|

|

|

|

|||||

|

|

|

We count the recent quarterly results from the likes of homebuilder Lennar and restaurant operator Darden Restaurants and five other S&P 500 members for their respective fiscal quarters ending in August as part of our September-quarter tally.

We have another seven S&P 500 members on deck to report such results this week, including Costco COST, Accenture ACN, and others. By the time the big banks come out with their quarterly reports on October 14th, we will have seen early Q3 results from almost two dozen S&P 500 members.

We will discuss current expectations for Costco and Accenture later in this note, but we will first review the aggregate Q3 expectations for the S&P 500 index as a whole.

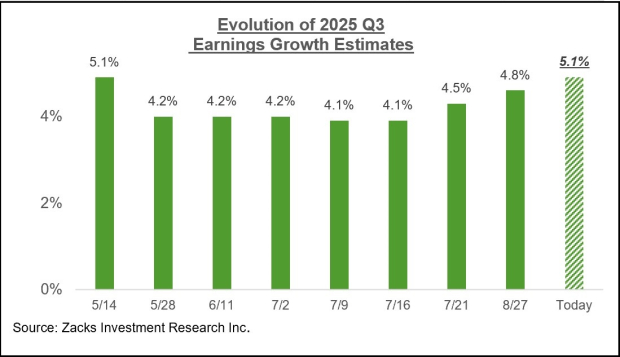

The expectation is for Q3 earnings to increase by +5.1% from the same period last year on +6% higher revenues. This would follow earnings growth rates of +12.5% and +12.3% in 2025 Q2 and Q1, respectively.

In the unlikely event that actual Q3 earnings growth for the S&P 500 index turns out to be +5.1%, as currently expected, this will be the lowest earnings growth pace for the index since the +4.4% growth rate in Q3 2023.

We have been regularly flagging in recent weeks that the estimate revisions trend has been positive since late April, after remaining under pressure in the months leading up to that point. You can see this in the chart below that plots how 2025 Q3 earnings growth expectations evolved in recent weeks.

Since the start of July, Q3 earnings estimates have increased for 5 of the 16 Zacks sectors, which include the Tech, Finance, and Energy sectors.

While Q3 estimates for the remaining 11 sectors have been under pressure, the favorable revisions trend for the Tech and Finance sectors is more than enough to offset their effect on the aggregate trends at the index level, as these two sectors alone account for more than 50% of the index’s total earnings.

On the negative side, estimates for 11 of the 16 Zacks sectors have been under pressure since the start of the quarter, with notable declines in the Medical, Transportation, Basic Materials, and Consumer Staples sectors, among others.

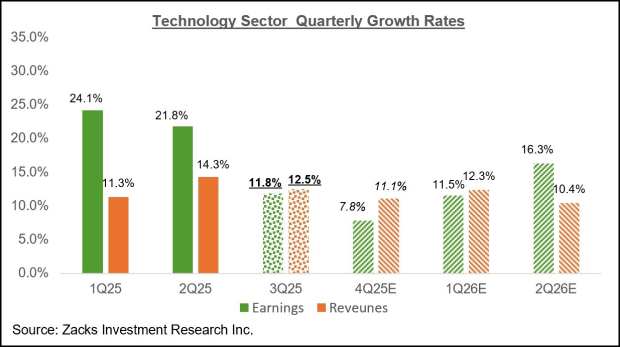

The Tech sector, which has been a standout growth driver in recent quarters, is expected to continue playing that role in 2025 Q3 as well, with total earnings for the sector expected to be up +11.8% on +12.5% higher revenues. Had it not been for the strong growth contribution from the Tech sector, total S&P 500 earnings growth for Q3 would be only +2% (instead of +5.1% otherwise).

The chart below illustrates the Tech sector’s earnings and revenue growth picture on a quarterly basis, comparing expectations for 2025 Q3 with actual growth for the preceding two periods and expectations for the following three quarters.

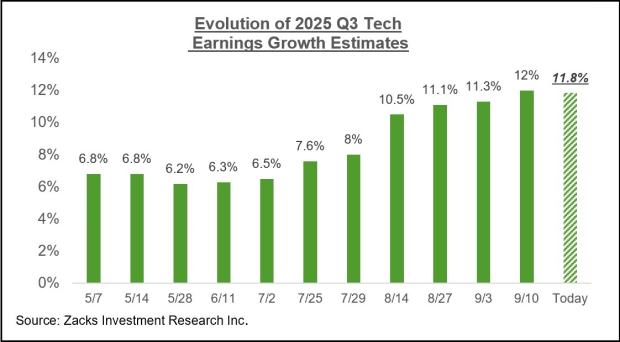

As noted earlier, Q3 estimates for the Tech sector have been trending higher since the quarter began, although they have decreased slightly in recent days, as the chart below shows.

Key Earnings Reports This week

We have more than 30 companies scheduled to report results this week, including seven S&P 500 members. In addition to Accenture and Costco, notable companies reporting this week include Micron Technologies, AutoZone, CarMax, and others.

Sentiment has been downbeat on Accenture shares lately, with the stock losing -32.2% of its value in the year-to-date period, lagging its peers as well as the broader market by big margins. Driving the negative sentiment about Accenture is a combination of flat IT spending trends outside of AI-focused spending and the disintermediation threat to the company’s business resulting from AI.

Accenture is expected to earn $2.98 per share on $17.3 billion in revenues, representing year-over-year changes of +6.8% and +5.6%, respectively. Estimates have been stable lately, but have modestly nudged down since the start of the period.

Costco shares have lost ground lately, with the stock up +4.4% this year, lagging Walmart’s +13.6% gain and the S&P 500 index’s +13.8% gain. The stock’s underperformance relative to Walmart started around July and has persisted since then. One likely explanation is the competitive challenge posed by Amazon’s announcement of same-day delivery for grocery items, but we will see if the quarterly release, scheduled after the market’s close on Thursday, September 25th, serves as a catalyst.

The expectation is that Costco will come out with $5.81 per share in earnings on $86.14 billion in revenues, representing year-over-year changes of +12.8% and +8.1%, respectively. The revisions trend has been moderately negative lately, with estimates for next year (fiscal year ends in August) down over the last two months.

The Earnings Big Picture

The chart below displays current Q3 earnings and revenue growth expectations for the S&P 500 index in the context of the preceding four quarters and the next three quarters.

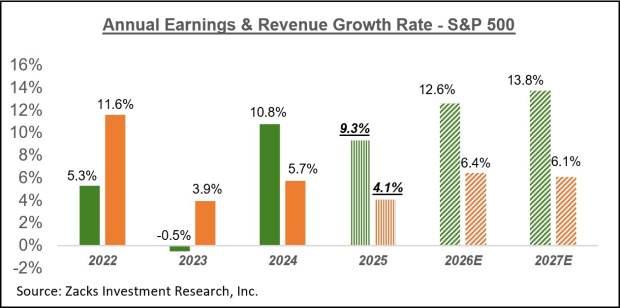

The chart below shows the overall earnings picture on a calendar-year basis.

In terms of S&P 500 index ‘EPS’, these growth rates approximate to $257.80 for 2025 and $290.29 for 2026.

For a detailed view of the evolving earnings picture, please check out our weekly Earnings Trends report here >>>>Q3 Earnings Outlook Remains Positive: A Closer Look

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-26 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite