|

|

|

|

|||||

|

|

|

Walmart Inc.’s WMT second-quarter fiscal 2026 results underscore the company’s strong sales momentum. Revenues rose 5.6% in constant currency, fueled by e-commerce growth and solid performance in the United States and internationally. Yet, adjusted operating income inched up just 0.4% in constant currency, held back by a 560-basis-point drag from higher general liability claims.

Reflecting demand resilience, management raised its full-year sales outlook to 3.75%-4.75%, up from 3%-4%, and lifted adjusted EPS guidance to $2.52-$2.62, supported by reduced currency headwind (now 2-3 cents versus 5 cents earlier). However, Walmart kept its forecast for adjusted operating income growth unchanged at 3.5%-5.5% in constant currency, signaling caution despite accelerating top-line trends.

Profitability remains constrained by expense pressures. The company booked an additional $450 million in liability claim costs during the second quarter, bringing the year-to-date impact to $730 million. Management noted claims inflation will persist in the second half, though at a slower pace, while tariffs and an unfavorable merchandise mix continue to weigh on margins.

Still, Walmart is gaining traction in businesses that could bolster profitability over time. Advertising revenues surged nearly 50% globally, including 31% growth in Walmart Connect U.S. (excluding VIZIO), while membership income advanced 15%. E-commerce economics also improved, with marketplace penetration and delivery efficiencies supporting better margins.

Walmart has shown it can boost sales, making margin recovery the main focus moving forward.

Walmart, which competes with Costco Wholesale Corporation COST and Target Corporation TGT, has been a standout performer, with shares rallying 25.6% in the past year, almost in tandem with the industry’s growth of 25.8%. Shares of Costco have advanced 5.7%, while Target declined 37.5% in the aforementioned period.

From a valuation standpoint, Walmart's forward 12-month price-to-earnings ratio stands at 34.84, higher than the industry’s 31.98. WMT carries a Value Score of C. Walmart is trading at a premium to Target (with a forward 12-month P/E ratio of 12.19) but at a discount to Costco (52.49).

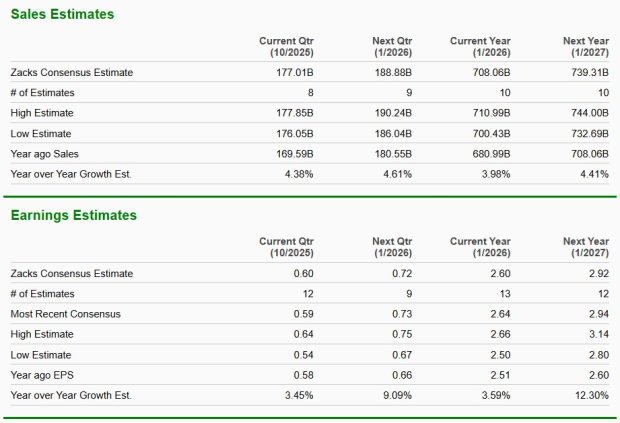

The Zacks Consensus Estimate for Walmart’s current financial-year sales and earnings per share implies year-over-year growth of 4% and 3.6%, respectively.

Walmart currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours |

Walmart To Report Results, Fresh Off New Highs, A New CEO And $1 Trillion Market Cap

WMT

Investor's Business Daily

|

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite