|

|

|

|

|||||

|

|

|

The outdoor industry spans recreation, wellness, and lifestyle experiences centered around nature and activity away from home. This theme includes brands involved in outdoor gear, apparel, recreational vehicles, and equipment and services that support activities such as hiking, camping, boating, and off-roading.

Driven by shifting consumer values toward health, sustainability, and experience-driven living, the industry benefits from steady demand across various age groups and regions. Many companies in this space leverage brand loyalty, product innovation, and direct-to-consumer strategies to drive recurring sales and maintain premium positioning.

Here we recommend three Outdoor Industry stocks with a favorable Zacks Rank that have double-digit price upside potential for fourth-quarter 2025. These are: Carnival Corporation & plc CCL, Norwegian Cruise Line Holdings Ltd. NCLH and Deckers Outdoor Corp. DECK. Each of our picks carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

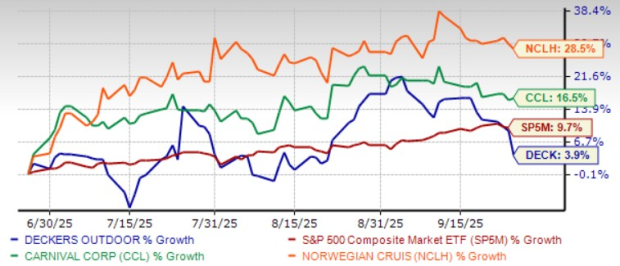

The chart below shows the price performance of our five picks in the past three months.

Carnival has been benefiting from resilient travel demand, stronger booking trends, higher onboard spending, and disciplined cost management. CCL’s solid execution across these areas led management to raise its full-year 2025 guidance, supported by operational efficiencies and strategic growth initiatives. CCL is also prioritizing fleet optimization, new ship launches, and targeted marketing investments to capture rising global demand.

Carnival is aggressively expanding its destination footprint to enhance guest experiences and drive high-margin revenue growth. CCL continues to invest in modern, guest-centric ships to fuel long-term demand.

AIDAdiva, the first vessel completed under the AIDA Evolution refurbishment program, has seen strong post-upgrade performance, prompting six additional AIDA ships to undergo similar transformations. CCL also ordered two newbuilds for AIDA, scheduled for delivery in 2030 and 2032.

Carnival has an expected revenue and earnings growth rate of 6% and 42.3%, respectively, for the current year (ending November 2025). The Zacks Consensus Estimate for current-year earnings has improved 0.5% over the last seven days.

The short-term average price target of brokerage firms for the stock represents an increase of 12.8% from the last closing price of $30.48. The brokerage target price is currently in the range of $26-$43. This indicates a maximum upside of 41.1% and a downside of 14.7%.

Norwegian Cruise Line is benefiting from strong consumer demand, solid onboard spending and benefits realized from strategic growth initiatives. Bookings were strong across all three brands, driving advance ticket sales to a record $4 billion at the end of the second quarter of 2025.

NCLH’s focus on fleet management strategy, including new ship additions and existing fleet enhancements, is encouraging for its long-term prospects. NCLH is investing in systems to support top-line growth. NCLH stated that a new revenue management system is under development, with the first phase expected to be completed by the end of 2025. Early benefits are anticipated by late 2026.

Norwegian Cruise Line has an expected revenue and earnings growth rate of 6% and 13.2%, respectively, for the current year. The Zacks Consensus Estimate for current-year earnings has improved 1% over the last 30 days.

The short-term average price target of brokerage firms for the stock represents an increase of 21.9% from the last closing price of $25. The brokerage target price is currently in the range of $24-$43. This indicates a maximum upside of 72% and a downside of 4%.

Deckers Outdoor’s entered fiscal 2026 with strong momentum, delivering record first-quarter results driven by the strength of HOKA and UGG. Both brands exceeded expectations through innovation, global marketing, wholesale expansion, and robust international demand, especially in Europe and China.

We foresee year-over-year increases of 14.6% and 6.7% in net sales for the HOKA and UGG brands, respectively, in fiscal 2026. DECK’s balanced channel strategy, disciplined execution, and solid financial position support ongoing investments in marketing, digital infrastructure, and selective retail growth.

DECK’s focus on innovation, expanding its consumer reach, and leveraging strong market trends positions it favorably for sustained success. International markets remain the standout driver of DECK’s growth. In the last reported quarter, international revenues surged 49.7% year over year to $463.3 million, significantly outpacing the U.S. revenues.

Deckers Outdoor has an expected revenue and earnings growth rate of 9% and almost flat respectively, for the current year. The Zacks Consensus Estimate for current-year earnings has improved 17.9% over the last 60 days.

The short-term average price target of brokerage firms for the stock represents an increase of 20.9% from the last closing price of $105.83. The brokerage target price is currently in the range of $90-$158. This indicates a maximum upside of 49.3% and a downside of 15%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 3 hours | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite