|

|

|

|

|||||

|

|

|

Pfizer PFE announced a definitive agreement to acquire obesity drug developer, Metsera MTSR, to re-enter the lucrative obesity space after it scrapped the development of danuglipron, a weight-loss pill, earlier this year.

Pfizer will acquire Metsera’s shares for $47.50 per share in cash or a total enterprise value of $4.9 billion. The deal also includes a non-transferable contingent value right (CVR) of up to $22.50 per share, contingent upon the achievement of certain clinical and regulatory milestones.

The purchase price of $47.50 represents a premium of around 43% on Metsera’s closing price on Friday. MTSR stock shot up 61% on Monday.

Metsera, a New York-based biotech, which went public earlier this year, is developing innovative therapies to treat obesity and cardiometabolic diseases. The acquisition will add Metsera’s four novel clinical-stage incretin and amylin programs to Pfizer’s pipeline. Metsera’s lead pipeline candidate is MET-097i, a weekly and monthly injectable GLP-1 receptor agonist (RA). Both doses are in phase II studies. It is also developing an ultra-long-acting amylin analog, MET-233i, in phase I. Two oral GLP-1 RA candidates are expected to enter clinical development soon.

The boards of both companies unanimously approved the transaction, which is expected to be closed in the fourth quarter of 2025, subject to shareholder approvals.

The proposed acquisition of Metsera comes after Pfizer failed to develop its own obesity candidate. In April, Pfizer discontinued the development of its GLP-1R agonist, danuglipron, which was being developed as a weight loss pill. Pfizer took the decision after one of the participants in the dose-optimization studies developed a potentially drug-induced liver injury, which resolved after danuglipron was discontinued. The deal with Metsera brings back Pfizer on the obesity map.

The obesity market has gained tremendous popularity, with Goldman Sachs projecting it to grow to $100 billion by 2030. Eli Lilly LLY and Novo Nordisk NVO currently dominate the space with their respective GLP-1 injections, Zepbound and Wegovy. In order to maintain their dominance in the market, both Lilly and Novo Nordisk are investing broadly in obesity and have several next-generation obesity drugs (both oral and injectable medications) currently in clinical development or under regulatory review.

Several other companies, like Amgen and Viking Therapeutics, are also developing more potent and convenient GLP-1-based candidates in late-stage studies.

Metsera’s products are relatively in early stages of development, and if approved, will be launched in the 2028-2029 period. This means Pfizer is at least 2-3 years away from having an obesity drug in the market. This implies it may lag far behind the likes of Lilly, Novo Nordisk and probably even Amgen and Viking in this highly competitive space. However, the obesity market has tremendous potential and may offer opportunities for all. Albert Bourla, chief executive officer of Pfizer, said that obesity is a “large and growing space with over 200 health conditions associated with it,” which creates significant unmet need. Only time will tell if Pfizer’s acquisition of Metsera will pay off.

Like Pfizer, some other large drugmakers, like AbbVie, Roche and Merck, have bought rights to obesity candidates through licensing deals with smaller biotechs in a bid to enter the obesity space.

In March, AbbVie in-licensed rights to develop phase I candidate, GUB014295 (now called ABBV-295), a long-acting amylin analog for the treatment of obesity, from Danish research company, Gubra. AbbVie plans to invest further in obesity.

To foray into the lucrative obesity market, last year, Merck in-licensed rights global rights to an investigational oral GLP-1 receptor agonist, HS-10535, from Chinese biotech Hansoh Pharma.

Roche acquired privately owned biotech, Carmot Therapeutics, in 2024, which added its lead incretin asset CT-388. Roche also recently entered into an exclusive collaboration and licensing agreement with Zealand Pharma to develop and commercialize petrelintide, Zealand Pharma’s amylin analog, as a standalone therapy and in a fixed-dose combination with CT-388.

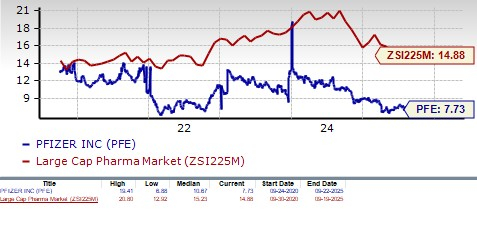

Pfizer’s stock has declined 9.4% so far this year against an increase of 0.9% for the industry.

From a valuation standpoint, Pfizer appears attractive relative to the industry and is trading below its 5-year mean. Going by the price/earnings ratio, the company’s shares currently trade at 7.73 forward earnings, lower than 14.88 for the industry and the stock’s 5-year mean of 10.67.

The Zacks Consensus Estimate for 2025 earnings has risen from $3.05 per share to $3.14 per share, while that for 2026 has risen from $3.08 per share to $3.10 per share over the past 60 days.

Pfizer has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| May-16 | |

| May-14 | |

| May-14 | |

| May-14 | |

| May-14 | |

| May-13 | |

| May-13 |

Novo Nordisks high-dose Wegovy touts near 28% weight loss in early responders

NVO

Clinical Trials Arena

|

| May-13 | |

| May-13 | |

| May-13 | |

| May-12 | |

| May-12 | |

| May-12 |

Meet The New IPO Trying To Take On Eli Lilly And Novo Nordisk In Obesity

LLY

Investor's Business Daily

|

| May-12 | |

| May-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite