|

|

|

|

|||||

|

|

|

Cloud computing giants are spending big on acquiring AI data center capacity.

This market is expected to generate $400 billion in revenue by 2028, and that's great news for this Nebius peer.

This Nebius alternative can increase its data center capacity at a faster pace, and it is trading at a significantly lower valuation.

Nebius Holdings (NASDAQ: NBIS) stock took off on Sept. 9, rising almost 50% in a single day after it emerged that the cloud artificial intelligence (AI) infrastructure provider has landed a massive contract with Microsoft (NASDAQ: MSFT) that's going to supercharge its growth for years to come.

For a company that has clocked $250 million in revenue in the past four quarters, the $19.4 billion contract from Microsoft that will run until 2031 is definitely a big deal. The tech giant has given Nebius such a lucrative deal to gain access to the latter's New Jersey data center. This is a dedicated AI data center powered by graphics processing units (GPUs), and Microsoft is going to use the same for handling AI workloads.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

However, Nebius is not the only dedicated AI cloud infrastructure company out there. There is another company that's been in fine form on the stock market this year, is growing at a solid pace, has a terrific backlog, and is cheaper than Nebius from a valuation perspective.

Let's take a closer look at that name and why it will be a good idea to buy it right away.

Image source: Getty Images.

CoreWeave (NASDAQ: CRWV) stock jumped more than 7% in the wake of the Nebius-Microsoft deal. It is easy to see why that was the case. Just like Nebius, CoreWeave also rents out its dedicated, GPU-powered data centers to customers looking to run AI and machine learning (ML) workloads.

The company points out that its AI infrastructure is purpose-built for AI, allowing its customers to reduce the time to market and improve efficiency and speed significantly. Not surprisingly, CoreWeave has witnessed remarkably solid demand for its AI infrastructure offerings, as is evident from the rapid growth in the company's revenue and backlog.

CoreWeave's top line jumped 207% in the second quarter of 2025 to $1.2 billion. But what's more impressive is its backlog worth $30.1 billion, which increased by nearly $14 billion from the year-ago quarter. CoreWeave's revenue backlog has doubled in the first half of 2025, thanks to the sizable contracts it has won from the likes of OpenAI and Google Cloud.

OpenAI has awarded CoreWeave contracts totaling $15.9 billion this year. CoreWeave has won business from new hyperscale and enterprise customers as well. Looking ahead, it won't be surprising to see CoreWeave's revenue backlog getting fatter. That's because major cloud computing providers are witnessing massive growth in their contractual obligations, and that's why they are tapping the likes of Nebius and CoreWeave to get their hands on more AI data center capacity.

Microsoft, for instance, saw its contracted remaining performance obligations (RPO) jump by 35% year over year in the previous quarter to a whopping $368 billion. The company credited this massive backlog to the robust demand for its cloud services. This makes it clear why the tech giant decided to turn to Nebius to unlock more capacity so that it can fulfill the heavy AI computing demand that it is witnessing.

An important thing worth noting here is that Microsoft is CoreWeave's largest customer, accounting for 62% of its top line in 2024. Meta Platforms and IBM are some of its other customers, and CoreWeave has also brought OpenAI on board this year. Given that the company sees its addressable market hitting $400 billion by 2028, investors can expect it to sustain its healthy growth levels in the long run, especially considering its focus on bringing more capacity online.

CoreWeave operated 33 AI data centers in North America and Europe at the end of the previous quarter with an active power capacity of 470 megawatts (MW). The company plans to end the year with 900 MW of active data center capacity. What's more, its contracted data center capacity of 2.2 gigawatts (GW) indicates that it can substantially ramp up its capacity in the long run.

Contracted power refers to the data center capacity that CoreWeave can bring online by deploying compute, networking, and storage equipment, which will turn the contracted capacity into active capacity. What's worth noting here is that CoreWeave's active capacity was well above Nebius' 220 MW at the end of the previous quarter. Additionally, its contracted capacity is much higher than that of Nebius, which expects to have 1 GW of contracted capacity by the end of next year.

So, CoreWeave is ahead of Nebius as far as capacity is concerned. Throw in a more attractive valuation, and it's easy to see why CoreWeave has the potential to fly higher in the future.

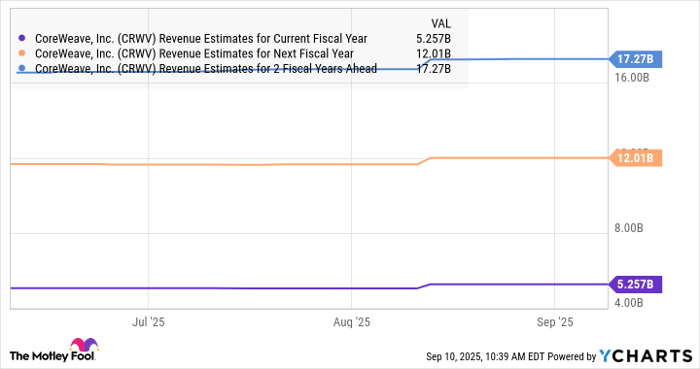

Consensus estimates are projecting red-hot growth in CoreWeave's revenue.

CRWV Revenue Estimates for Current Fiscal Year data by YCharts

Its outstanding backlog and the size of its total addressable market can indeed allow it to more than triple its top line in the space of just two years, as seen in the chart above. This makes CoreWeave an attractive buy since it is trading at less than 14 times sales, a massive discount to Nebius' price-to-sales ratio of 91.

Even if CoreWeave trades at 5 times sales (in line with the Nasdaq Composite index's multiple) after three years and achieves $17 billion in revenue, its market cap could jump to $85 billion. That points toward a 73% jump from current levels, though stronger gains cannot be ruled out.

Before you buy stock in CoreWeave, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CoreWeave wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $649,037!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,086,028!*

Now, it’s worth noting Stock Advisor’s total average return is 1,056% — a market-crushing outperformance compared to 188% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 8, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends International Business Machines, Meta Platforms, and Microsoft. The Motley Fool recommends Nebius Group and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 53 min | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Microsoft Stock Slopes Down To Lowest Point in Months; Is The Stock A Buy Now?

MSFT

Investor's Business Daily

|

| Feb-17 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite