|

|

|

|

|||||

|

|

|

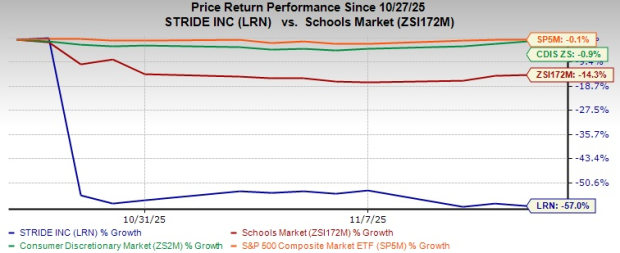

Stride, Inc. LRN plunged 57% since reporting its first-quarter fiscal 2026 earnings on Oct. 28, underperforming the Zacks Schools industry, the broader Zacks Consumer Discretionary sector and the S&P 500 Index.

The company’s first-quarter fiscal 2026 earnings and revenues topped the Zacks Consensus Estimate by 23.6% and 1%, respectively. Year over year, the metrics grew 39.4% and 12.7%, respectively, owing to higher enrollments and revenue per enrollment. The Career Learning segment outpaced the General Education segment's growth rate during the quarter. (read more: Stride Q1 Earnings & Revenues Top Estimates, Enrollment Hits New Record)

Even though the company laid out an upbeat fiscal 2026 outlook after starting the year with incremental growth, investors’ confidence is likely to have been hurt based on its short-term prospects. Sometimes, business enhancements and upgrades can result in weak near-term performance, which is exactly the case for Stride here. The management’s indication of muted enrollment trends throughout the fiscal year, with issues regarding new technology platform rollouts, has been concerning the investors.

During the first quarter of fiscal 2026, Stride highlighted disruptions regarding its two technology platform rollouts, including a front-end learning platform and a back-office platform. At the start of August 2025, the company started to witness withdrawals due to poor platform performance, such as login issues. Poor customer experience resulted in lower-than-expected conversion rates.

LRN’s approach of continuously investing in upgrading its learning and technology platforms is encouraging, but the new upgrade did not go as planned, leading to approximately 10,000-15,000 fewer enrollments, which could have been achieved without such disruptions. It is currently working on minimizing these technical issues and offering a seamless customer experience; however, the entire process might take some time, as indicated by the company. The presence of these technical challenges is expected to pull back the enrollment growth in fiscal 2026, unlike previous years, as indicated by the management.

Thus, based on all the adverse in-house scenarios, Stride laid out a comparatively muted fiscal 2026 outlook, even though the growth rate reflects positive trends. Fiscal 2026 revenues are expected to be between $2.480 billion and $2.555 billion, up from $2.405 billion reported in fiscal 2025.

LRN’s earnings estimates for fiscal 2026 and fiscal 2027 have moved south over the past 30 days by 4.8% and 8.3%, respectively. The analysts’ expectations are likely to have been hurt by the ongoing in-house concerns and muted enrollment growth outlook declared by the company.

Nonetheless, the revised figures for fiscal 2026 and 2027 imply year-over-year improvements of 3.6% and 6.2%, respectively.

Stride competes in career learning and K-12 services alongside online platform alternatives with key market players, including Strategic Education, Inc. STRA, American Public Education, Inc. APEI and Coursera, Inc. COUR.

Strategic Education brings a complementary playbook focused on career-relevant post-secondary credentials and campus-plus-online programs that emphasize workforce alignment, employer partnerships and outcomes-oriented program design, strengths that position it to capture demand for upskilling and credentialing at scale. On the other hand, American Public Education targets working adults, military and nursing markets with mission-built programs and stable enrollment channels, giving it niche depth in healthcare and public-service career pipelines where predictable demand and outcomes metrics matter.

Moreover, Coursera’s model offers flexibility and global recognition, but Stride’s ability to integrate tutoring and support services across its portfolio has provided stickier enrollment growth, especially in career-oriented pathways.

LRN appears to hold a competitive edge in its integrated K-12 plus career learning model, which few others fully replicate, and in its growing traction in the adult skills market. That said, Coursera’s scale and academic brand, Strategic Education’s advantage in deep postsecondary career programming and employer alignment and American Public Education’s edge in mission-aligned niche programs with steady institutional funnels, offer substantial competition.

Attractive Business Model: This Virginia-based education company offers K-12 online school programs alongside expanding hybrid and in-person options through a career learning platform for areas like healthcare, IT and advanced manufacturing. As the market is shifting from traditional school choices to more virtual and career-oriented options, the diversified offerings by the company fit perfectly into the puzzle. Its evolving model positions it at the intersection of technology, personalized instruction and workforce readiness.

Notably, its focus on hybrid innovation also benefits from state-level funding flexibility, enabling partnerships with school districts that seek scalable, cost-effective solutions. The K12 Tutoring collaboration with Lake Forest School District in Delaware to offer innovative and tailored educational solutions to students can be considered in this aspect.

Focus Toward Affordable Offerings: Amid an inflationary economic scenario with ongoing challenges regarding affordability, Stride is working on providing its students with affordable learning options. The company is working on sculpting programs that meet the current market demand trends, as well as being affordable at the same time. During the start of fiscal 2026, LRN rolled out free ELA tutoring for every second and third grader in its serving community. This program enables a child to work on reading, writing and communication skills.

Moreover, regarding career-focused programs, Stride is also working on providing personalized career-forward and tech-enabled education programs at an affordable price. The company’s revenues have the primary contribution from the Career Learning segment compared with the General Education segment. In the first quarter of fiscal 2026, its Career Learning segment’s revenues grew 16.3% year over year to $257.8 million, with enrollments growing 20%. This segment’s revenues outpaced the revenue growth for the General Education segment, which was 10.2% year over year in the fiscal first quarter.

Stable Liquidity Position: Despite facing near-term headwinds, LRN is working on maintaining a stable and sufficient liquidity position. As of Sept. 30, 2025, the company had cash and cash equivalents of $518.4 million, down from $782.5 million as of fiscal 2025. Although the cash position declined sequentially, it is sufficient to meet its long-term obligations worth $416.8 million.

Stride focuses on a balanced capital allocation approach, with excess being utilized across organic business enhancements, inorganic strategies and returning value to its shareholders.

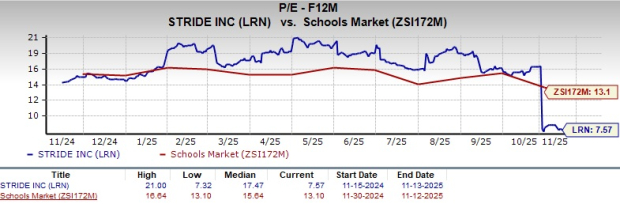

LRN stock is currently trading at a discount compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 7.57, as shown in the chart below.

Growth in the higher-margin Career Learning segment has reinforced Stride’s competitive advantage in blending K-12, hybrid and workforce-oriented education models. Its offerings remain aligned with the rising demand for flexible, career-focused pathways. Moreover, its approach toward expanding affordability initiatives and district partnerships bodes well.

However, the near-term challenges have been concerning. Its technology platform rollout failures due to login and usability issues have pressured investors’ sentiments. Besides, 10,000-15,000 lost enrollments and weaker conversion rates, which prompted management to guide to muted enrollment trends for fiscal 2026, are an unfavorable circumstance.

While Stride trades at a compelling valuation discount and retains strong structural demand tailwinds, restoring enrollment momentum and resolving platform issues will be central to improving investor confidence.

Summing up, based on the above discussion and trends of the technical indicators, it is prudent for existing investors to hold onto this Zacks Rank #3 (Hold) stock for now. New investors are advised to wait for now and look for a better entry point when the trends start favoring LRN stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite