|

|

|

|

|||||

|

|

|

Alphabet had easier remedies for its Google Search subsidiary in its monopoly court case.

The company now faces challenges in AI, in which it is competing well.

Even at an all-time high share price, the stock still looks cheap.

The tide seems to have turned for Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL). The parent company of Google saw its stock dip above $140 in April of this year over concerns about tariffs, antitrust cases both in the U.S. and in Europe, and rising competition for a share of the online search market from artificial intelligence (AI) startups. But since then, the stock has been on an absolute tear, hitting an all-time high of $238.13 in recent trading (a 70% jump).

While there is still the risk that tariffs cripple the global economy, Alphabet has shown strength with its new AI tools in 2025 as a leader in an industry not as affected by tariff actions. Last week, Alphabet's Google Search cash cow dodged a bullet when antitrust court-enforced remedies were outlined that are expected to be much burdensome than some analysts predicted.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

After what ended up being a big antitrust win for Google, should you buy Alphabet stock, even though it is trading near all-time highs?

Image source: Getty Images.

After Google Search was ruled by a U.S. court in 2024 to be a monopoly, investors had to wait patiently to see what remedies the judge would determine were needed for the business going forward. Proposed remedies from prosecutors included forcing Alphabet to sell off its Chrome browser and Android mobile operating system, which have dominant market shares and help retain users on Google Search instead of switching to competitors.

A huge part of Google's strategy to keep people using Google Search is building an ecosystem of platforms around the product, making it nearly impossible for competitors to budge their way in. The Chrome browser has an estimated 70% share of the browser market, which keeps people defaulting to Google for search queries. The same strategy is employed with Android for the mobile search market.

This week, the court ultimately did not force Alphabet to sell either of these platforms, instead ordering that Google share certain search data with qualified competitors. The court also prohibited exclusive search distribution agreements, though Google can still pay partners to feature its services. Additionally, it will have to submit to compliance monitoring for the next six years by an oversight committee. For Alphabet shareholders, it was the equivalent of dodging a bullet. The ecosystem of products (including Chrome and Android) that keep people using Google Search will remain in place.

Why did the court not resort to harsher remedies? Apparently, it factored in the rising threat that AI services pose to the traditional search engine market in the past few years. Effectively, it thinks AI provides a level of competition that should hamper Google from enacting monopolistic actions.

Oddly enough, AI is now the main threat facing Alphabet's business today, but it is also a potential opportunity for the company.

With the antitrust pressures easing for Alphabet, it can now sharpen its focus on AI. Rising competitors in the chatbot market include OpenAI, Anthropic, and Perplexity, businesses with services that are looking to steal a share of search queries from Google. Outside of macroeconomic fears or antitrust concerns, these competitors are the main worry that held down Alphabet stock in the past year.

In 2025, Alphabet has risen to this AI challenge. Its Gemini chatbot is growing rapidly and catching up to ChatGPT, with benchmark performance that leads the industry. Along with chatbots, Alphabet has deployed dozens of new AI tools across Google Search, YouTube, and other consumer services it owns. It is able to do so at such a large scale because of its internal data center infrastructure. The competition needs to go to third-party cloud providers to train and deploy its AI tools, a key difference that should give Alphabet a competitive advantage in AI over the long haul.

Speaking of cloud computing, Alphabet is one of these major infrastructure players powering these startups, which is another way the company should benefit from AI. Last quarter, Google Cloud was Alphabet's fastest-growing business with revenue up 32% year over year to $13.6 billion. It is now highly profitable, with 20% operating margins.

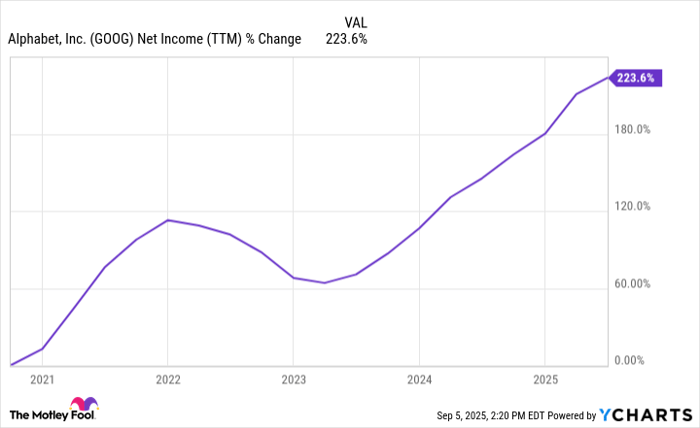

Data by YCharts.

Alphabet stock trades near an all-time high. Despite this, the stock does not look expensive because of how fast its earnings are growing. Net income is up a cumulative 224% in the last five years, leading its price-to-earnings ratio (P/E) to a reasonable level of 25. Google Search revenue is currently growing 12% year over year despite these AI threats, with the entire Google Services division posting an operating margin of 40%.

Growth opportunities abound for Alphabet in cloud computing, its Gemini chatbot, and even YouTube. Don't forget moonshot bets -- such as Waymo -- that are growing rapidly as well. Value investors might think it's a bad idea to buy a stock that just hit an all-time high, but Alphabet's continued business momentum still makes it a good buy-and-hold investment after this landmark antitrust decision.

Before you buy stock in Alphabet, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $670,781!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,023,752!*

Now, it’s worth noting Stock Advisor’s total average return is 1,052% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 8, 2025

Brett Schafer has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet. The Motley Fool has a disclosure policy.

| 5 min | |

| 11 min | |

| 56 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite