|

|

|

|

|||||

|

|

|

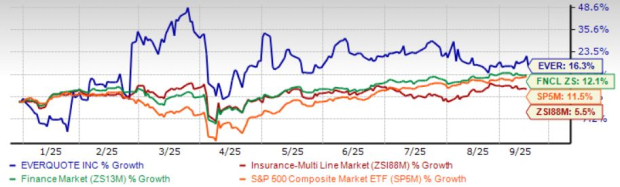

Shares of EverQuote, Inc. EVER have gained 16.3% year to date, outperforming its industry, the Finance sector and the Zacks S&P 500 Composite of 5.5%, 12.1% and 11.5%, respectively.

The insurer has a market capitalization of $848.9 million. The average volume of shares traded in the last three months was 0.5 million.

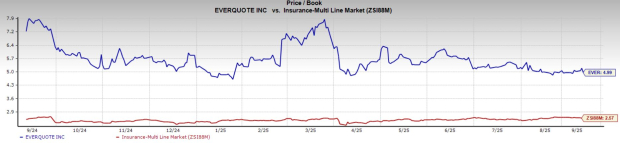

Shares of EVER are trading at a premium to the Zacks Multi line industry. Its price-to-book value of 4.94X is higher than the industry average of 2.05X.

However, shares of other multi-line insurers, such as MGIC Investment Corporation MTG, Assurant, Inc. AIZ, are trading at a discount to the industry, while shares of Lemonade, Inc. LMND are trading at a premium.

The Zacks Consensus Estimate for EVER’s 2025 earnings per share is pegged at 1.31, and the consensus estimate for revenues is pegged at $648.5 million.

The consensus estimate for 2026 earnings per share and revenues indicates a rise of 18.3% and 10.6%, respectively, from the corresponding 2025 estimates. EVER has an impressive Growth Score of A. This style score helps analyse the growth prospects of a company.

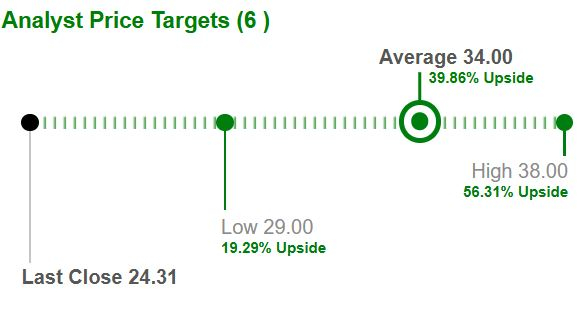

Based on short-term price targets offered by six analysts, the Zacks average price target is $34 per share. The average indicates a potential 39.86% upside from the last closing price.

The Zacks Consensus Estimate for 2025 earnings has moved up 3.15% in the past 30 days, while the same for 2026 has moved up 4.03% in the same time frame.

Return on equity (ROE) for the trailing 12 months was 36.9%, comparing favorably with the industry’s 14.8%. This reflects its efficiency in utilizing shareholders’ funds.

Return on invested capital in the trailing 12 months was 36.3%, better than the industry average of 2%, reflecting EVER’s efficiency in utilizing funds to generate income.

EverQuote is positioned for long-term growth, supported by its proprietary data platform, sharper focus on property and casualty markets, and leaner operations. Lower advertising costs, rising digital adoption in insurance, and a solid financial base further reinforce its growth prospects.

With auto carrier demand beginning to normalize, EverQuote is well-positioned to regain momentum in its core marketplace. The company expects third-quarter 2025 revenues of $163–$169 million, reflecting about 15% growth at the midpoint, and anticipates surpassing $1 billion in annual revenues soon. Revenue is projected to rise 28.8% in 2025. Its strong foothold in auto insurance provides a springboard for expansion into additional verticals, where higher consumer engagement and increased quote activity can further drive growth. At the same time, ongoing innovation in advertiser solutions should enhance monetization and deepen client relationships.

EverQuote has also authorized a $50 million share repurchase program, set to run through June 2026. This reflects management’s confidence in the company’s performance and cash position, while signaling a disciplined approach to capital use.

EverQuote plans to channel robust cash flow into AI, technology, and data initiatives, with a faster rollout scheduled for the second half of 2025 to sharpen efficiency and deepen its competitive moat. Building on this foundation, the company is enhancing its platform by combining proprietary data with in-house, third-party, and open-source tools to attract insurance shoppers from diverse channels. AI is being embedded across operations, from copilots and voice agents to automated workflows, while machine learning and data-driven automation are scaled to further strengthen efficiency and long-term growth.

Looking ahead, EverQuote has several pathways to sustain growth beyond its core auto marketplace. Expanding into non-auto categories, introducing new product offerings and pursuing selective acquisitions can diversify revenue streams. At the same time, leveraging its technology edge to attract high-intent consumers will strengthen its competitive position in the digital insurance space.

Despite recent progress, EverQuote continues to face notable headwinds. Rising expenses tied to marketing, operations, and technology weigh on margins, while larger carriers and rival platforms with stronger resources and brand recognition intensify competition in an already crowded marketplace.

Regulatory risk presents another challenge. Shifts in oversight can disrupt revenue streams, and the cost of meeting compliance standards adds further pressure. Any missteps could lead to penalties or enforcement actions, creating additional strain on profitability and long-term growth.

Overall, EverQuote demonstrates solid long-term potential through its data-driven platform, technology investments, and opportunities to expand beyond auto insurance. However, near-term challenges, including rising expenses, competitive pressures, and regulatory uncertainty, create a more cautious outlook.

Given its expensive valuation, it is better to wait for some more time before taking a call on this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite