|

|

|

|

|||||

|

|

|

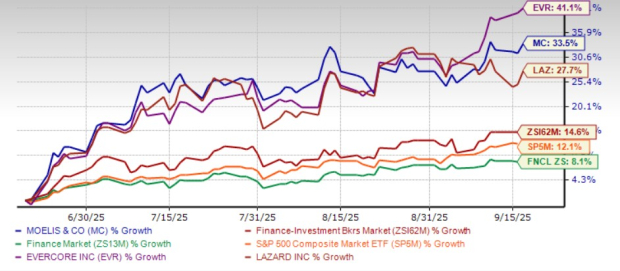

In the past three months, Moelis & Co. MC shares have demonstrated strong performance. The stock has soared 33.5%, outperforming the industry, the Finance sector and the S&P 500 index. Further, it has fared better than its peer, Lazard Inc. LAZ, while underperforming Evercore, Inc. EVR in the same time frame.

MC’s Three-Month Price Performance

This underscores positive market sentiments and confidence in Moelis & Co.’s financial health and prospects. Let’s find out whether MC’s current rally has legs or it's time to sell.

Federal Reserve Interest Rate Cut to Aid M&A: On Sept. 17, 2025, the Federal Reserve lowered rates by 25 bps for the first time this year, citing persistent inflation and a weakening labor market under the Trump administration’s tariff regime. The Fed also signaled two additional cuts before year-end.

Lower borrowing costs and supportive equity valuations should drive stronger mergers and acquisitions (M&A) volumes, enhancing Moelis & Co’s advisory revenues. While looser credit conditions may temporarily dampen restructuring activity, Moelis’s diversified advisory platform positions it to capture upside from increased domestic transactions and sector-specific consolidation.

Solid Organic Performance: Moelis & Co. has been demonstrating robust organic performance. Despite revenue declines in 2019, 2022, and 2023 due to cyclical softness in M&A completions, the company achieved a robust 10% compound annual growth rate (CAGR) over the five years ending in 2024. That momentum carried into the first half of 2025, supported by higher average fees per deal and an ongoing surge in global restructuring activity as highly leveraged companies adapt to a changing rate environment.

This, along with efforts to boost geographical expansion and capital markets business, will likely support the company’s revenues in the quarters ahead.

Business Diversification: MC has significantly diversified its business operations across a broad range of sectors and regions. Further, the company doesn’t have substantial client concentration, with the top 10 transactions representing less than 25% of total revenues.

Additionally, its collaborations in Japan and Mexico, as well as its non-controlling stake in Moelis Australia Limited, offer significant support. With more than $5.1 trillion in advised transactions since inception, global expansion and diversification are expected to continue supporting its profitability.

Encouraging Capital Distributions: Moelis & Co. has been engaged in meaningful capital distributions. Since 2014, the firm has announced 11 dividend increases, with the most recent one announced in February 2025.

In 2021, the company announced an increase in its share repurchase authorization by $100 million. As of June 30, 2025, it had roughly $61.1 million in authorization remaining.

Given a debt-free balance sheet, the company’s capital distributions seem sustainable going forward.

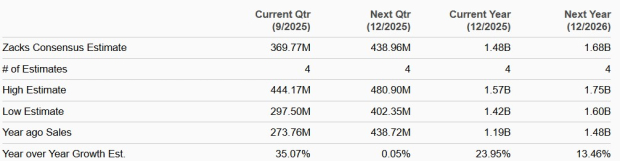

The Zacks Consensus Estimate for Moelis & Co.’s 2025 and 2026 revenues suggests a year-over-year increase of 24% and 13.5%, respectively.

Sales Estimates

Also, the consensus estimate for MC’s earnings suggests a 37.9% and 28.7% jump in 2025 and 2026, respectively. Earnings estimates for both years have been revised upward over the past 30 days.

Estimate Revision

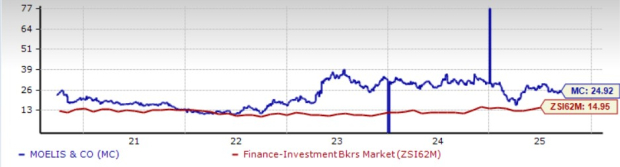

MC stock is currently trading at a 12-month forward price-to-earnings (P/E) of 24.92X. This is above the industry’s 14.95X and shows that the stock is expensive at present.

12-month Forward Price-to-Earnings Ratio (P/E F12M)

MC stock is expensive compared with Evercore and Lazard. At present, Evercore has a P/EF12M of 17.74X and Lazard’s P/EF12M is 15.96X.

Moelis & Co.'s robust organic growth, business restructuring initiatives and diversification efforts will drive growth. Moreover, bullish analyst sentiments are another positive.

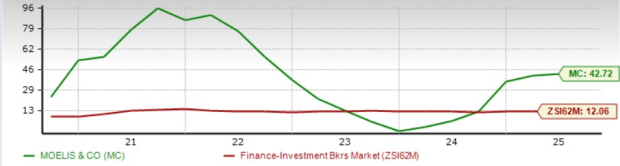

Additionally, Moelis & Co.’s growth initiatives have helped generate higher returns. This is demonstrated by the company’s return on equity (ROE) of 42.72% compared with the industry’s ROE of 12.06%.

Return on Equity

On the other hand, Evercore has an ROE of 27.29% and Lazard has an ROE of 34.33%, reflecting that MC is efficient in capital allocation activities compared with its peers.

However, a steady rise in expenses is a headwind. The company recorded a five-year CAGR of 10.1% (ended 2024), mainly due to higher compensation costs. The uptrend continued in the first six months of 2025. As the company expands its operations into new sectors and products, overall costs are expected to remain elevated.

Further, given rising geopolitical risks, foreign currency fluctuations and the global impact of tariff policies, MC may witness subdued overseas revenues (22.6% of total revenues in the first half of 2025), which will likely weigh on its growth to some extent.

Nonetheless, relatively lower rates on the back of interest rate cuts are likely to bolster M&A activities. Also, a solid balance sheet will likely continue to aid enhanced capital distributions. While valuation remains stretched, higher growth prospects justifies it. Thus, MC remains an attractive investment pick for investors.

Currently, MC sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-11 | |

| Jul-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite