|

|

|

|

|||||

|

|

|

Westamerica Bancorporation currently trades at $48.62 per share and has shown little upside over the past six months, posting a small loss of 5%. The stock also fell short of the S&P 500’s 15.9% gain during that period.

Is now the time to buy Westamerica Bancorporation, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

We don't have much confidence in Westamerica Bancorporation. Here are three reasons why WABC doesn't excite us and a stock we'd rather own.

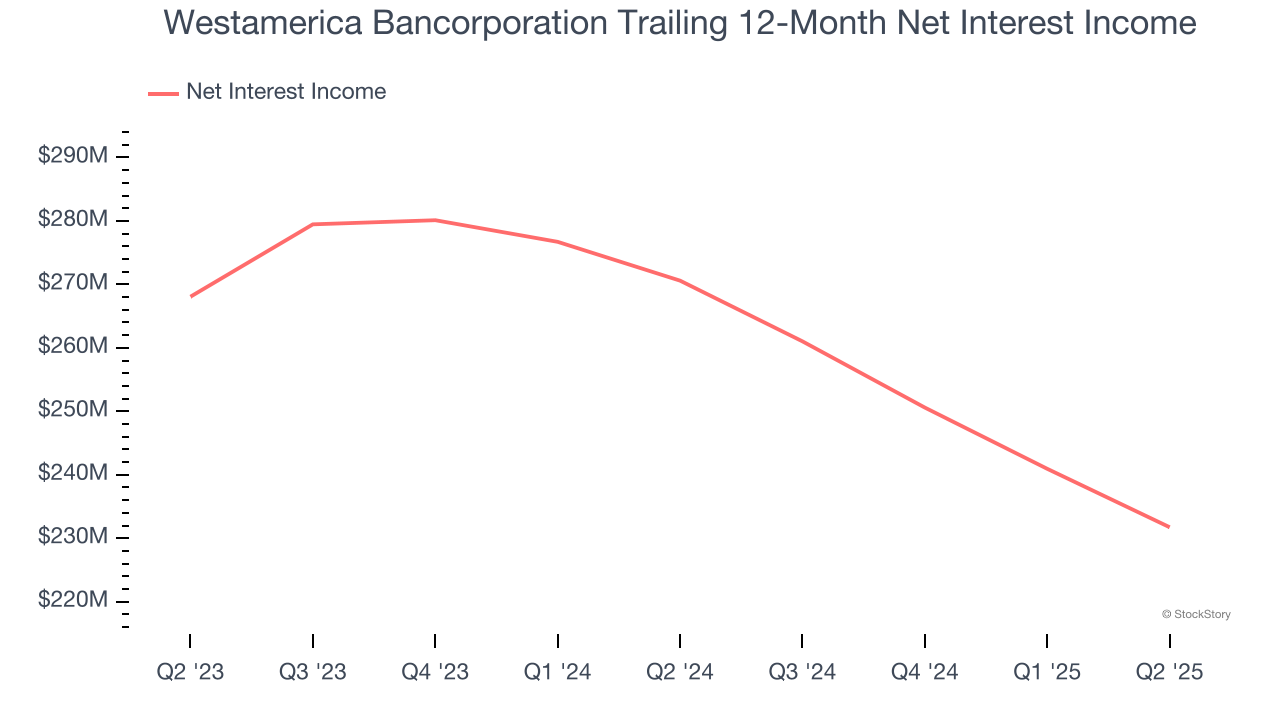

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Westamerica Bancorporation’s net interest income has grown at a 6.5% annualized rate over the last five years, slightly worse than the broader banking industry and in line with its total revenue.

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Westamerica Bancorporation’s net interest income to drop by 8.9%, a decrease from its 7% annualized declines for the past two years. This projection is slightly below its 7% annualized declines for the past two years.

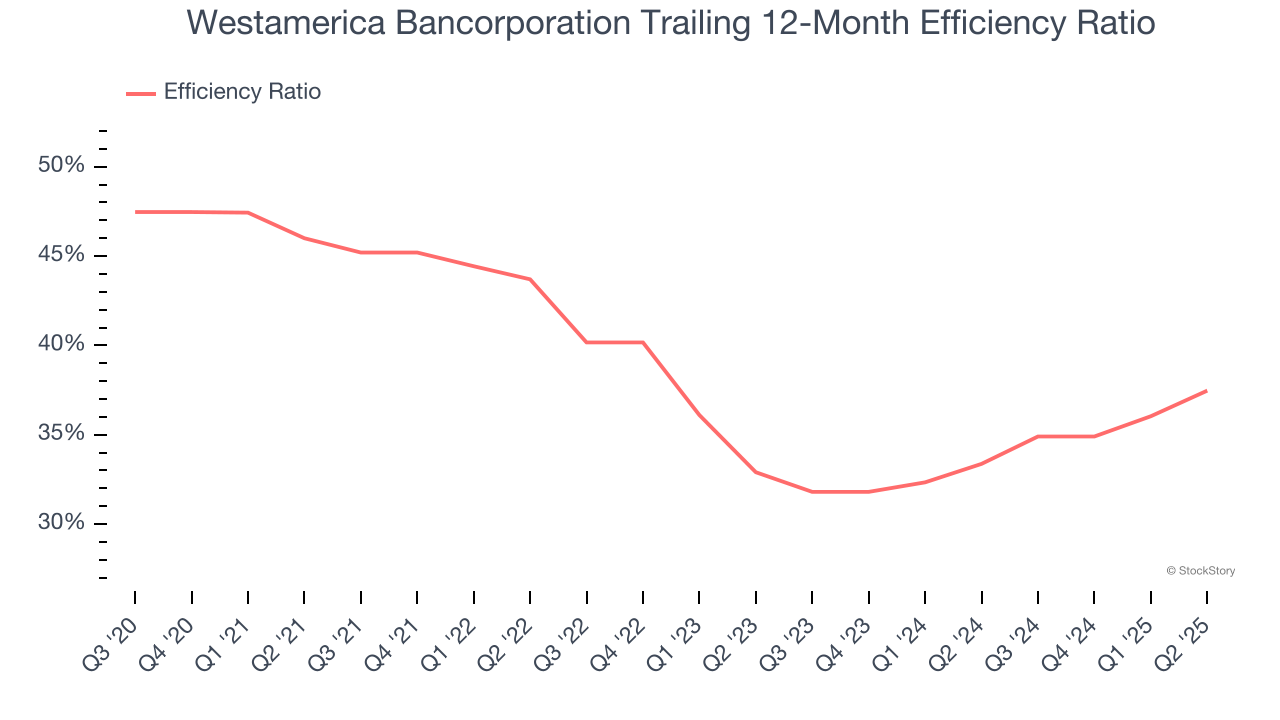

Topline growth is certainly important, but the overall profitability of this growth matters for the bottom line. For banks, we look at efficiency ratio, which is non-interest expense (salaries, rent, IT, marketing, excluding interest paid out to depositors) as a percentage of total revenue.

Investors focus on efficiency ratio changes rather than absolute levels, understanding that expense structures vary by revenue mix. Counterintuitively, lower efficiency ratios indicate better performance since they represent lower costs relative to revenue.

For the next 12 months, Wall Street expects Westamerica Bancorporation to become less profitable as it anticipates an efficiency ratio of 40.2% compared to 37.5% over the past year.

Westamerica Bancorporation’s business quality ultimately falls short of our standards. With its shares lagging the market recently, the stock trades at 1.3× forward P/B (or $48.62 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Apr-24 | |

| Apr-23 | |

| Apr-16 | |

| Apr-16 | |

| Apr-14 | |

| Feb-22 | |

| Feb-02 | |

| Jan-22 | |

| Jan-21 | |

| Jan-15 | |

| Jan-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite