|

|

|

|

|||||

|

|

|

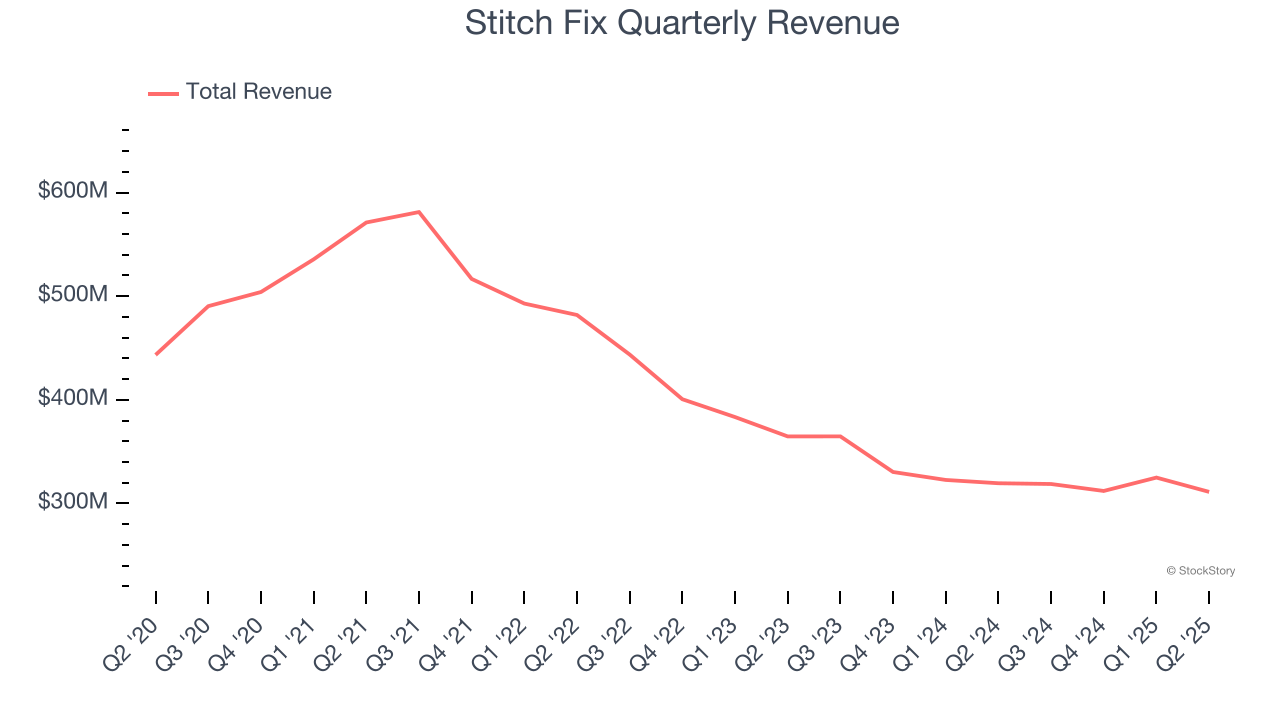

Personalized clothing company Stitch Fix (NASDAQ:SFIX) beat Wall Street’s revenue expectations in Q2 CY2025, but sales fell by 2.6% year on year to $311.2 million. On top of that, next quarter’s revenue guidance ($335.5 million at the midpoint) was surprisingly good and 13.1% above what analysts were expecting. Its GAAP loss of $0.07 per share was 29% above analysts’ consensus estimates.

Is now the time to buy Stitch Fix? Find out by accessing our full research report, it’s free.

“Fiscal 2025 was a milestone year for Stitch Fix. We finished the year with our second consecutive quarter of year-over-year revenue growth on an adjusted basis, and once again gained share in the US apparel market,” said Matt Baer, CEO, Stitch Fix.

One of the original subscription box companies, Stitch Fix (NASDAQ:SFIX) is an online personal styling and fashion service that curates personalized clothing selections for customers.

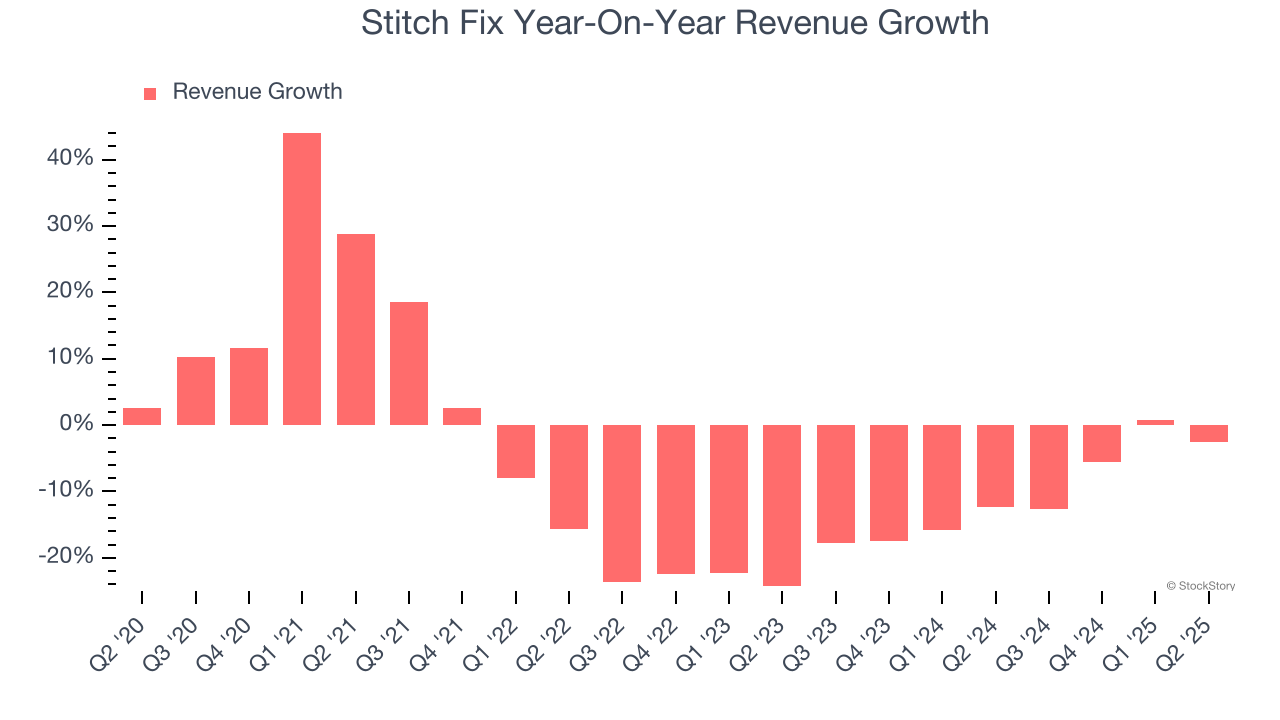

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Stitch Fix’s demand was weak over the last five years as its sales fell at a 5.8% annual rate. This wasn’t a great result and is a sign of poor business quality.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Stitch Fix’s recent performance shows its demand remained suppressed as its revenue has declined by 10.8% annually over the last two years.

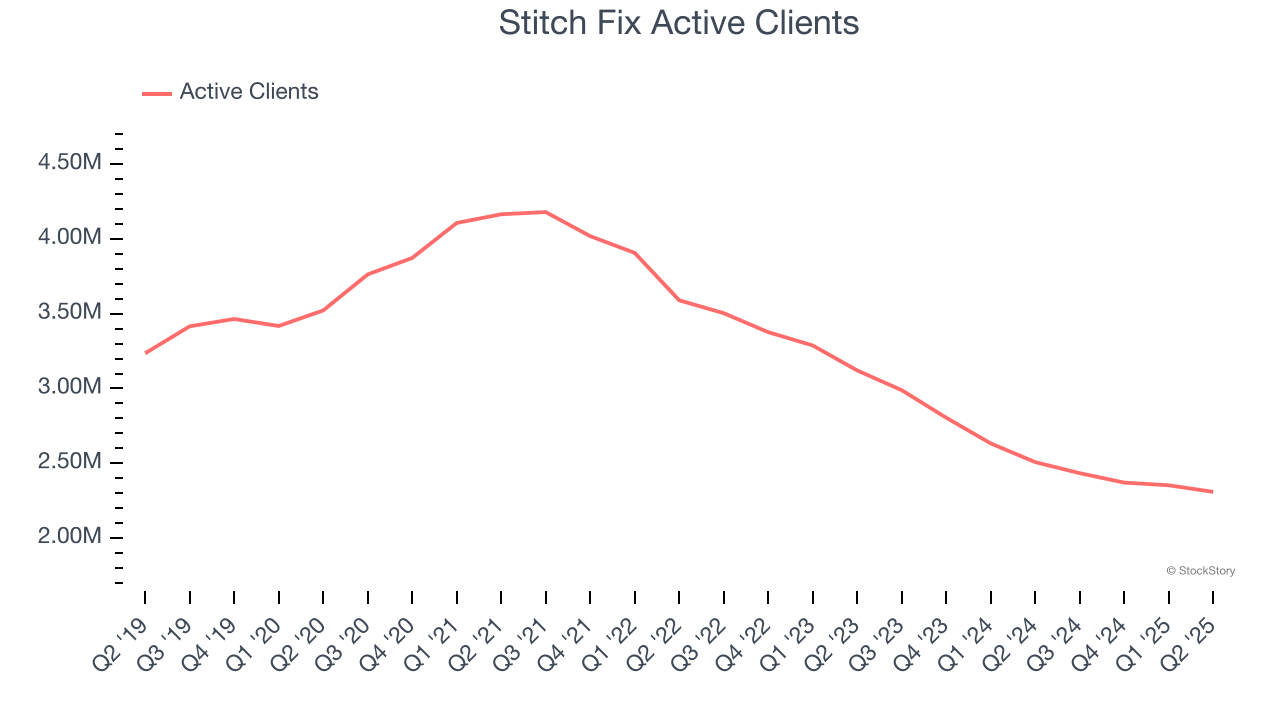

We can dig further into the company’s revenue dynamics by analyzing its number of active clients, which reached 2.31 million in the latest quarter. Over the last two years, Stitch Fix’s active clients averaged 15.5% year-on-year declines. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Stitch Fix’s revenue fell by 2.6% year on year to $311.2 million but beat Wall Street’s estimates by 2.4%. Company management is currently guiding for a 5.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 2% over the next 12 months. Although this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

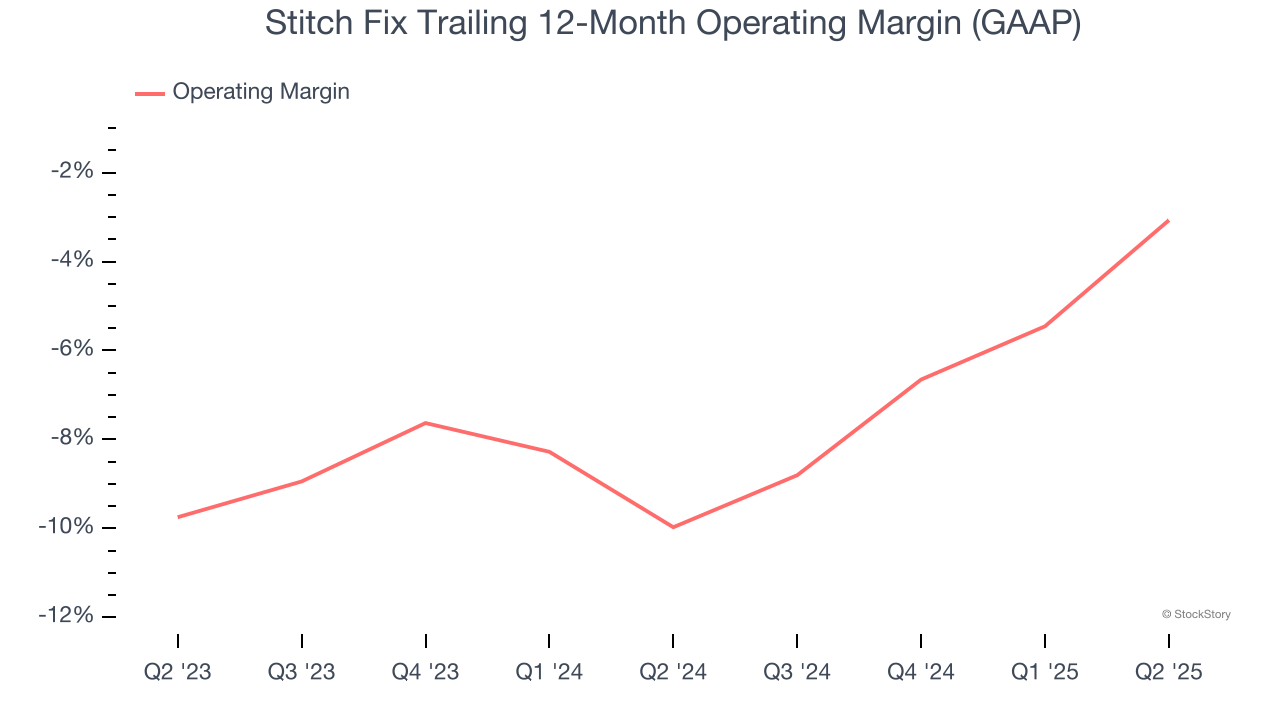

Stitch Fix’s operating margin has risen over the last 12 months, but it still averaged negative 6.6% over the last two years. This is due to its large expense base and inefficient cost structure.

Stitch Fix’s operating margin was negative 3.6% this quarter. The company's consistent lack of profits raise a flag.

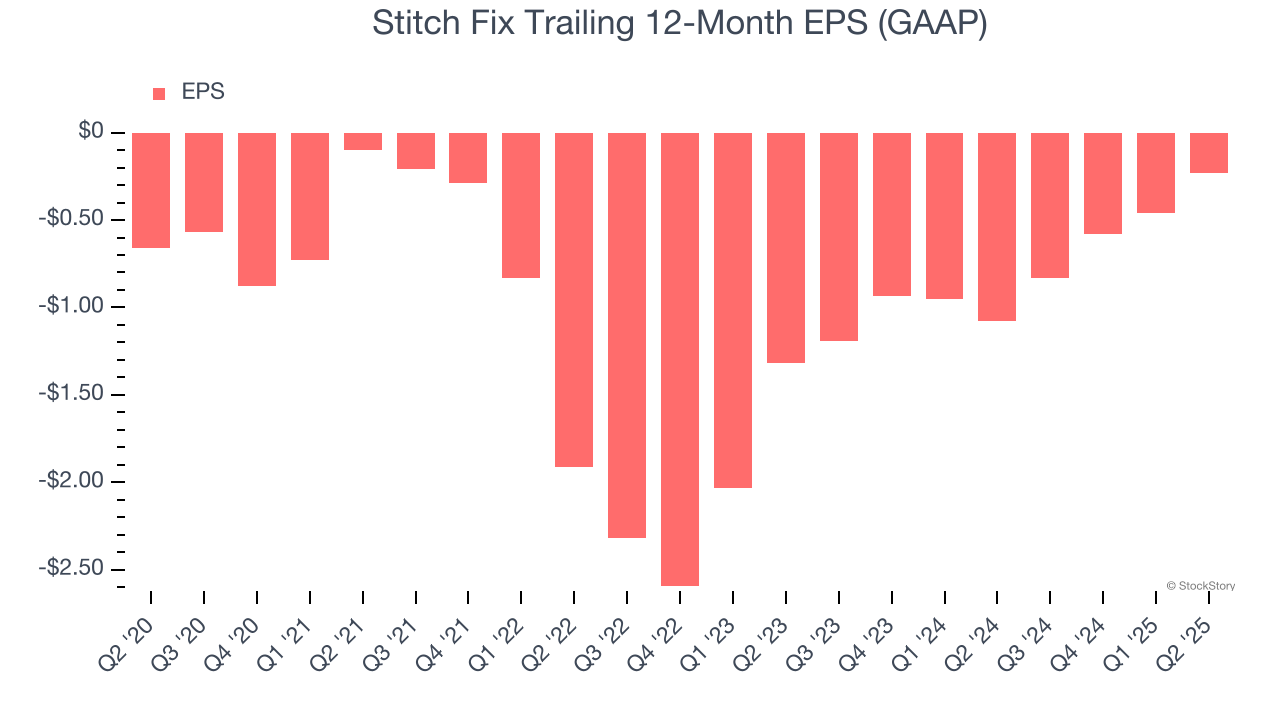

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Stitch Fix’s full-year earnings are still negative, it reduced its losses and improved its EPS by 19.1% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q2, Stitch Fix reported EPS of negative $0.07, up from negative $0.30 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Stitch Fix to perform poorly. Analysts forecast its full-year EPS of negative $0.23 will tumble to negative $0.35.

We were impressed by how significantly Stitch Fix blew past analysts’ EBITDA expectations this quarter. We were also glad its revenue guidance for next quarter trumped Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 12.8% to $6.36 immediately after reporting.

Stitch Fix had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

| Jul-10 | |

| Jun-24 | |

| Jun-17 | |

| Jun-16 | |

| Jun-15 | |

| Jun-15 | |

| Jun-11 | |

| Jun-11 | |

| Jun-10 | |

| Jun-10 | |

| Jun-10 | |

| Jun-10 | |

| Jun-10 | |

| Jun-04 | |

| May-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite