|

|

|

|

|||||

|

|

|

Pfizer is a generally well-run company and the current headwinds aren't really unusual.

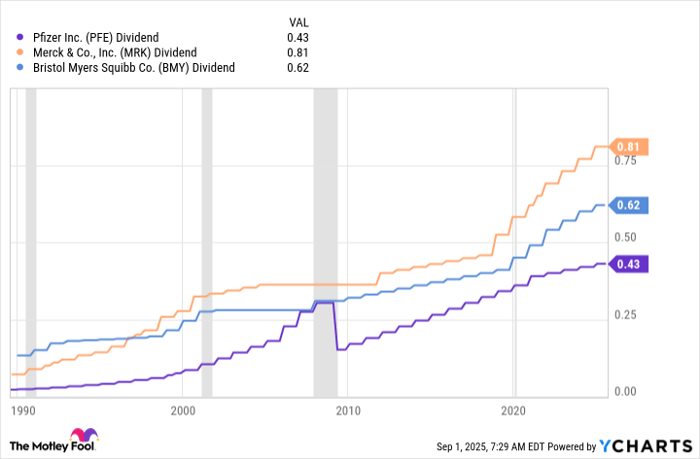

The pharma giant cut its dividend, while peers Merck and Bristol-Myers Squibb did not.

It's not the only high-yield option you have if you're looking to benefit from this industry.

There are a number of reasons to believe that Pfizer (NYSE: PFE) is an attractive dividend stock. The lofty 6.9% dividend yield is the obvious first reason, but the healthcare giant also has a long history of being well run. That said, if you are thinking of stepping in to buy Pfizer today, you'll want to know these three facts before you do.

Image source: Getty Images.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Pfizer is a pharmaceutical company. The drugs it makes are highly complicated to find, test, and develop. This is why drug makers are granted a temporary monopoly on new discoveries. However, the patent protection that companies like Pfizer get eventually end.

And when that happens competitors bring out generic versions of the products at lower price points. This is what's known as a patent cliff in the drug sector. Pfizer has a couple of big drugs expected to lose patent protection in the years ahead. As such, investors are closely watching, and worrying about, Pfizer's drug pipeline.

On top of that, there's a bit of uncertainty in the healthcare sector right now because of regulatory changes taking place in the United States. The new administration in Washington is viewing the healthcare industry, and particularly drug makers, in a more critical light. That has investors worried about the future, too. And as you might expect, stocks like Pfizer have been performing weakly. That's why the dividend yield is so high today.

The thing is, drug discovery is lumpy and regulatory changes aren't abnormal. From a big-picture perspective, Pfizer is just dealing with typical business gyrations. It has successfully done so before and will likely continue to be a long-term survivor this time around, as well. Concern is justified, but these aren't issues that will spell the end of this industry-leading pharma stock.

Pfizer has increased its dividend annually for 15 consecutive years. That streak, however, follows a dividend cut. This isn't meant as a warning that a another dividend cut is imminent. In fact, that doesn't seem very likely at all, noting that the adjusted earnings dividend payout ratio was 55% in the second quarter of 2025.

But Pfizer isn't the only pharma stock you can buy. Competitor Merck (NYSE: MRK) has a lower 3.9% or so dividend yield, but it has a dividend that has trended generally higher over time. Not every year, mind you, but when Pfizer cut its dividend during the Great Recession, Merck did not. The same basic story is in play with Bristol-Myers Squibb, which has a nearly 5.3% yield. If dividend consistency is important to you, you may want to consider stepping down on yield.

PFE Dividend data by YCharts

There's also a big-picture consideration to make here about drug maker Pfizer. You can get a 6.4% yield from real estate investment trust (REIT) Alexandria Real Estate. Why would a REIT be an alternative to a pharma stock? Alexandria's business focus is on leasing research space to healthcare companies like Pfizer. OK, Pfizer isn't one of the REIT's largest tenants, but Eli Lilly, Moderna, and Bristol-Myers Squibb are the top three tenants. Merck is No. 17.

Investing in Alexandria is a way to get exposure that sidesteps the typical drug cycle, since rent still has to be paid even after a patent cliff. The big story here, however, is that research and development is vital to the pharma industry. So Alexandria's tenants can't simply stop their research efforts if they want to remain competitive.

To be fair, Alexandria's yield is historically high today because it is working through a difficult period. Notably, occupancy has dropped around four percentage points in just six months. But it is still a well-positioned business (occupancy remains over 90%) and likely to survive without the need for a dividend cut. If you are looking at Pfizer, you should at least take the time to consider this REIT as a high-yield alternative.

The upshot here is that buying Pfizer is probably not a huge mistake, even for more conservative investors. But the dividend history has a material blemish on it that you won't find with some of its direct competitors. And if you don't like the inherent volatility of the drug discovery process, there are "picks and shovels" alternatives, like Alexandria, that you might want to consider instead.

Basically, Pfizer is OK, but not the only dividend choice you have at your disposal to get exposure to the pharmaceutical sector.

Before you buy stock in Pfizer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Pfizer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $654,759!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,046,799!*

Now, it’s worth noting Stock Advisor’s total average return is 1,042% — a market-crushing outperformance compared to 183% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alexandria Real Estate Equities, Bristol Myers Squibb, Merck, and Pfizer. The Motley Fool recommends Moderna. The Motley Fool has a disclosure policy.

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-14 | |

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite