|

|

|

|

|||||

|

|

|

CommScope Holding Company, Inc. COMM and Arista Networks, Inc. ANET are leading players in the networking infrastructure market. CommScope provides comprehensive networking solutions designed to support wireline and wireless network convergence, which are essential for the success of 5G technology. Its product portfolio has been specifically designed to help global service providers efficiently deploy fiber networks.

Conversely, Arista offers one of the broadest product lines of data center and campus Ethernet switches and routers in the industry. It provides routing and switching platforms with industry-leading capacity, low latency, port density and power efficiency.

Both CommScope and Arista are strategically positioned in the infrastructure market with overlapping relevance in networking infrastructure, enterprise IT solutions and cloud/data-center ecosystems. Let us delve a little deeper into the companies’ competitive dynamics to understand which of the two is relatively better placed in the industry.

CommScope continues to benefit from stringent cost-cutting measures and a focus on core operations. The company is actively pruning its non-core businesses while focusing on inorganic growth to boost its portfolio strength and remain at the forefront of technological innovation by developing solutions to support wireline and wireless network convergence.

The company has completed the divestiture of its Home Networks business to Vantiva SA (formerly Technicolor SA) to focus more on core operations. CommScope has further strengthened its portfolio by acquiring Casa Systems' Cable Business assets. The acquisition enhanced CommScope’s market-leading position in Access Network Solutions. It bolstered its virtual CMTS (Cable Modem Termination Systems) and PON (Passive Optical Network) product offerings, bringing significant synergies to the company’s operations. This move aligned with CommScope's strategy to expand its technological capabilities and customer base, especially in the domain of cloud-native network solutions.

Moreover, CommScope has revolutionized the way network operators scale their operations by launching the HX6-611-6WH/B antenna, which provides a high-capacity microwave backhaul solution to meet future network demands. By operating seamlessly in both the 6 GHz and 11 GHz bands, the HX6-611-6WH/B ensures reliable, long-haul connectivity, making it a critical asset for mobile network operators looking to future-proof their infrastructure.

However, CommScope sees fierce competition in each of its served markets. It is facing stiff competition from industry giants like Amphenol Corporation APH and Corning Incorporated GLW. The growing tension between the United States and China relating to trade restrictions imposed on the sale of communication equipment to China-based firms has dented the industry’s credibility, leading to a loss of business. Volatility in prices of raw materials and related components is also impacting the company’s profitability.

Arista holds a leadership position in 100-gigabit Ethernet switches and is increasingly gaining market traction in 200 and 400-gigabit high-performance switching products. It is witnessing solid demand trends among enterprise customers, backed by its multi-domain modern software approach, which is built upon its unique and differentiating foundation, the single EOS (Extensible Operating System) and CloudVision stack. Arista has made several additions to its multi-cloud and cloud-native software product family with CloudEOS Edge. It has introduced new cognitive Wi-Fi software that delivers intelligent application identification, automated troubleshooting and location services. The versatility of Arista’s unified software stack across various use cases, including WAN routing, campus and data center infrastructure, sets it apart from other competitors in the industry.

In addition to high capacity and easy availability, its cloud networking solutions promise predictable performance and programmability, enabling integration with third-party applications for network management, automation and orchestration.

The company boasts a comprehensive portfolio with the right network architecture for client-to-campus data center cloud and AI networking, backed by three guiding principles. These include best-in-class, highly proactive products with resilience, zero-touch automation and telemetry with predictive client-to-cloud one-click operations with granular visibility and prescriptive insights for deeper AI algorithms.

Arista is likely to benefit from its software-driven, data-centric approach, which helps customers build their cloud architecture and enhance the cloud experience they offer to their clients.

However, ANET remains plagued by high operating costs. Total operating expenses in second-quarter 2025 increased 13.8% year over year to $452.4 million, owing to a rise in headcount, product introduction costs and higher variable compensation expenditure. Moreover, the redesigning of products and their supply-chain mechanism has eroded margins. Although the company is witnessing increased demand, there are lingering supply bottlenecks for advanced products. Therefore, it is increasing orders for these components and trying to build up inventory, which is blocking working capital.

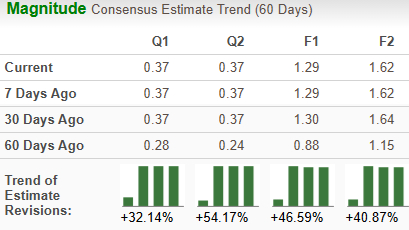

The Zacks Consensus Estimate for CommScope’s 2025 sales and EPS implies year-over-year growth of 11.2% and 4,400%, respectively. The EPS estimates have been trending northward (up 46.6%) over the past 60 days.

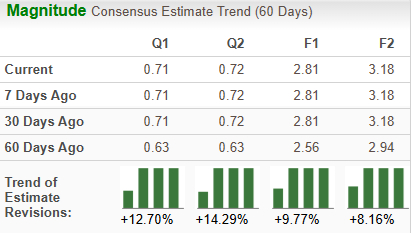

The Zacks Consensus Estimate for Arista’s 2025 sales and EPS implies year-over-year growth of 24.6% and 23.8%, respectively. The EPS estimates have been trending northward (up 9.8%) over the past 60 days.

Over the past year, COMM has skyrocketed 256.8% compared with the industry’s growth of 116%. Arista has surged 76% over the same period.

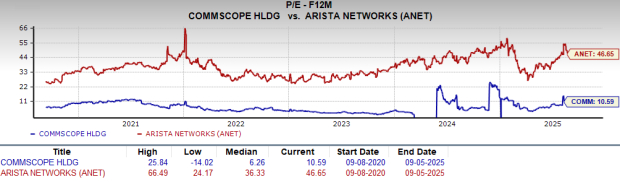

CommScope looks more attractive than Arista from a valuation standpoint. Going by the price/earnings ratio, CommScope’s shares currently trade at 10.59 forward earnings, significantly lower than Arista’s 46.65.

CommScope sports a Zacks Rank #1 (Strong Buy), while Arista carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Both companies expect their sales and profits to improve in 2025. Long-term earnings growth expectations for COMM and ANET are 23.8% and 16.6%, respectively. CommScope has a better price performance and estimate revisions compared with Arista, and is relatively cheaper in terms of the valuation metric. Arista has shown steady revenue and EPS growth for the past few years, while CommScope has been facing a bumpy road. However, CommScope seems to hold an edge compared with most operating metrics and appears to be a better investment option at the moment.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 7 hours | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 | |

| Mar-24 | |

| Mar-24 | |

| Mar-18 | |

| Mar-18 | |

| Mar-17 | |

| Mar-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite