|

|

|

|

|||||

|

|

|

Palantir's business is growing rapidly.

Both government and commercial clients are growing at nearly the same pace.

The stock has extreme expectations priced in.

Palantir (NASDAQ: PLTR) has been one of the premier stocks to own in 2025. The stock has more than doubled, but after such an incredible run, investors are wondering if it can continue to rise even higher.

Combine that sentiment with the fact that it's down over 15% from its all-time high, and it currently appears to be an attractive buying opportunity. However, there are a few facts investors should consider before buying Palantir shares, which could save them a significant amount of money in the long term.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: Palantir.

Palantir is a leader in artificial intelligence (AI), and its platform ingests multiple data streams, processes them, and then provides decision-makers with the most accurate information in real time. It can also deploy AI agents through its Artificial Intelligence Platform (AIP), enabling automation. This software was originally developed for government use, but it eventually found a use case outside of its original intent. Still, even with its government business being the more mature segment, it's growing at a rapid pace alongside its commercial division.

Q2 was a masterclass for Palantir, as it delivered 47% revenue growth in the commercial sector to $451 million, and government revenue rose 49% to $553 million. Unlike many of its high-flying software peers, Palantir is also incredibly profitable, and converted 33% of its revenue into net income.

That's about as good a quarter as it gets for most public companies of Palantir's size. With the business obviously thriving in these market conditions, it seems like Palantir is a no-brainer buy right now. However, there is one other important consideration before investing in Palantir's stock, which quickly undermines the investment thesis.

No matter how good an investment is, if you pay the wrong initial price for it, it can turn out to be a failure.

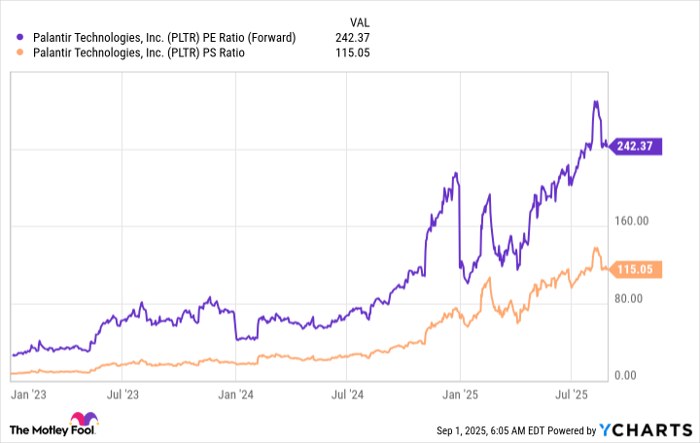

That's how I view an investment in Palantir today. The company is doing phenomenally well, but there's just too much future growth priced into the stock right now. Despite the 15% pullback, Palantir's stock still trades at 242 times forward earnings and at a price-to-sales ratio of 115.

PLTR PE Ratio (Forward) data by YCharts

These two valuation metrics make Palantir one of the most expensive stocks in the market, if not the most expensive. In Q2, Palantir grew revenue at a combined pace of 48%. That's still slower than AI king Nvidia (NASDAQ: NVDA), which grew at a 56% pace. However, Nvidia trades for 39 times forward earnings.

If we set a long-term valuation target of 40 times forward earnings for Palantir's stock, it would take years of growth without the stock price increasing to reach this level.

Let's make these assumptions:

If all three of these factors come true, Palantir would generate $26 billion in revenue and $9.1 billion in profits. Five years from now, that would value Palantir's stock at 41 times forward earnings. So, approximately five years' worth of growth is baked into Palantir's stock price based on those assumptions.

The problem is that those are flawed assumptions.

Wall Street only expects Palantir's revenue to grow at a 34% pace next year. Furthermore, the larger a company gets, the harder it is to grow revenue at a rapid pace, so each successive year will make it harder to reach that elusive 50% growth rate.

If this figure is adjusted down to a more realistic 30% CAGR, it would take Palantir eight years of growth to reach a valuation of around 40 times forward earnings.

Palantir is an incredibly expensive stock that's unrealistically valued. As a result, I think investors should avoid investing in it, as it is likely to be a long-term loser due to its high starting point.

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $661,268!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,045,818!*

Now, it’s worth noting Stock Advisor’s total average return is 1,047% — a market-crushing outperformance compared to 184% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Keithen Drury has positions in Nvidia. The Motley Fool has positions in and recommends Nvidia and Palantir Technologies. The Motley Fool has a disclosure policy.

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 8 hours | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite