|

|

|

|

|||||

|

|

|

UiPath PATH stands out in the competitive automation landscape for one simple reason: financial autonomy. At the close of the second quarter of fiscal 2026, the company held $1.4 billion in cash and equivalents and carried zero debt obligations.

That clean balance sheet is more than a statistic; it’s a strategic advantage. In an environment where many technology peers juggle refinancing pressures or interest expenses, UiPath can channel dollars toward growth, innovation and strategic initiatives.

A critical measure underscoring this strength is its current ratio of 2.75, significantly higher than the industry benchmark of 1.95. This liquidity buffer ensures UiPath can cover near-term obligations while retaining ample capacity to seize opportunities in a fast-moving automation software market. Whether it’s scaling AI-driven capabilities, expanding into new geographies, or acquiring niche automation providers, UiPath has the financial firepower to act decisively.

This debt-free profile becomes even more compelling against the backdrop of a volatile macroeconomic climate. Enterprise IT spending often slows during uncertainty, but UiPath’s liquidity provides a cushion to weather downturns without sacrificing long-term strategic priorities. Unlike rivals who must balance innovation with repayment schedules, UiPath enjoys the luxury of deploying its capital aggressively.

For investors, this balance sheet strength translates into durability and optionality. It minimizes downside risk while amplifying upside potential, particularly as global demand for automation accelerates. Put simply, UiPath’s financial foundation doesn’t just support growth; it enables bold bets on the future of enterprise automation.

Microsoft MSFT and ServiceNow NOW remain formidable rivals, but their financial strategies differ from UiPath’s. Microsoft, while a giant with unparalleled scale, must spread capital across diverse segments such as cloud, gaming and productivity software, somewhat diluting its focus on automation. ServiceNow continues to gain traction in enterprise workflow automation but remains heavily invested in sustaining growth momentum, balancing expansion with cost pressures.

Compared to these players, UiPath’s debt-free balance sheet allows it to dedicate resources squarely to automation. Microsoft has the advantage of size, and ServiceNow has enterprise reach, but UiPath’s singular financial flexibility gives it agility neither can fully replicate.

The stock has surged 12% over the past six months, underperforming the industry’s 28.5% rally.

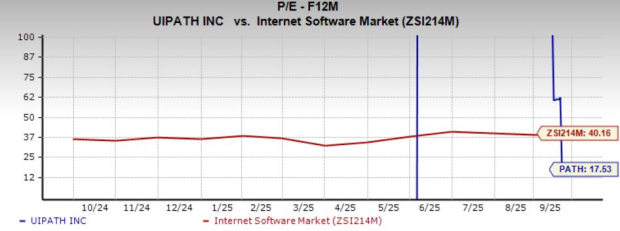

From a valuation standpoint, PATH trades at a forward price-to-earnings ratio of 17.53X, which is well below the industry’s average of 40.16X. It carries a Value Score of F.

The Zacks Consensus Estimate for PATH’s earnings has been on the rise over the past 30 days.

PATH stock currently carries a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 33 min | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours |

Microsoft Stock Slopes Down To Lowest Point in Months; Is The Stock A Buy Now?

MSFT

Investor's Business Daily

|

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite