|

|

|

|

|||||

|

|

|

There’s a reason Vici Properties is performing better than it seemingly should be at this time.

Coca-Cola shares have struggled thanks to worries over tariffs, but these fears aren’t merited to the degree they’re being priced in.

Electricity is on the verge of soaring, and one company stands more ready than most to meet the need.

Usually, when you've got some idle cash you're looking to invest, you'd choose to further diversify your portfolio with a completely new holding. Sometimes, though, it makes sense to buy more of a name you already own. This can be particularly true of dividend stocks, where sector diversification means a little less. Dividend sustainability is the top criterion on this front... that, and the dividend yield at the time of your purchase. Bigger is better, of course.

Here are three great dividend stocks to consider buying right now, even if you already own a stake in them. Their recent (but temporary) weakness will allow you to step in at an above-average yield.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Vici Properties (NYSE: VICI) is anything but a household name. In fact, there's a good chance you've never even heard of it. There's also a good chance that you've been on one of its properties without even realizing it.

Vici is a real estate investment trust, or REIT. REITs own portfolios of rental or revenue-bearing properties like apartment complexes, office buildings, or hotels, and pass along the majority of their profits to shareholders in the form of dividends. Vici's focus is entertainment. Its properties include 54 casinos, four golf courses, over 50 entertainment venues, and more than 1,000 retail stores and restaurants. MGM and Caesars are its top tenants, although it's not a stretch to suggest that all its tenants are able to stand up to economic headwinds and continue paying their rent.

It seems like a risky specialization. Discretionary spending can and does ebb and flow in step with the economy, after all. There is some risk here, to be sure.

Vici sidesteps a portion of the risk related to being in this business, since its leases are so-called "triple net" leases. That means the tenants are responsible for costs like property taxes, maintenance, and insurance. Vici only needs to worry about making the fixed payment on the loans it takes out to purchase its properties.

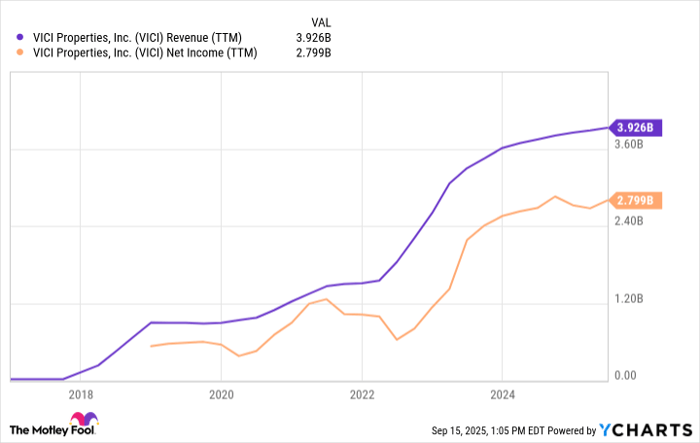

It's proven itself to be very good at what it does. As of the second quarter of this year, its occupancy rate stood at 100%, with $46 billion worth of assets turning into $1 billion worth of net rent-based revenue, and $865 million worth of net income. All three of these numbers extend well-established (if sometimes erratic) growth trends.

VICI Revenue (TTM) data by YCharts.

More importantly for income-minded investors, this cash flow supports a quarterly dividend payment that's been raised every year since Vici Properties went public in 2017. You'd be stepping in while the forward-looking yield stands at a healthy 5.4%.

You'll never experience jaw-dropping growth with this stock. But you will reliably collect a good amount of income that's been growing faster than inflation.

To say Coca-Cola (NYSE: KO) is an oldie-but-goodie dividend pick would understate the matter. It's been a top dividend stock recommendation for so long that it's almost become a cliché.

Yet, clichés usually exist for good reason. In this case, it's because the soft drinks giant boasts one of the stock market's most impressive dividend pedigrees. Not only has Coca-Cola paid a quarterly dividend like clockwork for decades, it's upped its per-share dividend payment every year for the past 63 years. Only eight other publicly traded companies have a longer track record of uninterrupted growth.

That's the result of the nature of the business paired with its sheer scale and savvy marketing of its brand names like Minute Maid, Gold Peak, and its namesake cola, just to name a few. You'll find the words "Coca-Cola" and the company's red and white logo on everything from Christmas ornaments to home décor to clothing, and more. It's not just a beverage company. It's become part of the culture, and for many people, it's part of a lifestyle.

Image source: Getty Images.

So why is the stock down nearly 10% from its April peak and still pressing deeper into a new multi-month low? Tariff fears, mostly. While it's not directly affected by higher import and export fees (Coca-Cola's products are typically bottled near where they're consumed), the market is worried that higher prices and resulting economic weakness worldwide could take a toll on consumers' capacity to pay for premium brands like Coca-Cola.

Investors weren't exactly thrilled with the organization's new full-year guidance numbers released in July, either. They weren't really any different than April's numbers. It's just that the market was hoping for some bullish revisions.

This is one of those cases, however, where the crowd has lost sight of the bigger picture. This year's expected revenue growth rate of between 5% and 6% is actually quite solid, as is the likely growth of 2% to 3% for its per-share profits.

There is one upside to the pullback. It's pumped Coca-Cola's forward-looking dividend yield up to just above 3%. It's been a while since anyone could plug into this stock at that rate.

Finally, add NextEra Energy (NYSE: NEE) to your list of dividend stocks to double up on right now, in the wake of weakness since 2021 that's inflated its forward-looking yield to 3.2%. Except for being the biggest name in the business as measured by market capitalization, NextEra Energy looks like just another utility outfit.

In many ways, it is. In addition to providing electricity to 12 million Floridians through its wholly owned utility outfit FPL, the company is also a wholesaler, selling power generated by its 72-gigawatt portfolio to other utility companies that need it to serve their own customers.

If you dig deeper, though, you'll find some more nuanced and qualitative differences between this organization and its peers. Namely, this one's handling the inevitable transition from fossil fuels to renewables better than most. More than half of the electricity it generates now comes from renewables like wind and solar, while another 36% is produced with natural gas.

Yet another 8% of its power comes from nuclear power plants, which have become en vogue again now that they're safer than in the past, and now that artificial intelligence data centers have created the immediate need. NextEra Energy is also expanding its energy-storage capacity, equipping it to meet the marketplace's needs more cost-effectively.

Although the company is over a century old, it looks like a utility outfit you'd build from scratch today to meet modern-day demand for electricity. It also doesn't appear to be bogged down by any legacy operations that other utility service providers are being all but forced to phase out now.

That's not quite the reason income investors should consider taking on a stake in this company. NextEra Energy stock is a buy here largely because the need for electricity is on the verge of exploding. Artificial intelligence technology implementation consultant ICF predicts demand for electricity in the United States alone is set to grow by 25% between now and 2030, and will be nearly 80% greater by 2050. With a backlog of nearly 30 gigawatts' worth of production capacity just waiting to be completed within the next couple of years, few (if any) other names in the business are as prepared for this growth as NextEra is.

Before you buy stock in Coca-Cola, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Coca-Cola wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $662,520!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,043,346!*

Now, it’s worth noting Stock Advisor’s total average return is 1,056% — a market-crushing outperformance compared to 188% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 15, 2025

James Brumley has positions in Coca-Cola. The Motley Fool has positions in and recommends NextEra Energy. The Motley Fool recommends Vici Properties. The Motley Fool has a disclosure policy.

| Mar-13 | |

| Mar-12 | |

| Mar-12 | |

| Mar-11 | |

| Mar-11 | |

| Mar-11 | |

| Mar-11 | |

| Mar-11 | |

| Mar-11 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite