|

|

|

|

|||||

|

|

|

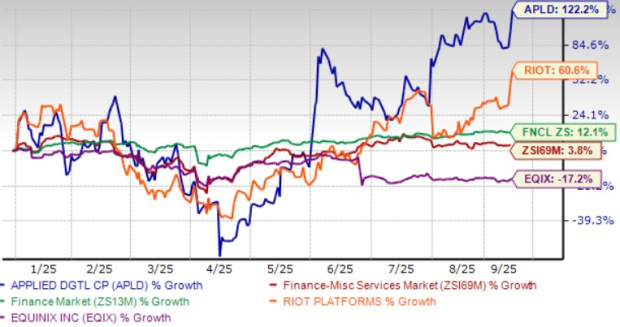

Applied Digital APLD shares have appreciated 122.2% year to date (YTD) compared with the broader Zacks Finance sector’s return of 12.1% and the Zacks Financial – Miscellaneous Services industry’s return of 3.8%. APLD shares have outperformed close peers, including Riot Platforms RIOT and Equinix EQIX, over the same time frame. While Riot Platforms’ shares have returned 60.6%, Equinix’s have dropped 17.2%.

The outperformance can be attributed to Applied Digital’s strong prospects. Robust demand for data center infrastructure and growing focus on energy efficiency are noteworthy developments in the data center industry. The global market for AI is expected to reach $500 billion by 2027, driven by increasing adoption across various industries, including healthcare, finance, transportation, and manufacturing. AI needs data centers with high power density, as well as changing power and cooling requirements.

Moreover, strong spending by hyperscalers, which is expected to exceed $350 billion in 2025, bodes well for APLD. Hyperscalers require high-capacity data centers to meet the escalating power needs of AI and GPU-driven applications. These factors bode well for APLD’s future prospects.

However, are the positive industry trends enough for the investors to jump into APLD? Let’s find out.

Applied Digital’s Data Center Hosting business provides energized infrastructure services to crypto mining customers. The company currently operates sites in Jamestown and Ellendale, ND, with a total hosting capacity of approximately 286 megawatts (MWs). The HPC Hosting business specializes in designing, constructing, and operating data centers that are well-equipped to support high-power density applications like high-performance computing (HPC) and AI.

The HPC Hosting business is expected to drive top-line growth over the long term. APLD’s Polaris Forge 1 is purpose-built for AI and HPC. The facility is designed to scale up to 1 gigawatt (GW). The first 100-MW facility is scheduled to be operational in the fourth quarter of 2025, the second 150-MW facility is set to come online in mid-2026, and the third 150-MW facility is planned for 2027.

Polaris Forge 1 will help Applied Digital offer reliable, power-dense solutions and become a leader in designing and building AI factories. AI Queries require 15 times the electricity of traditional queries, and racks now exceed 50 kilowatts. However, less than 10% of facilities can support this density, which offers a significant growth opportunity for Applied Digital.

APLD has inked three lease agreements (15-year base term with three five-year options) with CoreWeave CRWV to deliver 400 MW of critical IT load at Polaris Forge 1. Total anticipated contracted lease revenues from the CoreWeave deal are now expected to be roughly $11 billion. The CoreWeave partnership validates Applied Digital's strategic pivot from cryptocurrency mining to AI-optimized data center infrastructure. This partnership provides strong revenue visibility and effectively de-risks Applied Digital's business model.

Applied Digital currently has a single customer — Marathon Digital — under the Data Center Hosting business. APLD reported fiscal 2025 revenues of $144.2 million, up 6% from fiscal 2024, with Data Center Hosting contributing the majority.

The HPC Hosting currently has one customer and is expected to generate revenues once Polaris Forge 1 becomes operational, which is expected in late calendar year 2025.

The Zacks Consensus Estimate for APLD’s fiscal 2026 loss is currently pegged at 34 cents per share, which has widened by 13 cents over the past 30 days. The company reported a loss of 80 cents per share in fiscal 2025.

Applied Digital Corporation price-consensus-chart | Applied Digital Corporation Quote

The consensus mark for APLD’s first-quarter fiscal 2026 loss is currently pegged at 11 cents per share, which has widened by a nickel over the past 30 days. The company reported a loss of 3 cents per share in the year-ago quarter.

APLD stock is currently overvalued, as suggested by the Value Score of F.

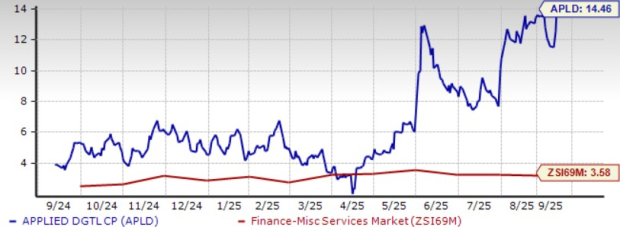

The stock is trading at a premium, with a forward 12-month price/sales of 14.46X compared with the industry’s 3.58X, Riot Platforms’ 7.89X and Equinix’s 7.79X.

Applied Digital is benefiting from the growing demand for AI infrastructure. The CoreWeave lease deal improves revenue visibility, which bodes well for long-term investors. However, the near-term prospect is murky given rising loss estimates. This, along with a stretched valuation, makes the stock a risky bet.

Applied Digital currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable time to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 min | |

| 3 hours | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite