|

|

|

|

|||||

|

|

|

Bill Gurley is best known for making an early bet on Uber.

Gurley recognized that Uber had potential that stretched beyond the core ridehailing business.

Given some recent comments, it would appear that Gurley sees Tesla following a similar trajectory, given its ambitions beyond electric vehicles and energy storage services.

Bill Gurley is a renowned venture capital investor, best known for his early bets on companies that have since become household names -- including Zillow, OpenTable, and Nextdoor. His most celebrated investment, however, was his early backing of Uber Technologies when the company was still vying for credibility of its ride-hailing business model.

Looking back, Uber's success may have seemed inevitable. But at the time, many skeptics dismissed the company as little more than a digital taxi service. Gurley, by contrast, recognized its greater potential: The optionality to evolve into a platform beyond ride-hailing and branch into adjacent services, ultimately reaching broader consumer demographics worldwide.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

It is this ability to identify transformational opportunities from afar that makes Gurley's recent remarks about Tesla (NASDAQ: TSLA) so noteworthy.

In the discussion below, I'll explore what the Silicon Valley veteran sees in Tesla today, and why it echoes the vision he applied to Uber many years ago.

A few days ago, Gurley joined a discussion on X (formerly Twitter) to push back against the claim that Tesla's valuation is a bubble waiting to burst.

If you study equity valuation theory, most models (such as a DCF) include the idea of "optionality". This represent the probability or odds that a company might be successful in new endeavors. No one ranks higher on that dimension than @elonmusk. Not even close.

-- Bill Gurley (@bgurley) Sept. 13, 2025

Gurley began his explanation by pointing to one of the most widely used valuation tools in finance: the discounted cash flow (DCF) model. In simple terms, a DCF model projects a company's future cash flows and discounts them back to their present value using the weighted average cost of capital (WACC). This calculation provides an estimate for a company's intrinsic value today.

Applying this framework to Tesla, however, is anything but straightforward. The company's current revenue and profits are driven by sales of electric vehicles and energy storage services. Long-time Tesla supporters understand that this is only part of the equation, though.

As Gurley notes, what makes Tesla's valuation so elusive is the company's "optionality" embedded in its broader ambitions. Beyond its legacy operations, Tesla is pursuing transformative bets in artificial intelligence (AI) -- particularly an autonomous ride-hailing fleet, known as the robotaxi, and its humanoid robotics platform, Optimus.

Image source: Getty Images.

By highlighting Tesla's optionality, Gurley is drawing a parallel to the kind of platform potential that underpinned his success with Uber. The comparison is striking, given that Tesla and Uber can currently be viewed as fierce rivals in the mobility market.

Gurley's acknowledgement of Tesla's ambitions beyond EVs and energy storage signals that he sees its so-called moonshot bets as too significant to dismiss. In effect, he may be suggesting that Tesla's innovation pipeline extends well beyond the confines of traditional competition -- underscoring the idea that overlooking these opportunities could prove to be a costly mistake in the long run.

For investors, Gurley's observation carries important implications. He reframes the narrative around Tesla as one beyond an automobile manufacturer but rather a more diversified platform spanning multiple ventures.

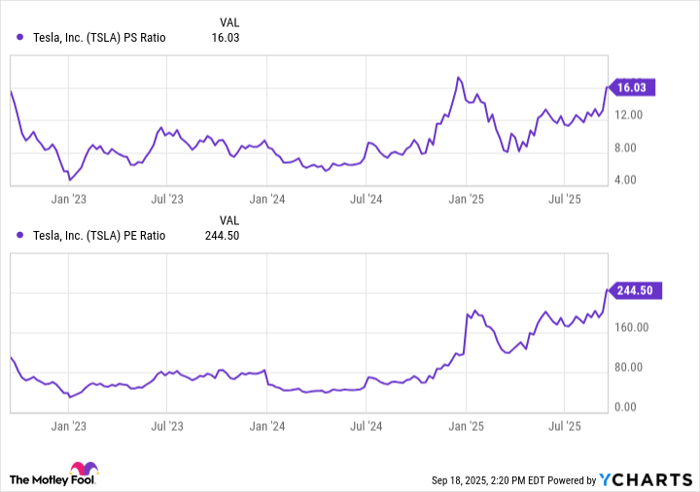

As the chart below illustrates, Tesla's expanding price-to-sales (P/S) and price-to-earnings (P/E) multiples suggest that the market is struggling to assign appropriate values to its emerging businesses, given that the company has yet to meaningfully commercialize them.

TSLA PS Ratio data by YCharts

In other words, a portion of the anticipated upside from initiatives like robotaxi and Optimus already appears priced in to Tesla's valuation despite their limited traction today. With that in mind, some investors may choose not to follow the clear momentum pictured above.

At the same time, Gurley implies that Tesla indeed should be valued less in line with capital-intensive car or energy companies and more as a technology-driven growth enterprise. Ultimately, Gurley's comments underscore the hidden multiplier potential that Tesla's optionality provides in its valuation. Should Musk and the team execute successfully, Gurley's insights may prove prophetic -- and what looks like a frothy valuation today could ultimately appear conservative in hindsight.

In my view, investing in Tesla stock today boils down to your personal alignment with the very narrative that Gurley points out.

If you are more risk-averse, then it's likely better to wait and see how Tesla scales its AI businesses and assess how these next-generation products move the needle for the business.

By contrast, if you are a growth investor and plan to hold onto a core position in Tesla over the course of several years, now may be an interesting time to scoop up some shares, as more upside could very well be in store, as Gurley alludes.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of September 22, 2025

Adam Spatacco has positions in Tesla. The Motley Fool has positions in and recommends Tesla, Uber Technologies, and Zillow Group. The Motley Fool has a disclosure policy.

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

Elon Musk: Tesla FSD Coming To Europe, Alongside Cybercab, Optimus Production

TSLA

Investor's Business Daily

|

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite