|

|

|

|

|||||

|

|

|

Alphabet operates in virtually all phases of the AI pipeline.

Google Cloud is Alphabet's fastest-growing segment.

Alphabet is the lowest-valued of the "Magnificent Seven" stocks.

There's no doubt that artificial intelligence (AI) has become a topic that's been virtually impossible to avoid over the past couple of years. Although it's not a new technology, the popularity of AI tools like ChatGPT has brought it to the mainstream.

Many companies dealing with AI have seen their stock prices surge due to investors rushing to take advantage of new growth opportunities. However, that has made many of these stocks inflated and overvalued.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

However, one stock that has shown promising AI growth, consistent profits, and a relatively low valuation is Alphabet (NASDAQ: GOOG)(NASDAQ: GOOGL). It's seemingly one of the best deals you can get from an AI stock right now.

Image source: Getty Images.

Although the focus on AI seems relatively new, Alphabet has been at the forefront of AI innovation for a while. It's responsible for many of the breakthroughs that have led to AI being what it is today. Alphabet is a full-stack AI company, meaning it operates in the three main phases of the pipeline.

Alphabet's subsidiary, DeepMind, is purely focused on AI research and development; its cloud platform, Google Cloud, allows it to provide scalable AI infrastructure for itself and other companies; and it has consumer-facing applications like its generative AI tool, Gemini.

Google Cloud will be a key part of Alphabet's AI growth in the near future. It's still third in market share behind Amazon Web Services (AWS) and Microsoft Azure, but it has been experiencing impressive growth. Google Cloud has also landed a six-year, $10 billion deal with Meta, making it the go-to platform to power Meta's AI ambitions.

Making money has never been a major problem for Alphabet, and its recent earnings show that's still the case. In the second quarter, Alphabet's revenue increased 14% year over year to $96.4 billion. Unsurprisingly, much of that came from its Google Services segment, which includes businesses like Google Search, YouTube ads, and Google subscriptions. Google Services revenue increased 12% year over year to $82.5 billion.

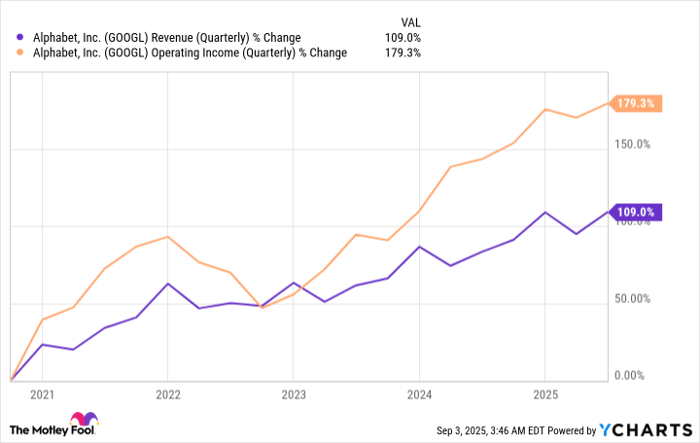

Alphabet's operating income (profit from core operations) also came in impressively, growing from $27.4 billion in the second quarter last year to $31.3 billion in this year's second quarter. Over the past five years, Alphabet's revenue and operating income have more than doubled.

GOOGL Revenue (Quarterly) data by YCharts

The most impressive growth -- and what most investors had their eyes on -- came from Google Cloud. Its revenue increased 32% year over year to $13.6 billion and was Alphabet's fastest-growing segment. Google Cloud is a business that should continue to be high-growth, as many companies flock to the platform for AI infrastructure.

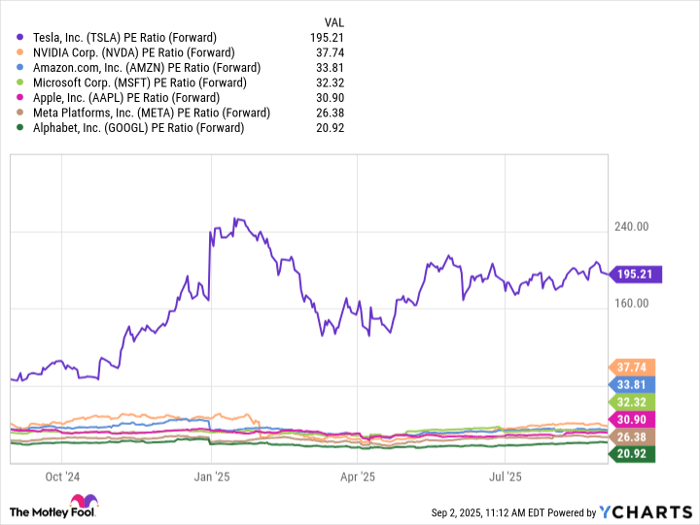

A stock's price by itself won't tell you whether or not it's valued low; instead, you should compare metrics to similar companies. In Alphabet's case, it's helpful to compare its price-to-earnings (P/E) ratio to other "Magnificent Seven" stocks.

When looking at Alphabet's forward P/E ratio -- which tells you how much you're paying per dollar of a company's expected earnings over the next 12 months -- it seems to be fairly low valued. Its forward P/E ratio is around 20.9 at the time of writing.

TSLA PE Ratio (Forward) data by YCharts

Given Alphabet's market position (especially Google), its profits, and growth prospects, its current valuation seems like a steal for long-term investors. There's also the company's dividend, which it first began paying last year, that can help hedge against some of the volatility that we've seen from growth and tech stocks in recent times.

Alphabet's current dividend yield is only around 0.40%, but Alphabet has the cash flow to make increasing the annual dividend a priority -- and that's what I expect to happen. It's not a foolproof investment, but the upside far outweighs the downside.

Before you buy stock in Alphabet, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $670,781!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,023,752!*

Now, it’s worth noting Stock Advisor’s total average return is 1,052% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Stefon Walters has positions in Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 3 min | |

| 12 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 6 hours | |

| 6 hours | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite