|

|

|

|

|||||

|

|

|

Tutor Perini Corporation TPC has long been recognized for its strength in large, complex infrastructure projects. The ongoing benefits from federal infrastructure legislation are expected to drive multi-year demand for projects across the construction and infrastructure sector. Underlying these market trends, the company’s Civil segment remains the bright spot, with robust backlog growth in transportation and infrastructure projects.

TPC’s shift toward higher-margin civil works offers better visibility on revenues over multiyear timeframes, with robust federal and state infrastructure funding offering the civil pipeline to capture additional high-value work in the upcoming term. During the second quarter of 2025, the company highlighted that its Civil segment’s (accounting for 51.8% of the total revenues in the first half of 2025) revenues of $1.43 billion were the highest ever in the first half of 2025, growing 32.3% year over year. Moreover, this segment’s backlog as of June 30, 2025, increased 155.9% year over year to $11.17 billion. During the second quarter, TPC won two civil works projects in the Midwest, having a total value of $127 million and $90 million worth of additional funding for a mass transit project in California.

Given the backlog growth and position, Tutor Perini will be able to expand its earnings growth and scale margins if it can effectively convert its sizable backlog into higher-margin revenues and accelerate claim resolutions. Although execution risks are concerning, TPC’s focus shift on high-margin civil projects, backed by market tailwinds, is expected to support its prospects in the near and long term.

Owing to the favorable industry backdrop, TPC once again raised its 2025 GAAP earnings per share (EPS) guidance in the range of $1.70-$2.00 (up from the previous range of $1.60-$1.95), with adjusted EPS expected in the range of $3.65-$3.95 (up from $2.45-$2.80). Besides, the company is optimistic that its GAAP and adjusted EPS in 2026 and 2027 will be more than the upper end of the 2025 renewed guidance.

For 2025 and 2026, TPC’s earnings estimates have trended upward in the past 30 days by 106.6% and 28.9%, respectively. The revised estimated figures for 2025 and 2026 imply year-over-year growth of a whopping 220.8% and 4.9%, respectively.

The analysts’ sentiments are likely to have been bullish for TPC, attributable to increased public infrastructure demand and its ability to capture those opportunities in its favor, driving its backlog.

Rising U.S. infrastructure funding is faring well for other key market players, including Fluor Corp. FLR and Granite Construction Incorporated GVA, which shares space with Tutor Perini.

Fluor, with its broader global footprint, has seen strong backlog expansion across energy, chemicals and infrastructure, supported by both public and private sector demand. Infrastructure funding in the US is a positive catalyst, but Fluor’s diversification means benefits extend beyond civil projects, giving it multiple levers to grow its backlog. The company’s restructuring efforts have also enhanced its ability to capture higher-margin work.

Granite Construction has been more directly aligned with U.S. infrastructure tailwinds, particularly in highways, bridges and water projects. Granite Construction’s backlog has been steadily building, supported by state and federal funding programs. Compared with Tutor Perini and Fluor, Granite Construction’s smaller scale is balanced by its focused exposure, making infrastructure funding a more direct growth driver.

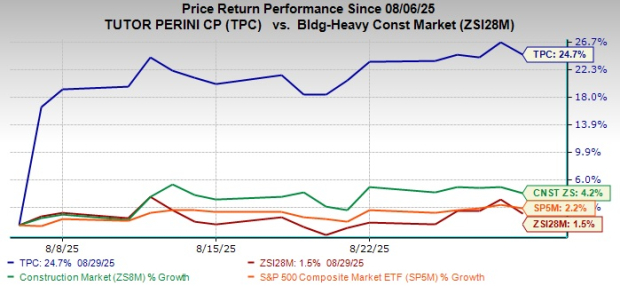

Shares of this California-based general contracting company have gained 24.7% since the day of its second-quarter 2025 earnings release (Aug. 6), outperforming the Zacks Building Products - Heavy Construction industry, the broader Zacks Construction sector and the S&P 500 index.

TPC’s current valuation looks promising for investors. The stock is currently trading at a discount compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 15.1. The discounted valuation of the stock, compared with its peers, advocates for an attractive entry point for investors.

The stock currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 7 hours | |

| Aug-03 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-28 | |

| Jul-28 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite