|

|

|

|

|||||

|

|

|

Let’s dig into the relative performance of Progressive (NYSE:PGR) and its peers as we unravel the now-completed Q2 property & casualty insurance earnings season.

Property & Casualty (P&C) insurers protect individuals and businesses against financial loss from damage to property or from legal liability. This is a cyclical industry, and the sector benefits when there is 'hard market', characterized by strong premium rate increases that outpace loss and cost inflation, resulting in robust underwriting margins. The opposite is true in a 'soft market'. Interest rates also matter, as they determine the yields earned on fixed-income portfolios. On the other hand, P&C insurers face a major secular headwind from the increasing frequency and severity of catastrophe losses due to climate change. Furthermore, the liability side of the business is pressured by 'social inflation'—the trend of rising litigation costs and larger jury awards.

The 33 property & casualty insurance stocks we track reported a satisfactory Q2. As a group, revenues beat analysts’ consensus estimates by 1.5%.

In light of this news, share prices of the companies have held steady as they are up 4.4% on average since the latest earnings results.

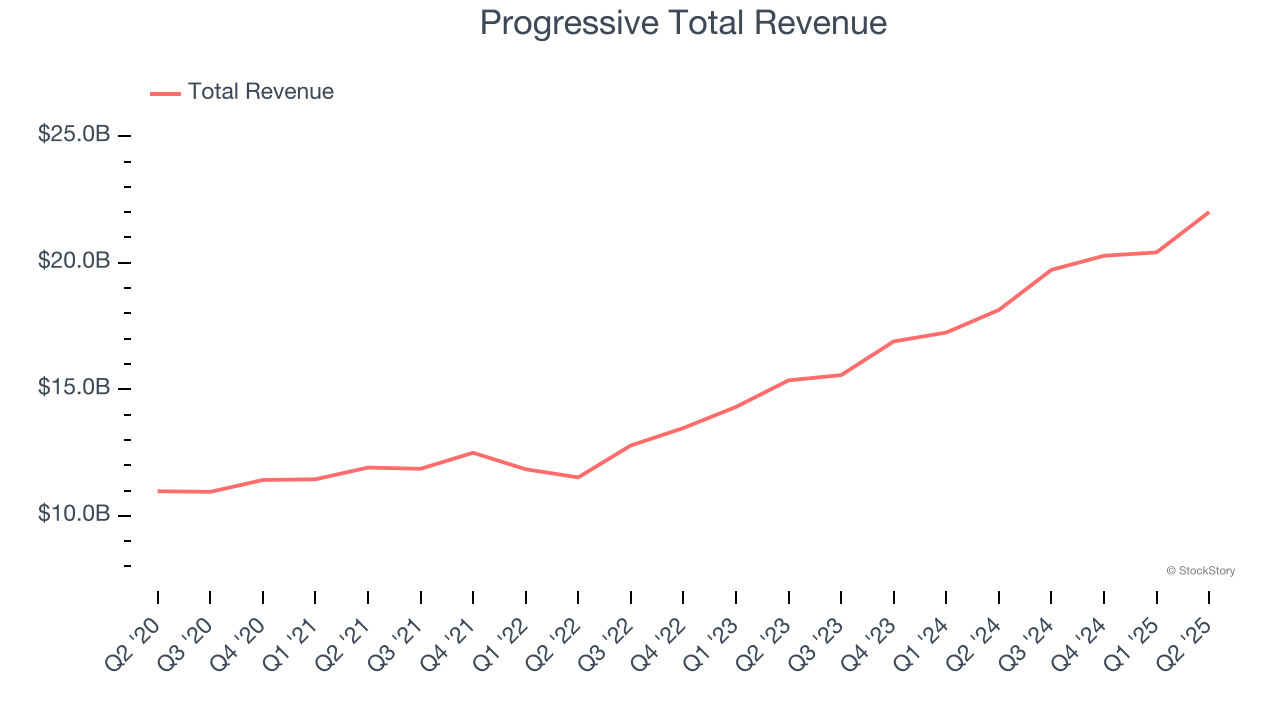

Starting as a small auto insurance company in 1937 with a pioneering focus on high-risk drivers, Progressive (NYSE:PGR) is a major auto, property, and commercial insurance provider that offers policies through independent agents, online platforms, and over the phone.

Progressive reported revenues of $22 billion, up 21.3% year on year. This print exceeded analysts’ expectations by 1.4%. Overall, it was a strong quarter for the company with a solid beat of analysts’ book value per share estimates and a beat of analysts’ EPS estimates.

The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $243.05.

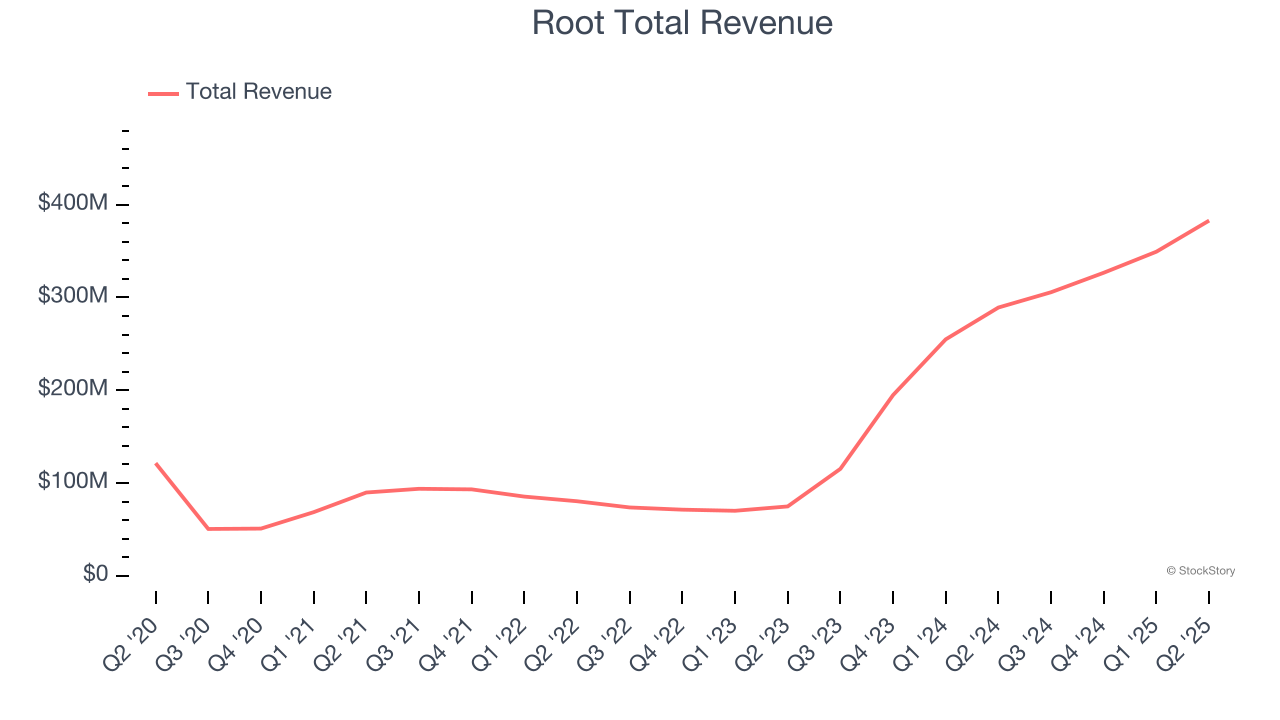

Pioneering a data-driven approach that rewards good driving habits, Root (NASDAQ:ROOT) is a technology-driven auto insurance company that uses mobile apps to acquire customers and data science to price policies based on individual driving behavior.

Root reported revenues of $382.9 million, up 32.4% year on year, outperforming analysts’ expectations by 7.5%. The business had an incredible quarter with a beat of analysts’ EPS and net premiums earned estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 20.1% since reporting. It currently trades at $98.40.

Is now the time to buy Root? Access our full analysis of the earnings results here, it’s free.

Founded in 1926 during the early days of automobile insurance, Selective Insurance Group (NASDAQ:SIGI) is a property and casualty insurance company that sells commercial, personal, and excess and surplus lines insurance products through independent agents.

Selective Insurance Group reported revenues of $127.9 million, down 89.3% year on year, falling short of analysts’ expectations by 90.3%. It was a disappointing quarter as it posted a miss of analysts’ EPS and book value per share estimates.

Selective Insurance Group delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 11.8% since the results and currently trades at $79.81.

Read our full analysis of Selective Insurance Group’s results here.

Founded in the aftermath of the 2008 housing crisis to bring new capacity to the mortgage insurance market, NMI Holdings (NASDAQ:NMIH) provides mortgage insurance that protects lenders against losses when homebuyers default on their mortgage loans.

NMI Holdings reported revenues of $173.8 million, up 7.2% year on year. This result met analysts’ expectations. Taking a step back, it was a slower quarter as it produced net premiums earned in line with analysts’ estimates and a narrow beat of analysts’ EPS estimates.

The stock is up 4.8% since reporting and currently trades at $39.77.

Read our full, actionable report on NMI Holdings here, it’s free.

Founded in 2013 to fill gaps in catastrophe insurance markets, Palomar Holdings (NASDAQ:PLMR) is a specialty insurance provider that offers property and casualty insurance products in underserved markets, with a focus on earthquake coverage.

Palomar Holdings reported revenues of $203.3 million, up 55.1% year on year. This print topped analysts’ expectations by 9.2%. It was a strong quarter as it also produced an impressive beat of analysts’ net premiums earned estimates.

Palomar Holdings pulled off the fastest revenue growth among its peers. The stock is down 8.4% since reporting and currently trades at $120.75.

Read our full, actionable report on Palomar Holdings here, it’s free.

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 22 min | |

| 14 hours | |

| Feb-27 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite