|

|

|

|

|||||

|

|

|

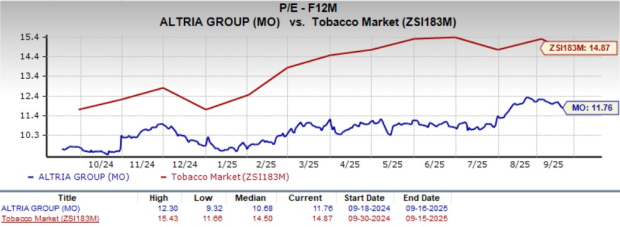

Altria Group, Inc. (MO) is currently trading at a compelling discount relative to both its industry peers and the broader market, positioning it as a potential value opportunity for long-term investors. The stock’s forward 12-month price-to-earnings (P/E) ratio stands at 11.76, well below the Zacks Tobacco industry’s average of 14.87 and significantly lower than the S&P 500’s average of 23.39.

When measured against leading competitors, Philip Morris International Inc. (PM), Turning Point Brands, Inc. (TPB), and British American Tobacco p.l.c. (BTI), Altria’s relative undervaluation becomes even more evident. Philip Morris and Turning Point Brands trade at substantially higher multiples of 20.04X and 28.25X, respectively, while British American Tobacco is more in line with Altria at 11.59X.

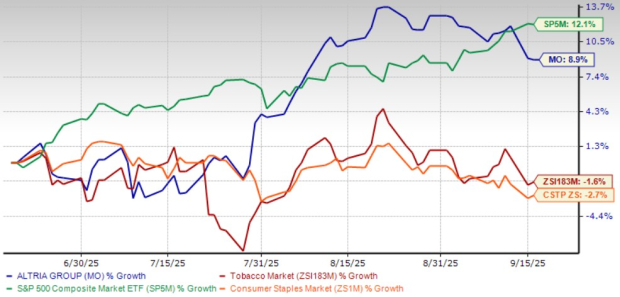

In terms of share performance, Altria has delivered solid gains over the past three months, advancing 8.9%. The tobacco giant outperformed both the industry and the Consumer Staples sector, which slipped 1.6% and 2.7%, respectively, in the same time frame. Meanwhile, the S&P 500 increased 12.1%.

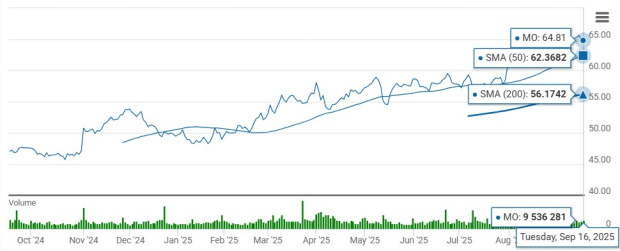

Technical indicators highlight Altria’s strength, with the stock last trading at $64.81, above its 50-day and 200-day moving averages of $62.37 and $56.17, respectively, signaling solid upward momentum and price stability. This suggests positive market sentiment and increasing investor confidence in MO’s outlook.

So far, Altria’s attractive valuation, steady stock performance, and supportive technical indicators underscore its market appeal. To fully grasp what is driving this momentum and assess the company’s long-term potential, it is critical to examine Altria’s underlying fundamentals, where its earnings resilience, portfolio diversification, and strategic growth initiatives become evident.

Altria has reinforced its rally with resilient earnings performance. In the second quarter of 2025, adjusted earnings per share (EPS) rose 8.3% year over year to $1.44, driven by higher pricing, cost efficiencies, and share repurchases. Revenues net of excise taxes were stable at $5.29 billion, highlighting the strength of the company’s diversified portfolio and disciplined execution. Reflecting this momentum, management raised the lower end of its 2025 adjusted EPS guidance to $5.35-$5.45, signaling growth of 3% to 5%.

on! nicotine pouch brand continues to deliver standout results, fueling growth in the company’s oral tobacco segment. Shipments jumped 26.5% in the second quarter to 52.1 million cans, lifting the brand’s retail share to 8.7% of the total oral tobacco market. Supported by effective marketing campaigns and brand activations, on! has gained significant consumer traction. This momentum helped the segment’s adjusted operating income climb 10.9% in the quarter, with margins expanding 310 basis points to 68.7%. The success of on! highlights Altria’s progress in expanding its smoke-free portfolio, a cornerstone of its long-term growth strategy.

Meanwhile, Altria’s smokeable products segment continues to demonstrate resilience, driven by strong pricing and disciplined brand management. Adjusted operating income rose 4.2% in the second quarter, with margins expanding 290 bps to 64.5%. Marlboro maintained its long-standing leadership in the premium category, expanding its share to 59.5% of the segment. This performance highlights the enduring strength of Altria’s flagship brand and its ability to defend profitability even in a challenging industry environment.

Despite strong performance in its smoke-free business, Altria continues to face significant headwinds in its core combustible business. Domestic cigarette shipments fell 10.2% in the second quarter of 2025, reflecting ongoing declines across the broader industry. This contraction is further compounded by rising competition from flavored disposable e-vapor products, highlighting the challenges Altria faces in sustaining volumes in its traditional cigarette portfolio.

Reflecting positive sentiment around Altria, the Zacks Consensus Estimate for EPS has seen upward revisions. Over the past 60 days, the estimate for the current year and next year has increased by 2 cents each to $5.39 and $5.55, respectively. These upward revisions signal improving sentiment among analysts. Based on current projections, MO is expected to deliver year-over-year EPS growth of 5.3% this year and 2.9% next year.

Altria’s combination of attractive valuation, resilient earnings, and supportive technical indicators makes it an appealing choice for long-term, value-oriented investors. Strong growth in the smoke-free portfolio, led by the on! nicotine pouch brand helps offset pressures in the combustible business. Upward EPS revisions over the past 60 days highlight improving analyst sentiment. At present, the stock appears well-positioned for stability, making it more suited for holding rather than aggressive buying. Altria currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-10 | |

| Jul-09 | |

| Jul-03 | |

| Jul-03 | |

| Jul-02 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite