|

|

|

|

|||||

|

|

|

Grocery Outlet Holding Corp. GO showed steady progress in the second quarter of 2025, reflecting a sharper focus on store-level productivity. Net sales increased 4.5% year over year, reaching $1.18 billion, supported by 1.1% comparable store sales (comps) growth and contributions from new store openings. Comps growth was driven by a 1.5% increase in transaction volume, which offset a modest 0.4% decline in average ticket size. The sequential lift from first-quarter growth of 0.3% suggests operational initiatives and store expansion are starting to show early signs of traction.

Management highlighted "green shoots" from targeted initiatives, emphasizing the impact of enhanced in-stock positioning on high-velocity items. The company achieved roughly 150-200 basis points (bps) of comp lift on the fastest-selling 20% of SKUs, demonstrating that focused execution of top-selling products can drive meaningful sales growth. This targeted approach provides a scalable framework to replicate success across the broader store network.

During the quarter, Grocery Outlet opened 11 stores and closed two, bringing its store base to 552 locations. The inclusion of United Grocery Outlet stores also expanded the comp base, further supporting growth comparisons.

At the same time, the company is lifting sales at existing stores through operational tools and execution upgrades. The rollout of the real-time order guide improved in-stock levels of top-selling items, delivering a 200-bps comp lift in test stores. Additionally, a new forecasting tool for meat and produce has driven double-digit sales increases in pilot locations, underscoring how improved inventory visibility directly supports higher sales productivity, store-level execution and customer satisfaction.

Management’s commentary suggests sequential gains in comparable sales through the remainder of the year. We expect comps to improve 2% and 2.6% in the third and fourth quarters, respectively.

Grocery Outlet’s value strategy is driving growth. Management's Known Value Item pricing strategy has been refined to ensure 15-20% basket savings versus discount peers, addressing previous gaps in value perception.

Looking ahead, Grocery Outlet expects these initiatives to drive accelerated comp momentum in the second half of 2025. Management has reaffirmed its guidance for 1-2% comparable store sales growth and raised its full-year adjusted EPS outlook to $0.75-$0.80, reflecting stronger operating discipline and lower interest expense. By balancing measured store expansion, investing in tools that enhance in-store execution and empowering its independent operator network, the company is building a model for long-term productivity and sustainable sales growth.

Ollie's Bargain Outlet Holdings, Inc.’s OLLI second-quarter 2025 results highlighted robust comparable store sales growth, rising 5% year over year. This increase was driven primarily by higher transaction counts across key categories such as food, hardware, lawn & garden, housewares and domestics, reflecting strong customer demand for the company’s value-driven offerings. Management raised full-year comparable store sales guidance to 3-3.5% compared to the prior 1.4-2.2%.

BJ’s Wholesale Club Holdings, Inc. BJ saw a mixed performance in its second quarter, with total comparable club sales declining 0.3% year over year, primarily due to lower fuel retail prices. Excluding gasoline, comparable sales rose a solid 2.3%, driven by strong customer traffic. Digital initiatives continued to drive momentum, with digitally enabled comparable sales surging 34%, contributing to a two-year stacked growth of 56%. Looking ahead, BJ expects fiscal 2025 comparable club sales, excluding gasoline, to increase between 2% and 3.5% year over year, reflecting ongoing investments in membership growth, higher-tier penetration, and enhanced digital capabilities.

Albertsons Companies, Inc. ACI reported strong comparable sales momentum in the first quarter of fiscal 2025, driven by robust growth across pharmacy, digital platforms and loyalty programs. The company’s focus on enhancing the customer value proposition, modernizing operations through technology and productivity initiatives, and investing in store upgrades and private brands contributed to the improved performance. Reflecting this positive trajectory, Albertsons has raised its fiscal 2025 comparable sales guidance to a range of 2.0-2.75%, up from the prior forecast of 1.5-2.5%, signaling confidence in sustained customer engagement and long-term operational improvements.

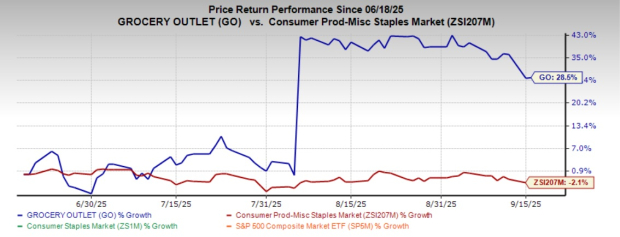

GO stock has gained 28.5% in the past three months against the industry’s 2.1% decline.

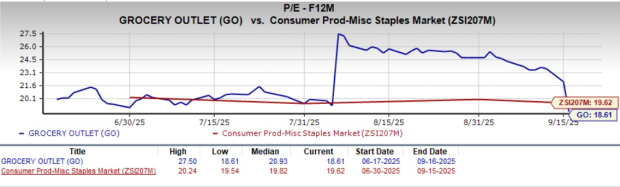

Grocery Outlet’s forward 12-month price-to-earnings ratio of 18.61X indicates a lower valuation compared with the industry’s average of 19.62X.

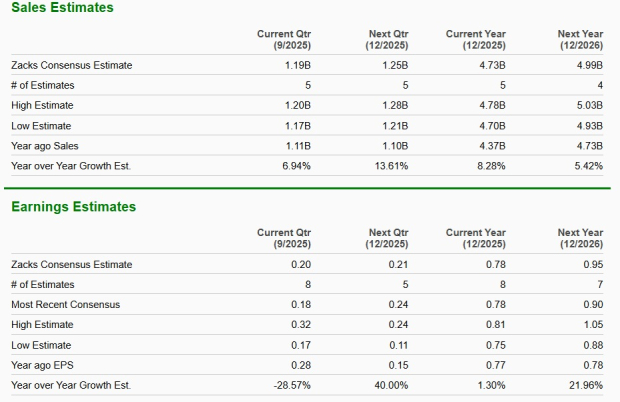

The Zacks Consensus Estimate for Grocery Outlet’s current fiscal-year sales and earnings per share implies year-over-year growth of 8.3% and 1.3%, respectively.

Grocery Outlet carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 13 hours | |

| Apr-23 | |

| Apr-23 | |

| Apr-20 | |

| Apr-17 | |

| Apr-16 | |

| Apr-16 | |

| Apr-15 | |

| Apr-15 | |

| Apr-15 | |

| Apr-15 | |

| Apr-14 | |

| Apr-14 | |

| Apr-14 | |

| Apr-14 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite