|

|

|

|

|||||

|

|

|

Oil and energy stocks are experiencing a notable surge, with crude prices rising further above $60 a barrel in the last few trading sessions.

The momentum in the commodity price has been driven by a mix of supply constraints, geopolitical tensions, and various market dynamics.

On the supply side, OPEC+ has been gradually unwinding previous production cuts, limiting supply growth as demand continues to recover from the pandemic. Further impacting supply have been sanctions imposed by the U.S. government on Russian and Venezuelan oil.

As far as market dynamics, the International Energy Agency (IEA) has noted that most advanced economies have shown stronger-than-expected oil consumption in 2025. This has coincided with refinery crude throughputs surging to record levels in August, indicating strong demand for refined products like gasoline and diesel fuel.

Keeping this broader scenario in mind, here are three oil and energy stocks that investors may want to consider with a Zacks Rank #1 (Strong Buy).

As an exploration and production company as well as a producer of oil and natural gas, California Resources' CRC strategic execution led to robust Q2 results, exceeding EPS and sales expectations by 20%, respectively. In the wake of its strong Q2 results, full-year EPS estimates for California Resources have now surged more than 15% in the last 60 days for fiscal 2025 and FY26.

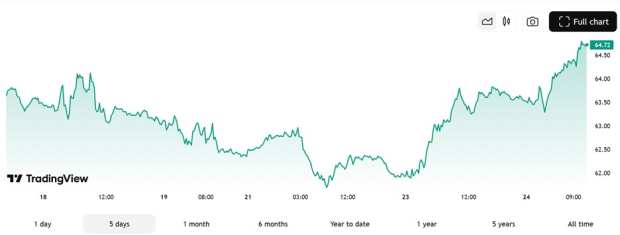

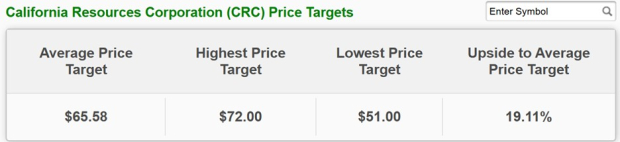

Edging toward its 52-week highs of $60 a share, analysts have remained bullish on CRC stock, with California Resources hitting peaks in free cash flow. Notably, this has supported aggressive shareholder returns, as the company returned a record $287 million to shareholders via buybacks and dividends during Q2. Furthermore, analysts at Bank of America BAC, UBS UBS, and Barclays BCS have raised their price targets for CRC to between $66-$70, citing strong revenue growth and operational discipline.

At the moment, CRC has a generous 2.82% annual dividend yield, and the Average Zacks Price Target of $65.58 a share suggests 19% upside.

Checking the boxes in terms of growth and value, NCS Multistage NCSM provides engineered products and support services for oil and natural gas well completions, along with field development strategies in the United States and internationally.

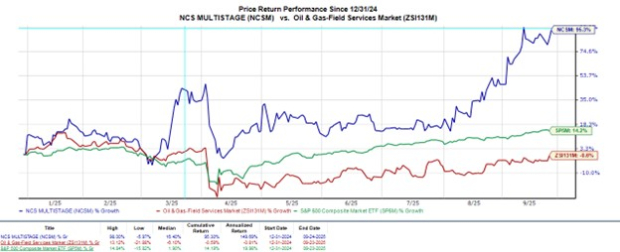

NCS’s capital-light business model and geographic expansion have helped the company outperform its Zacks Oil and Gas-Field Services peers, with NCSM shares skyrocketing +90% YTD compared to its industry’s virtually flat performance and the S&P 500’s return of +14%.

Trading at less than 1X sales, NCS’s top line is expected to increase by 8% in FY25 and FY26, with projections edging toward $200 million. Over the last five years, NCS’s top line has stretched over 50% from annual sales of $107 million in 2020.

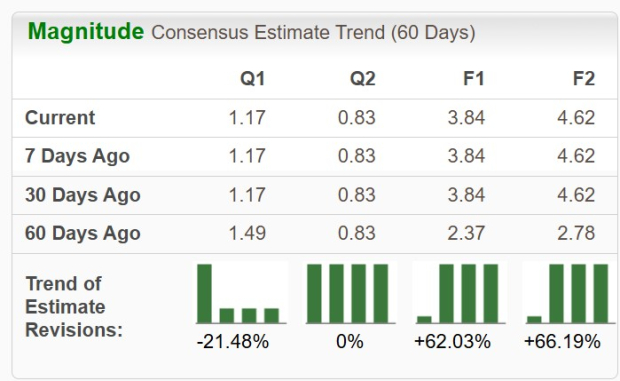

Hovering near a 52-week peak of $51 a share, NCSM also trades at an attractive 12X forward earnings multiple with EPS projected to increase 6% this year and forecasted to spike another 20% in FY26 to $4.62. More intriguing, in the last 60 days, EPS revisions have soared over 60% for FY25 and FY26, as NCS also crushed its most recent quarterly expectations.

Last but not least, Tidewater TDW stands out as a provider of offshore service vessels and marine support to the offshore energy industry. Owning over 200 offshore support vessels, Tidewater is the largest Offshore Support Vessel (OSV) operator in the world.

Appealing to Tidewater’s steady top and bottom line growth trajectory is that it has seen its fiscal 2025 earnings estimates increase 15% over the last two months from projections of $3.14 per share to $3.61. This comes as Tidewater blew away its Q2 earnings expectations by 339% in early August, with quarterly EPS at $1.23 compared to estimates of $0.28. As shown below, Tidewater has now posted a very impressive average earnings surprise of 104.7% over the last four quarters.

Attributed to its operational excellence and strong offshore vessel market strength, Tidewater maintained a record average day rate per vessel of $23,000 on a gross margin of 50.1%.

TDW shares have soared over +20% in the last three months, but are still 27% from a one-year high of $77. Making a further rebound look plausible, Tidewater’s EPS is projected to climb to $5.04 next year, and revisions are up 5% in the last 60 days. Plus, TDW has a reasonable forward P/E multiple of 15X.

Amid the recent surge in crude prices, California Resources, NCS Multistage, and Tidewater have led the rally in oil and energy stocks. Stemming from their strong quarterly reports, more upside could be ahead as these highly ranked oil and energy stocks are already benefiting from a very pleasant trend of rising earnings estimate revisions.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 7 hours | |

| 8 hours | |

| 9 hours | |

| 10 hours | |

| Aug-09 | |

| Aug-08 | |

| Aug-08 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite