|

|

|

|

|||||

|

|

|

New Elite Feature: Compare relative returns, fundamentals, and sector rankings head-to-head.

Globus Medical, Inc. GMED continues to benefit from the robust demand for its Musculoskeletal Solutions products. Additionally, its string of product launches is highly promising to drive growth in the coming quarters. Meanwhile, headwinds from unfavorable foreign exchange and intense competition remain concerns for GMED’s operations.

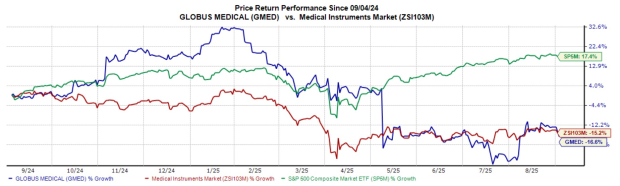

In the past year, this Zacks Rank #3 (Hold) stock has declined 16.6% compared with the industry’s 15.2% fall. The S&P 500 composite rose 17.4% in the same time period.

The renowned medical device company has a market capitalization of $7.94 billion. Globus Medical has an earnings yield of 5.4%, well ahead of the industry’s -4.9% yield. Its earnings surpassed estimates in three of the trailing four quarters, and missed in one, delivering an average surprise of 10.8%.

Let’s delve deeper.

Musculoskeletal Prospects Strong: Globus Medical is gaining market share in the musculoskeletal solutions space, banking on the strong performance of its implantable devices, biologics, accessories and unique surgical instruments. Ongoing momentum in the company’s U.S. Spine business remains encouraging. In line with this, the U.S. Spine business grew 5.7% year over year in the second quarter. Additionally, the company’s core trauma product portfolio continues to grow rapidly, driven by new investments and a strong focus on expanding its reach. In the second quarter, the core trauma business grew 35% year over year.

The company plans to expand its international presence by introducing more Musculoskeletal Solutions products and growing its sales force in both existing and new markets. Meanwhile, the recent acquisition of Nevro expands Globus Medical's presence in the musculoskeletal market, unlocking a $2.5 billion market opportunity. This strategic move complements Globus Medical’s current spinal portfolio offering.

Steady Pace of Product Development: In line with the company’s business strategy to focus on its integrated product development, Globus Medical is consistently making efforts in research and development. In July, the company launched DuraPro with Navigation, a next-generation oscillating system designed to safeguard delicate tissue. In addition to DuraPro, it launched Verzera, a navigated high-speed drill system integrated with the ExcelsiusGPS and ExcelsiusHub systems. In the previous quarter, the company expanded the Advanced Materials Science implant portfolio with the COHERE ALIF Spacer. Additionally, the launch of Modulus ALIF Blades marks an extension of its market-leading Modulus ALIF interbody spacer system.

Image Source: Zacks Investment Research

Exposure to Currency Movement: The company is subject to currency exchange rate fluctuations related to its international sales, which accounted for approximately 19.4% of the total net sales in the second quarter of 2025. A significant portion of GMED’s foreign revenues and expenses is generated in Japan, the Eurozone, the United Kingdom and Australia. Additionally, government policy changes and related uncertainty about policy changes could increase market volatility and currency exchange rate fluctuations, creating added pressure for Globus Medical.

Competitive Landscape: The presence of a large number of players made the musculoskeletal devices market intensely competitive. The orthopedic industry, in particular, is highly competitive with the presence of more prominent players. Globus Medical needs to constantly introduce or acquire new products to withstand the competitive pressure and maintain its market share.

The Zacks Consensus Estimate for GMED’s 2025 earnings per share (EPS) has moved north 1.3% to $3.21 in the past 30 days.

The Zacks Consensus Estimate for the company’s 2025 revenues is pegged at $2.85 billion, suggesting a 13% rise from the year-ago reported number.

Some better-ranked stocks in the broader medical space are Envista NVST, Masimo MASI and Phibro Animal Health PAHC.

Envista has an estimated earnings growth rate of 15.2% for fiscal 2026 compared with the S&P 500 composite’s 11.7% growth. Shares of the company have rallied 16% compared with the industry’s 3.4% growth. NVST’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 16.50%.

NVST carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Masimo, currently carrying a Zacks Rank #2, has an estimated long-term earnings growth rate of 12.5% compared with the industry’s 9.9%. Its earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 9.17%. MASI shares have rallied 18.9% against the industry’s 15.4% decline in the past year.

Phibro Animal Health, carrying a Zacks Rank #2, has an earnings yield of 6.3% against the industry’s -0.3%. Shares of the company have surged 76.5% compared with the industry’s 3.4% growth. PAHC’s earnings beat estimates in each of the trailing four quarters, with the average surprise being 27.9%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| May-22 | |

| May-21 | |

| May-07 | |

| May-07 | |

| May-07 | |

| May-07 | |

| May-06 | |

| May-06 | |

| May-06 | |

| May-06 | |

| May-05 | |

| May-05 | |

| May-04 | |

| Apr-29 | |

| Apr-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite