|

|

|

|

|||||

|

|

|

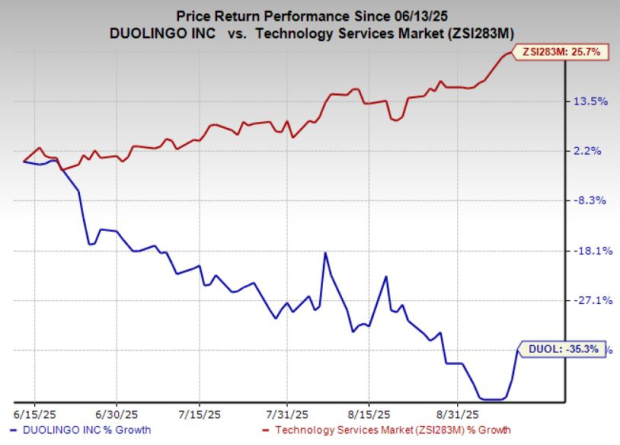

Duolingo, Inc. DUOL has been facing heavy selling pressure, sliding 35% over the past three months. This sharp decline stands out when compared to the broader industry, which climbed 26% in the same period, and the Zacks S&P 500 composite, which advanced 11%. The performance gap highlights just how much Duolingo has lagged behind the market and its peers.

Meanwhile, competitors Coursera COUR and Chegg CHGG have been moving in the opposite direction. Coursera has surged 31% over the past three months, while Chegg has gained 18.5%. The contrasting trajectories of Coursera and Chegg versus Duolingo point to significant shifts in investor sentiment within the online learning space.

At the latest close, Duolingo’s stock price was $309.3, a steep 43% below its 52-week high of $251.3. This pullback raises the question: Is Duolingo setting up for a recovery, or could further weakness be ahead? With DUOL sliding while Coursera and Chegg are trending higher, you need to carefully weigh whether now is the right time to consider Duolingo.

Let us help you…

One of the strongest positives for Duolingo lies in how it is turning artificial intelligence and proprietary learner data into a competitive edge. Unlike many companies where AI remains a vague promise, Duolingo is embedding it directly into its product roadmap and financials. By using its massive learner dataset, the company can rapidly build and launch new verticals, such as music and chess, with a level of accuracy and personalization that competitors cannot easily replicate.

The efficiency of AI has also translated into cost advantages. In the most recent quarter, Duolingo raised its full-year outlook partly because AI-related expenses came in lower than anticipated. Gross margin rose sequentially by 130 basis points to 72.4%, a clear sign that innovation is not eroding profitability. Even more impressive is how quickly AI is accelerating content expansion. The company rolled out 148 new language courses in April, marking its largest expansion ever. To put this in perspective, it took over a decade to build the first 100 courses, but AI-driven efficiencies enabled nearly 150 in less than a year. This ability to scale course content rapidly translates into stronger user engagement, deeper brand trust, and ultimately, sustainable growth in bookings.

Another positive for Duolingo is the way it is building a multi-pronged revenue model that extends far beyond language learning subscriptions. The company has been successfully steering more users toward premium tiers, driving a 6% year-over-year increase in subscription ARPU through mix-shift rather than simple price hikes, a healthier form of monetization.

Optionality beyond languages is proving real. The launch of the Chess course, which quickly surpassed one million daily active users on iOS, demonstrates that Duolingo’s teaching model can scale into entirely new subjects. Early traction in Music and other categories only strengthens this case. Importantly, each new subject not only expands the addressable market but also increases user retention by giving learners more reasons to engage daily.

Financial guidance reflects this momentum with management projecting $1.011 to $1.019 billion in FY 2025 revenues and adjusted EBITDA margins approaching 29%. With about 36% revenue growth expected at the midpoint, Duolingo is balancing innovation with profitability, creating a compelling long-term investment profile.

A key measure of a company's profitability is its return on equity (ROE), which indicates how efficiently it uses shareholders' investments to generate earnings. At the end of the second quarter of 2025, DUOL's ROE stood at 13.3%, above the industry average of 6.7%. This suggests that Duolingo has been effective in investing in profitable areas, a point further supported by its return on invested capital, which is 9.1%, well above the industry average of 3.9%.

Duolingo's liquidity position is also robust, with a current ratio of 2.81 at the end of the second quarter of 2025 compared to the industry’s 1.78. A current ratio above 1 indicates that Duolingo is well-positioned to meet its short-term obligations, providing a buffer against potential financial challenges.

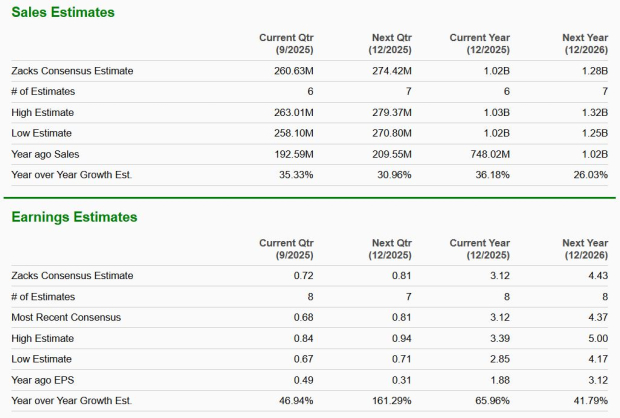

Looking ahead, the Zacks Consensus Estimate for Duolingo's 2025 earnings is set at $3.12, indicating an impressive 66% year-over-year increase. Earnings in 2026 are projected to increase 42% year over year. The company's sales are expected to grow 36% in 2025 and 26% in 2026, indicating strong top and bottom-line growth prospects.

This positive outlook is reinforced by upward estimate revisions. In the past 60 days, six estimates for 2025 earnings have been revised upwards, with no downward revisions, reflecting strong analyst confidence in the company. The Zacks Consensus Estimate for 2025 earnings has increased 7.6% during this period. Five estimates for 2026 earnings have been revised north, with no southward revisions. The Zacks Consensus Estimate for 2026 earnings has increased 5% during this period.

Duolingo presents a compelling buy opportunity. The company’s foundation of proprietary data and AI-driven efficiencies is enabling faster product rollouts, deeper engagement, and meaningful cost advantages. Beyond its core language offerings, Duolingo is proving its model works across new subjects, such as chess and music, broadening its market and strengthening retention. At the same time, it is diversifying revenue streams through premium subscriptions, advertising, and testing services, reducing reliance on a single driver. With strong liquidity, rising analyst confidence, and sustained growth prospects, Duolingo’s dip looks more like an entry point than a red flag.

DUOL currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 14 hours | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Jul-30 | |

| Jul-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite