|

|

|

|

|||||

|

|

|

Dutch Bros Inc. (BROS) is pressing the accelerator on expansion, but the key question remains whether transaction growth can keep pace with its ambitious store rollout.

In the second quarter of 2025, revenues surged 28% year over year to $416 million, supported by 6.1% system same-shop sales growth and 3.7% transaction growth. Company-operated shops posted even stronger comps at 7.8%, fueled by nearly 6% transaction gains. These results highlight solid customer demand at a time when consumer traffic has been pressured across much of the restaurant industry.

Expansion remains the centerpiece of Dutch Bros’ strategy. The chain opened 31 shops in second-quarter 2025, entering Indiana as its 19th state and is on track to open at least 160 system shops in 2025. New store productivity is holding at elevated levels, with average unit volumes of $2.05 million, reinforcing management’s confidence in achieving a long-term target of more than 2,000 shops by 2029.

At the same time, the company is leaning on transaction-driving initiatives, menu innovation, increased advertising and its Dutch Rewards program, which accounted for 72% of system transactions. Still, maintaining traffic momentum could prove challenging as competition in the beverage category intensifies and consumer spending normalizes.

For now, Dutch Bros is delivering on both growth and profitability, with adjusted EBITDA up 37% in second-quarter 2025. Investors will be watching closely to see if customer traffic can continue to fuel comps as the brand stretches into new geographies.

Dutch Bros’ expansion drive brings it into sharper competition with both established and emerging players. Starbucks Corporation (SBUX), the global coffee leader, continues to leverage its vast scale, menu innovation and a powerful Rewards program to retain customer loyalty. While U.S. traffic has softened recently, Starbucks’ digital reach and pricing power remain key competitive advantages that Dutch Bros must counter with value and localized engagement.

On the regional front, Krispy Kreme, Inc. (DNUT) has been pushing deeper into beverage offerings as part of its strategy to broaden relevance beyond doughnuts. With an increasing emphasis on coffee and specialty drinks, Krispy Kreme is vying for share in similar dayparts where Dutch Bros thrives. Both brands aim to capitalize on convenience-driven demand, but Dutch Bros’ ability to maintain transaction growth will be critical as larger rivals strengthen their hold in overlapping markets.

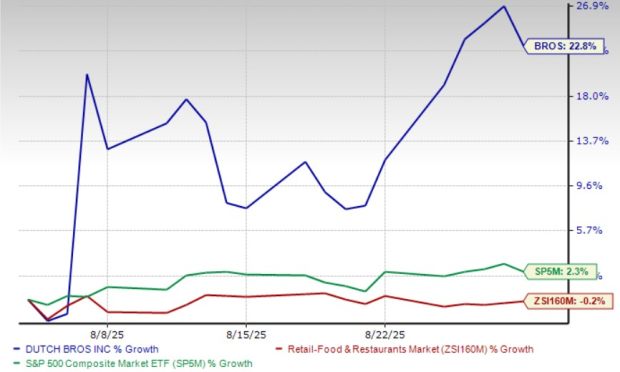

Dutch Bros’ stock has surged 22.8% in a month against the industry’s decline of 0.2%.

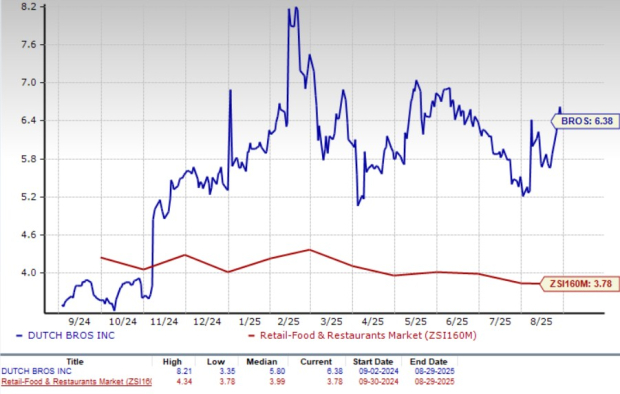

BROS is trading at a premium to the industry, with a forward 12-month price-to-sales of 6.38X. The figure is well above the industry average of 3.78X.

Over the past 30 days, BROS' 2025 earnings estimates have increased to 66 cents per share from 59 cents.

Dutch Bros currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 6 hours | |

| 12 hours | |

| 20 hours | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite