|

|

|

|

|||||

|

|

|

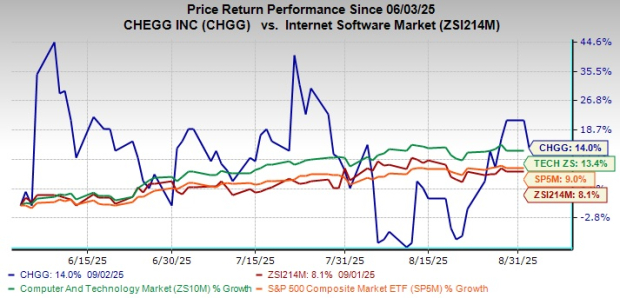

Chegg, Inc.’s CHGG shares have trended upward 14% in the past three months, outperforming the Zacks Internet - Software industry, the Zacks Computer and Technology sector and the S&P 500 index.

The stock is currently trading at $1.41 as of today’s market open, with a 52-week high-low range of 44 cents to $2.43 per share.

This California-based education technology company is gaining from the reinvention of its Chegg Study service and Busuu Premium offering. Moreover, its focus on enhancing the Chegg Skills product and implementing AI to transform Chegg Study into a more efficient business is boding well for its long-term prospects. Apart from focusing on building revenue growth, the company is also engaging in efforts to reduce its expense structure and expand its liquidity position through several restructuring initiatives.

Let us dive into understanding the factors that are driving Chegg’s momentum.

Chegg is currently focusing on revamping Chegg Study, its core academic product, into a Personalized Learning Assistant through AI. This transformation into a personalized learning coach helps students improve their chances of graduating through a more effective learning process. For September 2025, the company plans to launch two new core capabilities into the existing user interface, further enhancing Chegg Study into a personalized learning coach for the modern learner.

Besides Chegg Study, the company is also benefiting from its investments in the Busuu and Skills business, highlighting growth areas including language learning, workplace readiness and upskilling. Busuu, the language learning business, underwent enhancements across AI-powered features, including the new speaking bites product, which is boding well for Chegg. Busuu’s revenues grew 15% year over year in the second quarter of 2025, reflecting impressive contributions from the B2C (6% year-over-year revenue growth) and B2B (39% year-over-year revenue growth) segments. For the second half of 2025, under B2C, the company expects to focus on product innovation, with continued emphasis on AI as a driver of personalization. Under B2B, the focus will remain on rolling out Guild into the English learning vertical and expanding its offering with Learning Pathways.

Chegg is taking aggressive steps to reduce its total operating expenses across multiple fronts, including workforce reduction and office closures, necessary cuts in operating expenses, lease and real estate rationalizations and significant capital expenditure reductions. Through these restructuring efforts, during the first six months of 2025, Chegg’s total operating expenses declined year over year by 72% to $202.5 million. The exceptional downtick was due to a 34% decline in research and development expenses, a 20% decrease in sales and marketing expenses, and a 9% decline in general and administrative expenses.

Thanks to its disciplined cost management and restructuring actions, CHGG expects to realize adjusted expense savings of between $165 million and $175 million for 2025, with an additional $100-$110 million in adjusted savings expected in 2026. Through these efforts, the company aims to strengthen its cash flow and create shareholder value, thereby expanding its long-term market position.

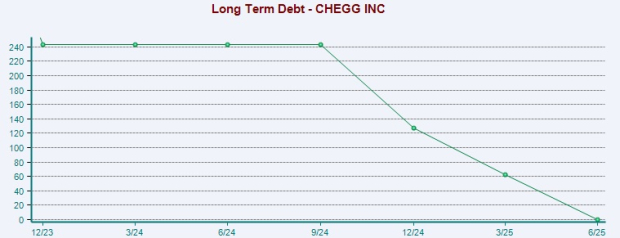

Chegg is currently maintaining a stable and sufficient liquidity position, intending to utilize its free cash to strengthen its business and enhance shareholder value. As of June 30, 2025, it had cash and cash equivalents and investments of $114.1 million, with no long-term debt, as witnessed from the chart below. As of the second quarter of 2025, its current maturities were $62.5 million, down from $358.6 million as of 2024-end.

As of the first six months of 2025, net cash provided by operating activities was $19.7 million compared with $67.5 million in the year-ago comparable period. Thus, given the liquidity position and net cash flows from operations, CHGG is well-positioned to fund its operations and debt service obligations for at least the next 12 months.

Chegg operates in a highly competitive landscape that spans school programs, online education and digital learning services. The company has long been recognized for its subscription-driven model that combines study support, textbook solutions and now Busuu-powered language learning. Against this backdrop, Coursera, Inc. COUR, Duolingo, Inc. DUOL and Stride, Inc. LRN each represent distinct yet overlapping challenges within the broader edtech ecosystem.

Coursera offers a massive library of university-backed courses and certifications, positioning itself as a leader in academic partnerships and professional development. For students seeking career-oriented learning, Coursera creates a formidable option. Duolingo, on the other hand, dominates the language-learning niche with its gamified app and AI-driven engagement. With a strong mobile presence and daily user engagement, Duolingo has built a brand synonymous with accessible, bite-sized learning. Meanwhile, Stride focuses primarily on K-12 online school programs, providing virtual classes, curriculum and supplemental tools that have grown in relevance with shifts toward digital-first learning.

While Coursera, Duolingo and Stride each carve out specialized markets, Chegg’s competitive advantage lies in its subscription-based ecosystem, which integrates study help, textbooks, skills and now AI-enabled support. This combination creates stickiness and convenience for students, making Chegg a one-stop platform for learning services in a fragmented edtech environment.

CHGG’s bottom-line estimates for 2025 indicate a loss per share, while those of 2026 indicate break-even earnings. Over the past 30 days, the estimates for 2025 have contracted to 11 cents per share, while those of 2026 have contracted to a breakeven point.

Although the estimated figures for 2025 indicate a downtrend of 114.7% year over year, estimates for 2026 indicate 100% growth.

CHGG stock is currently trading at a discount compared with the industry peers, with a forward 12-month price-to-sales (P/S) ratio of 0.42, as evidenced by the chart below. The discounted valuation of the stock, compared with its peers, advocates for an attractive entry point for investors.

Chegg’s strategic initiatives, notably the reinvention of Chegg Study into an AI-driven personalized learning assistant and continued growth in the Busuu language learning platform, are driving momentum. Moreover, on the financial front, its disciplined cost-cutting efforts, combined with its solid liquidity position, provide flexibility to sustain operations and invest in growth.

Despite near-term earnings pressures, with 2025 expected to show a loss per share, the trajectory improves toward breakeven in 2026, indicating an inflection point in profitability. Besides, its discounted valuation compared with its industry peers marks an attractive entry point.

Given Chegg’s ongoing product innovation, successful cost optimization, improved growth outlook and attractive valuation, the stock appears well-positioned for long-term upside. Backed by its current Zacks Rank #1 (Strong Buy), CHGG stock looks like a favorable investment choice at current levels. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-31 | |

| Mar-26 | |

| Mar-18 | |

| Mar-13 | |

| Mar-13 | |

| Mar-13 | |

| Mar-12 | |

| Mar-12 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite