s 25% tariffs on all imported vehicles are likely to boost the fleet value for the leading rental car operator.

The implied pricing leverage Avis will have for its rental car services has also led to positive investor sentiment.

Known for its massive earnings potential, let’s see if the rebound in Avis stock can continue or if it’s time to fade the recent rally.

Despite a sharp rebound off its 52-week lows of $54 a share in March, Avis stock is still 43% from its one-year peak of over $130 last May. Seeing as rental car operations tend to be cyclical based on seasonal demand, a string of three consecutive quarterly earnings misses had led to the sharp decline in CAR shares which is illustrated by the red arrows in the Price, Consensus and EPS surprise chart below.

Although Avis has missed bottom-line expectations in three of its last four quarterly reports, the company most recently surpassed Q4 EPS estimates in February, posting an adjusted loss of -$0.23 a share compared to estimates of -$0.96.

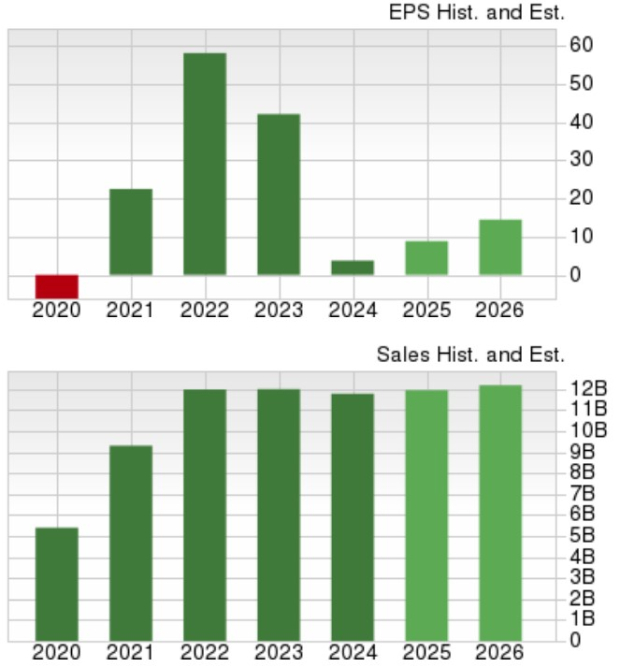

Reassuringly, Avis's annual earnings are expected to rebound and soar to $8.84 per share this year, versus EPS of $3.74 in fiscal 2024. This comes as Avis had a one-time non-cash impairment of $2.3 billion last year and additional non-cash charges of $180 million which was attributed to a strategic decision to accelerate its fleet rotations by purchasing new vehicles.

The move is aimed at improving long-term operational efficiency and reducing fleet costs in the future with Avis’s EPS projected to soar another 63% in FY26 to $14.47. However, it’s noteworthy that FY25 and FY26 EPS estimates have declined over the last 60 days.

On the top line, Avis’s total sales are currently slated to rise 1% in FY25 and are projected to increase another 2% in FY26 to $12.2 Billion.

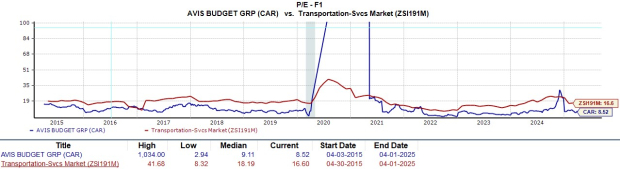

At current levels, CAR trades at just 8.7X forward earnings. This is a significant discount to its Zacks Transportation-Services Industry average of 16.5X with some of the other notable companies in the space being C.H. Robinson Worldwide CHRW, REV Group REVG, and Hertz Global HTZ.

It’s noteworthy that Hertz isn’t profitable so P/E valuation can’t be used in comparison to its rental car competitor. That said, like Hertz, Avis trades at less than 1X sales which is on par with the industry average.

Undoubtedly, Avis stock is attractive to long-term investors under $100 a share but there could be better buying opportunities ahead. To that point, if EPS estimates continue to decline it may be time to fade the recent rally as this could likely lead to more downside risk in CAR shares and a sell rating despite Avis's attractive valuation.

That said, an uptick in EPS revisions could lead to a buy rating and is plausible if imported vehicle tariffs start to show a positive impact on the company’s operations and fleet value. For now, Avis stock lands a Zacks Rank #3 (Hold).

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite