|

|

|

|

|||||

|

|

|

Lululemon's sales are slowing in North America, but it is doing better than the competition.

Internationally, the brand is flourishing.

Shares of Lululemon look cheap after its massive stock price drawdown.

Things have gone from bad to worse for Lululemon (NASDAQ: LULU). Increased competition and changing consumer trends in the United States have triggered a major growth slowdown for the apparel brand, and the stock is now off close to 70% from all-time highs. At a price of $160, the stock is at one of its lowest levels in years.

Shareholders of Lululemon are feeling the pain. At the same time, its valuation is now close to its lowest level ever. Does that make Lululemon stock a slam-dunk buy below $170?

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Image source: Getty Images.

The core reason why Lululemon's stock has faltered is slowing growth in the United States and Canada. Americas revenue increased just 1% last quarter, with comparable-store sales growth at physical locations down 3% on a constant-dollar basis. Compared to its history, this is one of the worst periods revenue-wise for the brand in its home market.

Bears believe Lululemon is getting attacked by upstart brands such as Alo Yoga, Vuori, and Gymshark. However, since these brands are not publicly traded, observers do not know how fast (or not) they are growing. Investors can look at other competitors such as Nike, Adidas, and Athleta, which have publicly available information. Last quarter in North America, Nike's revenue declined by 11%, Adidas grew 8%, and Athleta's revenue declined by 9% year over year, all in constant U.S. dollar figures.

This is great context for Lululemon's position in North America. Athleta is the closest direct competitor to Lululemon, and its sales are doing much worse. Seeing these figures aligns with management's claims that Lululemon is gaining market share of the performance apparel category in the United States, making its 1% growth rate much more palatable for investors.

Internationally, the activewear category is in a much better position, as a rising tide lifting all boats. As Lululemon grows its reach in new countries, it is seeing impressive revenue growth figures.

China revenue grew 24% year over year on a constant-dollar basis last quarter, and revenue outside of China and North America increased 15%. Combined, revenue outside of North America is now 30% of Lululemon's overall revenue and should increase as a percentage of the business over time. The company is expanding with new flagship stores in China and Europe, a strategy that is working wonderfully to convince locals to start wearing the brand.

For the fiscal year ended in January 2021, Lululemon's China revenue was just $298 million. Over the last 12 months, it was approximately $1.7 billion and has grown at a 47% annual rate since January 2021.

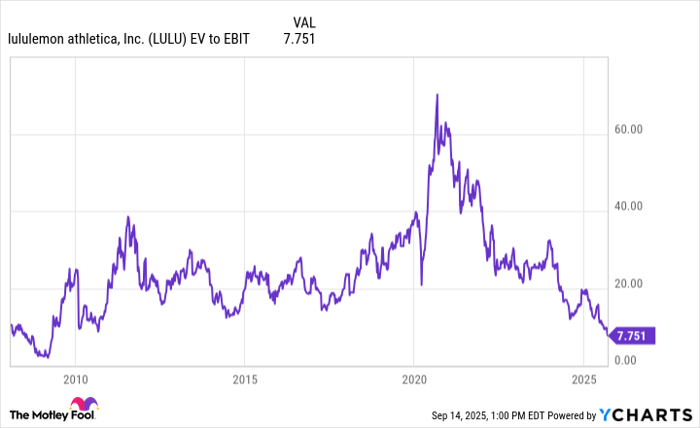

LULU EV to EBIT data by YCharts

Lululemon's revenue is treading water in North America while posting strong growth internationally. But what about its profitability?

The brand is facing headwinds from increasing marketing costs and tariffs on imports into the United States. Gross profit margin slipped to 58.5% last quarter compared to 59.6% in the same quarter a year ago. Operating income decreased 3% year over year in the period, posting a margin of just over 20%.

Guidance calls for $240 million in additional gross profit headwinds this year due to tariffs, which likely hurt Lululemon's stock price. If tariffs remain elevated for the United States, Lululemon will face some margin compression in the years to come. This could hurt its operating income, which has already slightly declined to $2.5 billion over the last 12 months.

Despite these margin worries, Lululemon stock looks historically cheap at current levels, especially if you believe this international revenue growth will continue. At a market cap of $19 billion, Lululemon trades at less than 8x its trailing operating income, which is close to its cheapest earnings ratio ever. Management is pouring money into share repurchases, which will further help growth in earnings per share (EPS) over the long haul.

For those willing to look through the tariff headwinds, Lululemon stock looks extraordinarily cheap today.

Before you buy stock in Lululemon Athletica Inc., consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Lululemon Athletica Inc. wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $648,369!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,089,583!*

Now, it’s worth noting Stock Advisor’s total average return is 1,060% — a market-crushing outperformance compared to 189% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 15, 2025

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Lululemon Athletica Inc. and Nike. The Motley Fool has a disclosure policy.

| 3 hours | |

| 6 hours | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-15 |

Companies Are Replacing CEOs in Record Numbersand Theyre Getting Younger

LULU

The Wall Street Journal

|

| Feb-15 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite