|

|

|

|

|||||

|

|

|

PTC’s 32.1% return over the past six months has outpaced the S&P 500 by 20.8%, and its stock price has climbed to $212.96 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now still a good time to buy PTC? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Originally known as Parametric Technology Corporation until its 2013 rebranding, PTC (NASDAQ:PTC) provides software that helps manufacturers design, develop, and service physical products through digital solutions for CAD, PLM, ALM, and SLM.

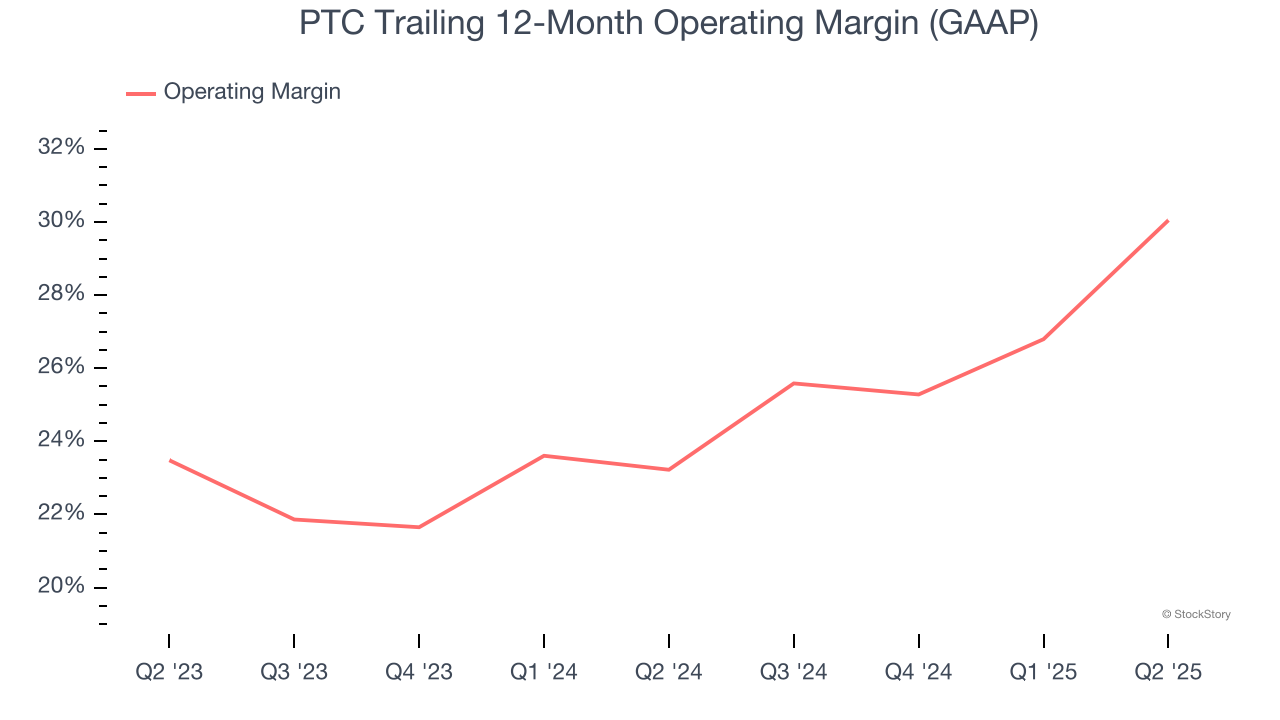

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

PTC has been a well-oiled machine over the last year. It demonstrated elite profitability for a software business, boasting an average operating margin of 30%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

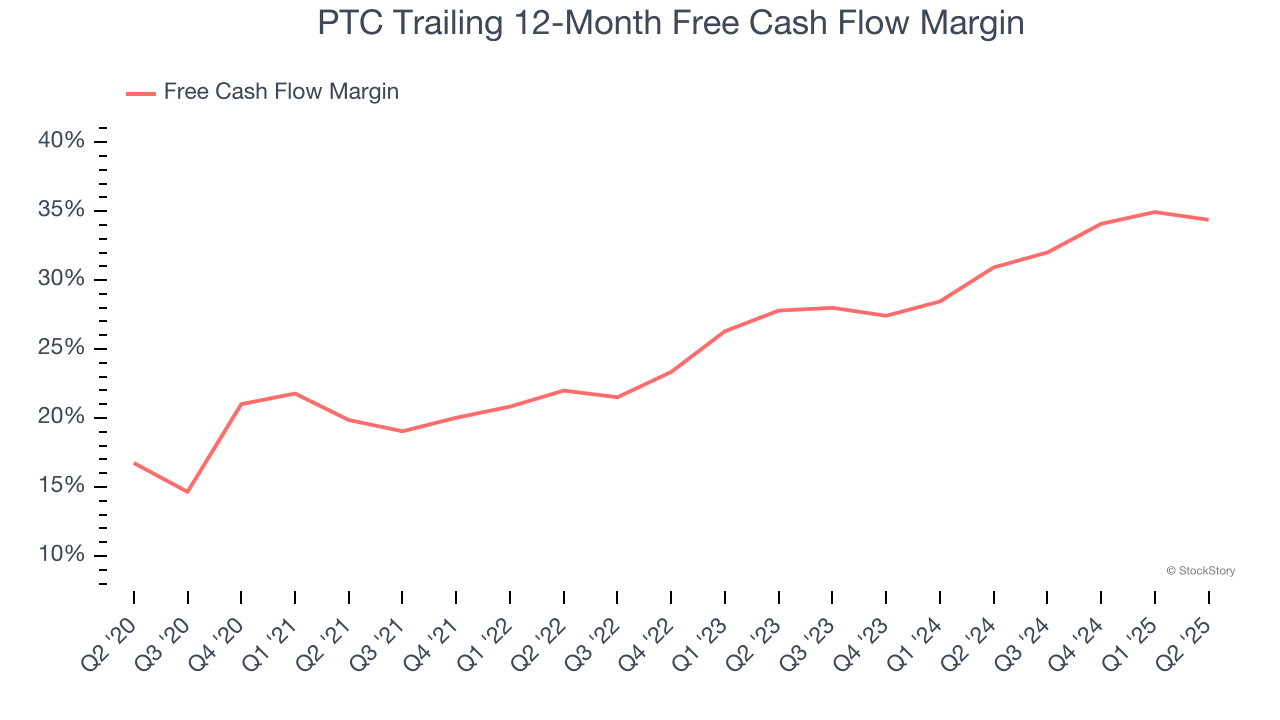

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

PTC has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the software sector, averaging an eye-popping 34.4% over the last year.

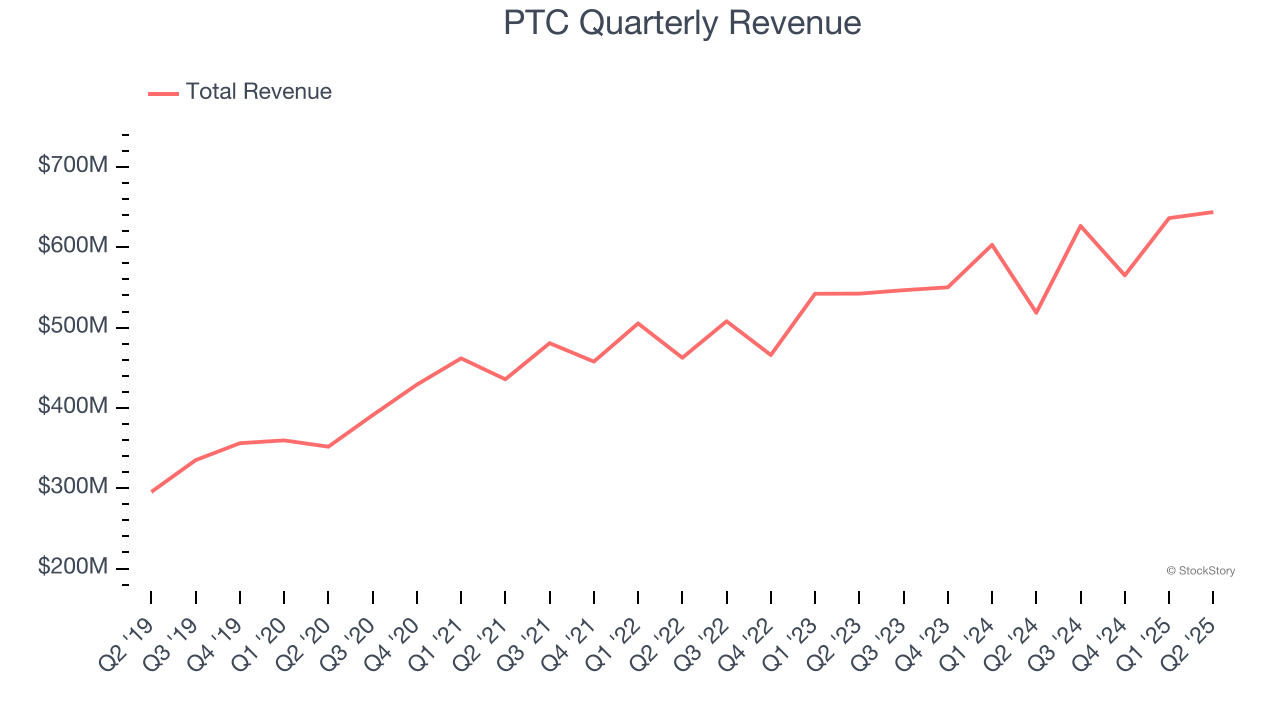

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, PTC’s sales grew at a sluggish 9.1% compounded annual growth rate over the last three years. This wasn’t a great result compared to the rest of the software sector, but there are still things to like about PTC.

PTC’s positive characteristics outweigh the negatives, and with its shares beating the market recently, the stock trades at 9.3× forward price-to-sales (or $212.96 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jun-11 | |

| Jun-11 | |

| Jun-10 | |

| Jun-10 | |

| May-28 | |

| May-21 | |

| May-13 | |

| May-12 | |

| May-07 | |

| May-06 | |

| May-06 | |

| May-06 | |

| May-06 | |

| May-06 | |

| May-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite