|

|

|

|

|||||

|

|

|

The adoption of AI tools in the cybersecurity market is increasing at a healthy pace, and Zscaler is building a solid revenue pipeline thanks to this technology.

AI chips are in great demand, which makes Micron Technology a terrific buy considering its phenomenal pace of growth.

Artificial intelligence (AI) stocks turned out to be big winners for investors in the past few years as the proliferation of this technology has allowed several companies to unlock new growth avenues, helping them boost their revenue and earnings at a healthy pace.

The good part is that AI adoption still has a long way to go. That's not surprising as companies using generative AI solutions are reportedly witnessing a return of 3.7 times for every dollar they spent on this technology. With the global economy expected to get a 15% boost thanks to AI in the long run, the adoption of this technology is likely to gain more momentum.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

That's why it would be a good idea to take a closer look at two AI stocks benefiting from improving AI adoption in different industries and that seem well placed to deliver healthy gains to investors in the long run.

Image source: Getty Images.

The cybersecurity-focused AI market is expected to grow by almost fourfold by 2030, generating $94 billion in annual revenue at the end of the decade. Zscaler (NASDAQ: ZS) gives investors an opportunity to capitalize on this opportunity.

The company is not only integrating AI-powered tools into its cybersecurity platform, but is also offering services that can help organizations secure their AI assets. The good part is that Zscaler's AI services are gaining solid traction among customers. This is evident from the fact that 27% of the new business that the company got in fiscal 2025 was from its emerging products.

These emerging products include several AI-focused tools, which help secure large language models (LLMs) and applications and give organizations access to AI virtual assistants to simplify their cybersecurity operations. It recently launched Zscaler AI Guard, a platform that's supposed to "stop attacks, protect sensitive data, and ensure regulatory compliance, enabling businesses to adopt AI securely."

The improving demand for Zscaler's AI tools is the reason why the company reported a solid set of results recently. Zscaler's revenue for the fourth quarter of fiscal 2025 (which ended on July 31) increased 21% year over year to $719 million. Its non-GAAP net income jumped by almost 24%. The company ended the year with a 26% increase in adjusted earnings to $3.28 per share.

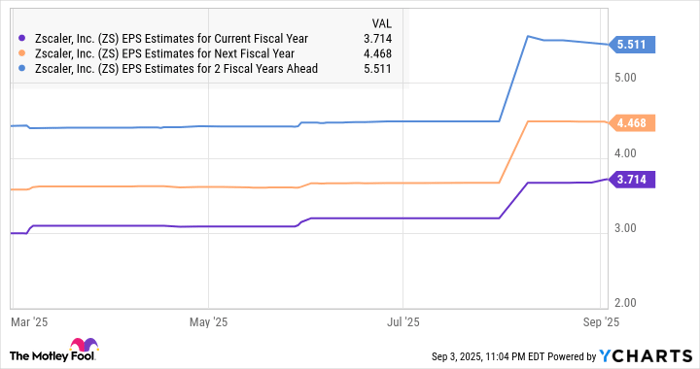

There is a good chance that its rate of earnings growth will accelerate in the future. That's because Zscaler's revenue pipeline is growing at a much faster pace than its revenue. The company's remaining performance obligations (RPO) jumped by 31% year over year in the previous quarter to $5.8 billion, exceeding the 23% jump in the company's annual revenue to $2.67 billion.

Zscaler, therefore, has a much stronger revenue pipeline going forward as RPO is the total value of a company's contracts that it has yet to fulfill at the end of a period. This explains why the company's bottom-line growth is expected to get better.

ZS EPS Estimates for Current Fiscal Year data by YCharts

Zscaler stock has shot up 50% in 2025. Its 12-month median price target of $321 points toward another jump of 19%. This cybersecurity stock, however, can sustain its bull run and do better than that considering the healthy improvement in its revenue pipeline that's likely to translate into stronger earnings growth.

Chipmakers such as Nvidia, Advanced Micro Devices, and Broadcom have been helping customers train LLMs and run AI inference applications in data centers, and Micron Technology (NASDAQ: MU) is playing a central role in helping these companies design powerful chip systems capable of tackling AI workloads.

Micron designs and manufactures high-bandwidth memory that goes into the graphics processing units (GPUs) and custom chips designed by chipmakers. HBM allows data center chips to transfer huge amounts of data at high speeds while keeping energy consumption in check. These characteristics are critical for tackling AI workloads in servers. Not surprisingly, chip designers have been looking to integrate higher amounts of HBM into their AI chips.

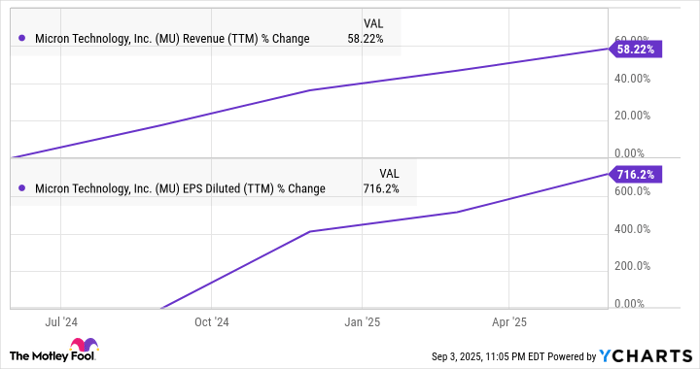

Micron is a direct beneficiary of soaring HBM demand. Its revenue and earnings jumped at an incredible pace in recent quarters.

MU Revenue (TTM) data by YCharts

That trend is likely to continue because of a couple of reasons.

First, the HBM market's revenue is expected to hit a massive $130 billion in 2030. That would be a huge increase over the $4 billion revenue that the HBM market generated in 2023.

Second, Micron seems to be capturing a bigger share of the market. Its HBM revenue increased by over 50% on a sequential basis in the past couple of quarters, and Morningstar estimates that the company could end fiscal 2025 with a 20% share of this market. Even better, Morningstar estimates that Micron's high-bandwidth memory revenue could increase by sixfold over the next five years, hitting $30 billion by 2030.

Throw in Micron's catalysts in the generative AI smartphone and personal computer markets, and it won't be surprising to see the company exceeding Wall Street's growth expectations going forward.

So, investors can consider buying Micron stock right away as its median price target of $154 points toward a potential jump of 30% over the next year. The stock has already gained 40% in 2025, and the rapid pace of its growth should ensure that its bull run continues.

Before you buy stock in Micron Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $670,781!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,023,752!*

Now, it’s worth noting Stock Advisor’s total average return is 1,052% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Nvidia, and Zscaler. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

| 4 hours | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite