|

|

|

|

|||||

|

|

|

Outdoor specialty retailer Sportsman's Warehouse (NASDAQ:SPWH) reported revenue ahead of Wall Street’s expectations in Q2 CY2025, with sales up 1.8% year on year to $293.9 million. Its non-GAAP loss of $0.12 per share was in line with analysts’ consensus estimates.

Is now the time to buy Sportsman's Warehouse? Find out by accessing our full research report, it’s free.

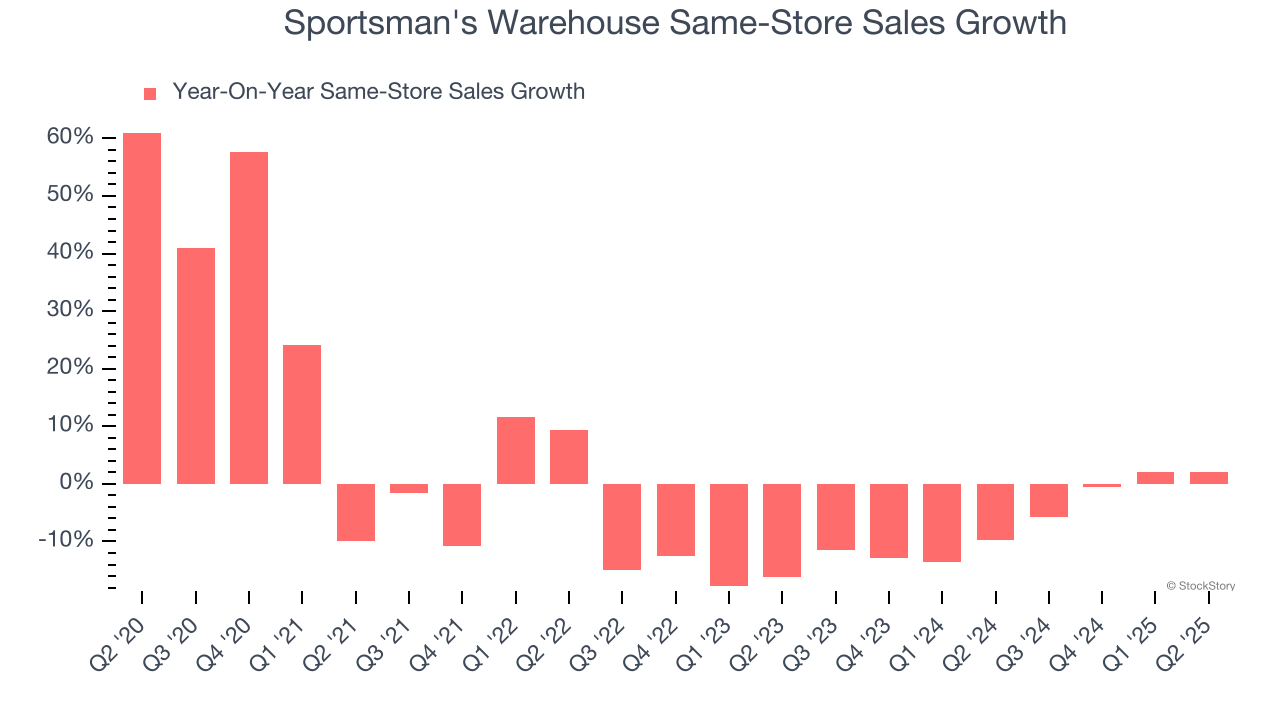

“I’m encouraged by the progress our team is making as we advance our transformation strategy. In the second quarter, we delivered 2.1% same store sales growth—our second consecutive quarter of positive comps—despite ongoing consumer headwinds and a tough June comparison,” said Paul Stone, President and Chief Executive Officer of Sportsman’s Warehouse.

A go-to destination for individuals passionate about hunting, fishing, camping, hiking, shooting sports, and more, Sportsman's Warehouse (NASDAQ:SPWH) is an American specialty retailer offering a diverse range of active gear, equipment, and apparel.

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

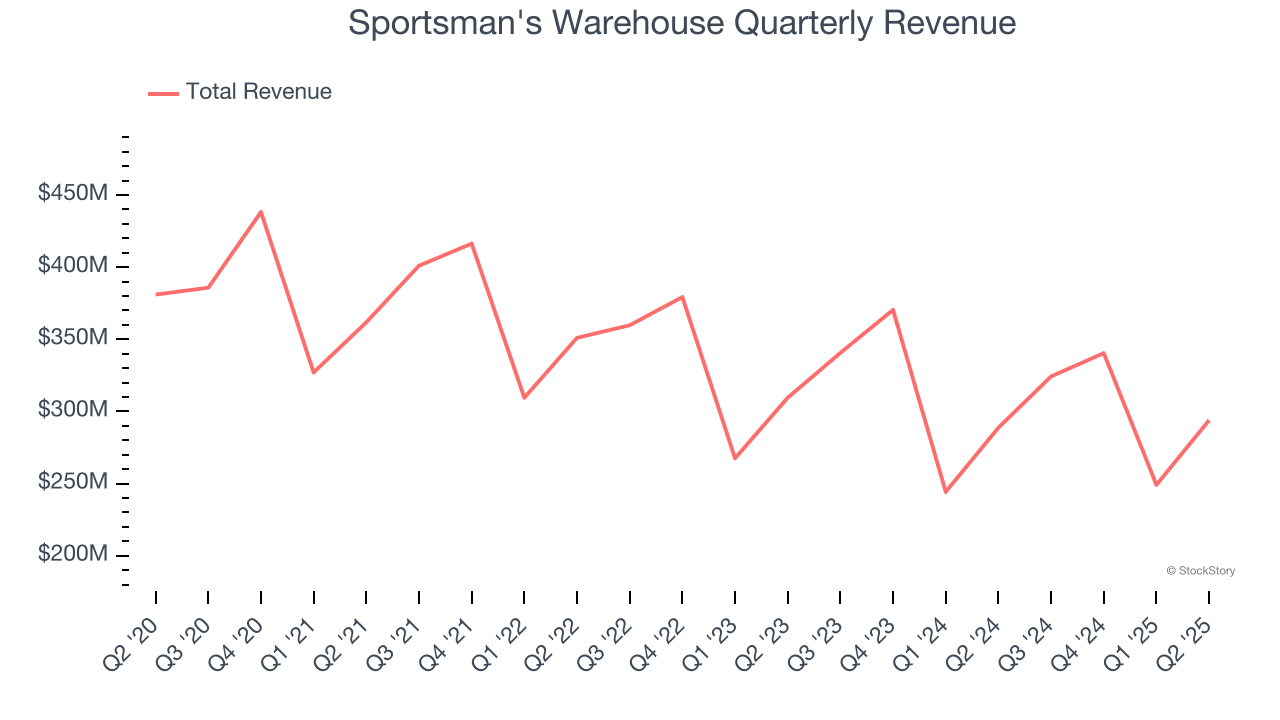

With $1.21 billion in revenue over the past 12 months, Sportsman's Warehouse is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Sportsman's Warehouse’s sales grew at a tepid 6% compounded annual growth rate over the last six years (we compare to 2019 to normalize for COVID-19 impacts). This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, Sportsman's Warehouse reported modest year-on-year revenue growth of 1.8% but beat Wall Street’s estimates by 0.8%.

Looking ahead, sell-side analysts expect revenue to grow 1% over the next 12 months, a deceleration versus the last six years. This projection doesn't excite us and suggests its products will see some demand headwinds.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Sportsman's Warehouse’s demand has been shrinking over the last two years as its same-store sales have averaged 6.2% annual declines.

In the latest quarter, Sportsman's Warehouse’s same-store sales rose 2.1% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

We were impressed by how significantly Sportsman's Warehouse blew past analysts’ EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance trumped Wall Street’s estimates. On the other hand, its EPS was in line. Zooming out, we think this was a good print with some key areas of upside. Investors were likely hoping for more, and shares traded down 5.7% to $2.82 immediately after reporting.

Is Sportsman's Warehouse an attractive investment opportunity at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.

| Jun-03 | |

| Jun-02 | |

| Jun-02 | |

| Jun-02 | |

| May-19 | |

| May-15 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-17 | |

| Mar-10 | |

| Mar-06 | |

| Mar-03 | |

| Feb-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite