|

|

|

|

|||||

|

|

|

Over the last six months, Western Union’s shares have sunk to $8.73, producing a disappointing 18% loss - a stark contrast to the S&P 500’s 11.6% gain. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Western Union, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons why WU doesn't excite us and a stock we'd rather own.

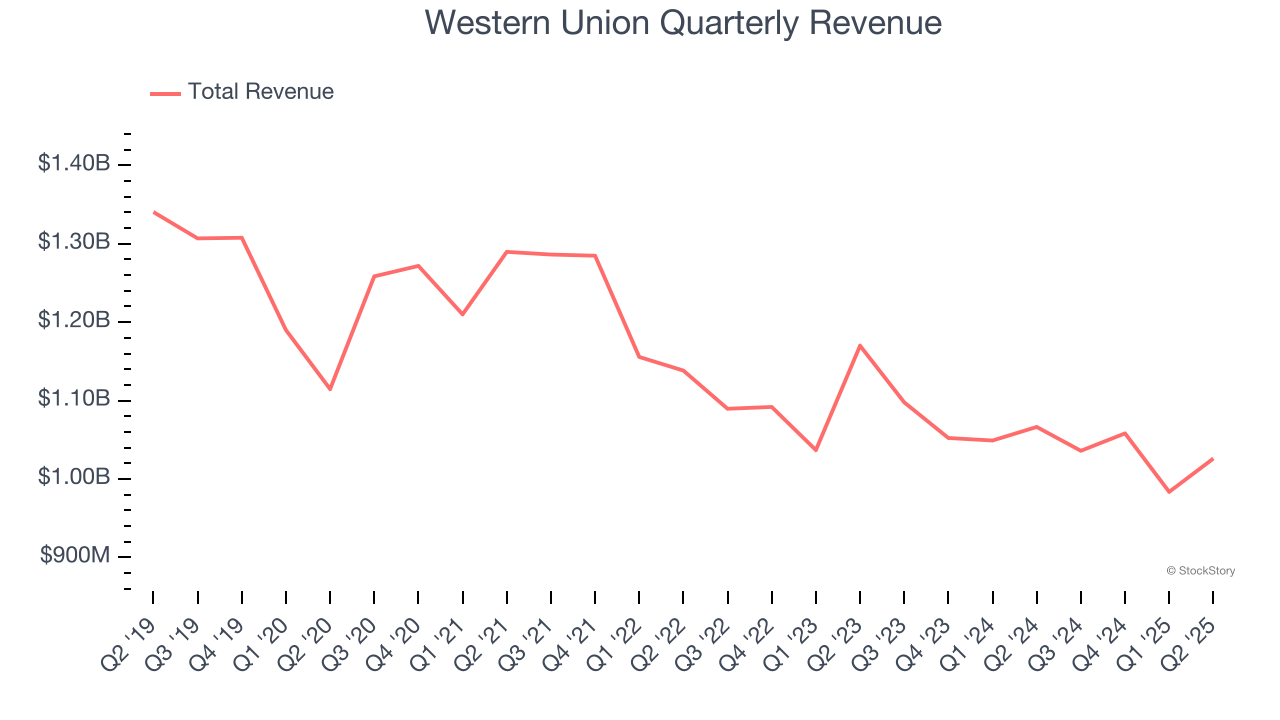

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

Over the last five years, Western Union’s demand was weak and its revenue declined by 3.6% per year. This was below our standards and signals it’s a low quality business.

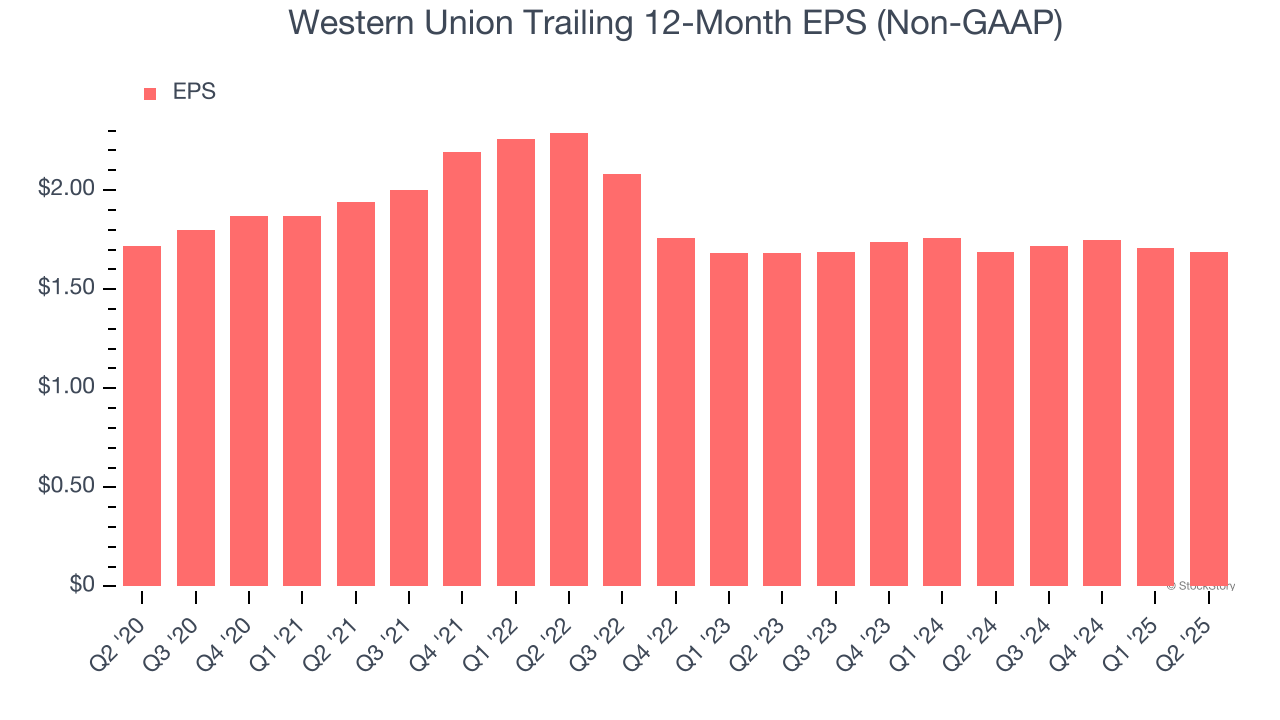

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Western Union’s flat EPS over the last five years was weak. On the bright side, this performance was better than its 3.6% annualized revenue declines.

Return on equity (ROE) measures how effectively banks generate profit from each dollar of shareholder equity - a critical funding source. High-ROE institutions typically compound shareholder wealth faster over time through retained earnings, share repurchases, and dividend payments.

Over the last five years, Western Union has averaged an ROE of negative 1,261%, a bad result not only in absolute terms but also relative to the majority of firms putting up 25%+. It also shows that Western Union has little to no competitive moat.

We see the value of companies driving economic growth, but in the case of Western Union, we’re out. Following the recent decline, the stock trades at 4.8× forward P/E (or $8.73 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now. We’d recommend looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-24 | |

| Mar-24 | |

| Mar-21 | |

| Mar-17 | |

| Mar-13 | |

| Mar-11 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite