|

|

|

|

|||||

|

|

|

Spending on advanced chipmaking equipment is expected to increase sharply in the next five years due to AI.

ASML makes equipment that allows customers to shrink their chips, making them more powerful and efficient.

An attractive valuation and solid earnings growth potential make this chipmaking stock worth buying here.

ASML Holding (NASDAQ: ASML) is one of the most important players in the global semiconductor industry. The Dutch semiconductor equipment giant manufactures machines that play a critical role in helping chipmakers and foundries print advanced chips.

However, ASML stock has been subdued since hitting an all-time high on July 8 last year. It has shed 11% of its value since then, while the broader PHLX Semiconductor Sector index has gained 10% during this period. ASML's underperformance since July last year can be attributed to the potential effect of tariffs on the company's equipment sales, along with its poorer-than-expected guidance for 2025.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

The good part is that ASML stock has started gaining some momentum lately. The stock has jumped 27% in the past month, thanks to positive Wall Street commentary and the strength of the semiconductor market owing to the robust demand for artificial intelligence (AI) chips. It won't be surprising to see ASML sustaining this momentum and delivering solid gains to investors over the next three years.

Let's see why this semiconductor stock is primed for more upside by 2028.

Image source: Getty Images.

The proliferation of AI has played a central role in driving robust growth in semiconductor demand over the last three years. The picture for the next three years seems favorable as well, with Advanced Micro Devices CEO Lisa Su forecasting that sales of AI accelerator chips such as graphics processing units (GPUs) and custom processors are set to increase at an annual pace of 60% through 2028, generating a massive $500 billion in annual revenue.

It won't be surprising to see that happening, given how fast the demand for AI computing in the cloud is increasing. Cloud infrastructure providers such as Oracle, Microsoft, Google, and Amazon don't have enough data center capacity at their disposal to meet customer demand for training and deploying AI models, or for running inference applications in the cloud.

This has led to a massive order backlog at the leading cloud computing companies. For instance, the combined backlog of Amazon, Microsoft, and Google stood at a whopping $669 billion at the end of the previous quarter. Oracle recently reported remaining performance obligations (RPO) worth a whopping $455 billion, up by a massive 359% from the year-ago period.

So, these cloud giants are already sitting on more than $1 trillion in revenue backlog that they need to fulfill. That's the reason why the spending on chipmaking equipment can be expected to accelerate over the next three years, as these companies are likely to keep spending huge amounts of money on setting up data center infrastructure. That's going to create demand for more chips, which in turn will lead to an increase in demand for the chipmaking equipment that ASML sells.

What's worth noting is that the chips used for tackling AI workloads -- be it in data centers, personal computers (PCs), or smartphones -- are manufactured using advanced process nodes. These advanced nodes help make chips with small transistor sizes, usually below 7-nanometer (nm). Not surprisingly, leading chipmakers are looking to make their chips smaller to increase computing performance and reduce energy consumption simultaneously.

ASML is the only company that can help chipmakers print smaller chips with its high NA (numerical aperture) extreme ultraviolet (EUV) lithography machines, which can be used for making chips that are just 2nm in size. This explains why companies such as SK Hynix, Intel, and Samsung have been lining up to purchase ASML's high NA machines to further shrink the size of their process nodes in a bid to manufacture cutting-edge chips.

ASML's monopoly-like position in the EUV lithography market explains why the demand for its equipment is expected to take off. S&P Global estimates that ASML's EUV sales could rise an impressive 49% this year, followed by further growth in unit volumes and the average selling price (ASP) through the end of the decade.

Industry association SEMI is expecting the spending on equipment capable of producing advanced chips to increase to more than $50 billion by 2028, which would be a big jump from last year's outlay of $26 billion. This could pave the way for substantial upside over the next three years.

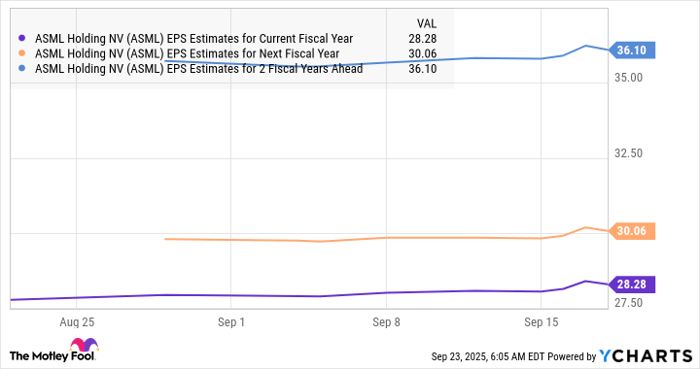

The points discussed above make it clear that ASML has the potential to deliver solid growth over the next three years. Its earnings growth is expected to accelerate remarkably in 2028 following an expected single-digit increase next year.

ASML EPS Estimates for Current Fiscal Year data by YCharts.

What's worth noting is that ASML's net income has increased by 67% in the first six months of 2025 from the same period last year. Given that the company is expected to witness a nice jump in the ASP of its EUV machines over the next three years, especially the high-NA machines, there is a solid chance that it could deliver stronger growth than what analysts are forecasting.

Assuming it can clock even $40 per share in earnings in 2028 and trades at 33 times earnings after three years (in line with the tech-laden Nasdaq-100 index), its stock price could hit $1,320. That would be a 38% increase from current levels. But don't be surprised to see this AI stock delivering much bigger gains. The market could reward it with a premium valuation on account of the potential acceleration in growth.

Before you buy stock in ASML, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and ASML wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $651,593!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,089,215!*

Now, it’s worth noting Stock Advisor’s total average return is 1,058% — a market-crushing outperformance compared to 188% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 22, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends ASML, Advanced Micro Devices, Amazon, Microsoft, and Oracle. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-16 | |

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite