|

|

|

|

|||||

|

|

|

Joby Aviation JOBY, a leading player in the electric vertical takeoff and landing (eVTOL) space, is currently considered relatively overvalued. In terms of price-to-book value, JOBY is trading at 12.35X, higher than the Zacks Transportation - Airline industry and peer Archer Aviation ACHR. Like Joby Aviation, Archer Aviation also has a Value Score of F.

The question regarding JOBY that naturally arises is whether it is worth overpaying for the transportation player. Let us delve deeper and analyze JOBY’s fundamentals to answer the question.

Recently, JOBY showcased its autonomous defense capabilities by completing a military exercise. As part of the Resolute Force Pacific, a department-level exercise led by Pacific Air Forces, Joby conducted a demonstration and validation of its Superpilot autonomous flight technology over the Pacific Ocean and Hawaii. The exercise saw the transportation company logging in excess of 7,000 miles of autonomous operations across more than 40 flight hours.

The demonstration was in sync with Joby’s long-term strategy to develop dual-use technologies and highlighted its ability to offer an autonomous solution for the U.S. government’s requirement for light intra-theater airlift. Joby’s latest success positions it well to compete for the future Department of Defense programs.

Joby aims to start carrying passengers in Dubai next year. As part of its efforts related to air taxi commercialization, Joby recently completed the acquisition of Blade Air Mobility’s urban air mobility passenger business. Following the closure, Blade has changed its name to Strata Critical Medical SRTA. The passenger operations will continue to be led by its founder and CEO, Rob Wiesenthal, as a wholly-owned subsidiary of Joby.

The acquisition provides Joby access to Blade’s established network of terminals and loyal flyers in key markets, such as New York and Southern Europe. As a result, Joby gets a ready-made market for the aircraft. The buyout may expedite Joby’s entry into commercial service with its eVTOL aircraft once certified. Moreover, the closure of the buyout is likely to provide Joby a head start over competitors like Archer Aviation. Apart from providing market access and scale, the buyout is likely to reduce costs for new vertiports.

As part of its push toward commercialization, Joby recently completed its first flight between two U.S. airports — Marina and Monterey, CA — operating alongside other aircraft in FAA-controlled airspace. This milestone marks significant progress in Joby’s path to commercial readiness, showcasing advancements in safety, operational performance, air traffic integration, and certification efforts.

Earlier in the year, Joby unveiled plans to expand operations. To this end, the transportation company announced the expansion of its site in Marina, CA, which will double its aircraft production capacity at that location. The expanded site will span 435,500 square feet, helping the company to scale up its commercial operations. Once operational, Joby expects the Marina site to be able to produce up to 24 aircraft per year as it races to launch air taxis.

Driven by its commercialization-related efforts, JOBY shares have performed exceedingly well lately, gaining in excess of 72% in the past 90 days, outperforming its industry as well as rival Archer Aviation.

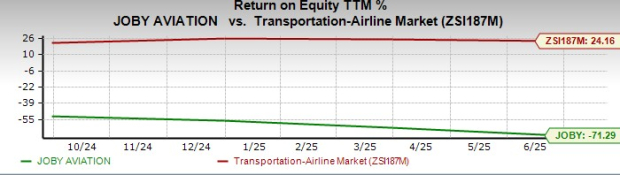

Joby Aviation is unlikely to be profitable any time soon, as commercial operations have yet to start. The company’s negative return on equity further highlights its lack of profitability.

Image Source: Zacks Investment Research

In its path toward commercialization, JOBY is unlikely to escape turbulence as it navigates regulatory approvals, infrastructure development and consumer adoption. In the absence of commercialization, there is no real demand for urban air mobility at present.

Only time will tell how the market and customer demand for eVTOLs will turn out to be. Public acceptance of eVTOLs as an alternative to traditional transport methods could face hurdles related to safety, noise and affordability concerns. Without widespread recognition, JOBY's growth potential may be constrained. Additionally, the risk of battery failure due to high voltage and thermal issues is highly likely for eVTOL aircraft.

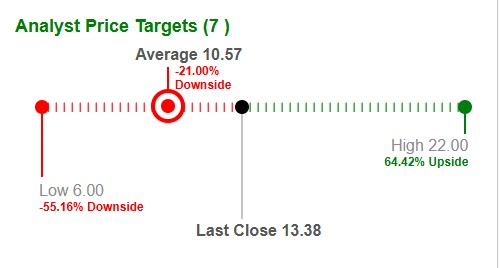

Based on the write-up, we can safely conclude that the company’s long-term outlook is strong, given the brightness associated with the eVTOL market and some investors may be willing to accept the premium. However, its current stock price already reflects a lot of this optimism. With the company facing certain risks, like the absence of significant revenues and uncertainties related to commercialization, jumping in now might mean overpaying. The Wall Street average target price for Joby Aviation is $10.57, suggesting a 21% downside.

Despite the eVTOL-related optimism, JOBY, currently carrying a Zacks Rank #4 (Sell), looks like a stock to avoid rather than chase.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jun-24 | |

| Jun-24 | |

| Jun-22 | |

| Jun-15 |

How Joby is building its air taxi company in Dayton with workers who are production heroes

JOBY +5.68%

Journal-News, Hamilton, Ohio

|

| Jun-15 |

Thomas Gnau: How Joby is building its air taxi company in Dayton with workers who are production heroes

JOBY +5.68%

Journal-News, Hamilton, Ohio

|

| Jun-15 | |

| Jun-09 |

Cathie Wood Unloads Nearly $13 Mil Of ACHR Stock. Vertical Aerospace Completes Flight.

ACHR -7.16% ACHR -5.08%

Investor's Business Daily

|

| Jun-09 | |

| Jun-09 | |

| Jun-07 | |

| Jun-02 | |

| May-27 | |

| May-26 | |

| May-20 | |

| May-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite