|

|

|

|

|||||

|

|

|

CrowdStrike is poised to benefit from the most powerful investing megatrend of our time: AI.

Kinsale Capital Group may be more of a Steady Eddie investment, but it is trading at an unusually low valuation.

In less than six months, the S&P 500 and Nasdaq-100 have soared by 33% and 43%, respectively, from their 2025 lows.

Despite those incredible runs for the broader market indexes, I'd argue that plenty of once-in-a-decade opportunities remain available for investors. These two are my favorite bets to surge higher from here.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Cybersecurity juggernaut CrowdStrike (NASDAQ: CRWD) saw its stock price drop by nearly 50% after it rolled out a flawed software update that triggered a global IT outage in July 2024.

At the time, many investors and analysts (rightfully) worried about the repercussions for CrowdStrike in terms of retaining customers -- let alone attracting new ones. However, just over a year after that debacle, the company's shares have doubled in value, powered by reaccelerating sales growth in its latest quarter.

In a weird way, the outage served as a stress test of the moat around CrowdStrike's business. And, quite frankly, it passed with flying colors.

The post-outage period offered customers a perfect opportunity to switch to rival cybersecurity providers, but for the most part, they didn't really jump ship. This stability highlights the switching cost moat surrounding CrowdStrike's operations. Now, distanced from the fiasco, the company is diving into today's biggest megatrend: artificial intelligence (AI). And specifically, securing AI.

Image source: CrowdStrike.

Thanks to its recently announced acquisition of AI security leader Pangea, CrowdStrike now offers an AI detection and response module, similar to its existing endpoint detection and response capabilities.

Now securing all things AI, from large language models (LLMs) to AI agents, CrowdStrike will block prompt injection attacks, prevent risky AI use, and trace AI agents back to their human creators.

Kicking off its foray into defending the AI world, CrowdStrike partnered with Salesforce, a customer relationship management juggernaut, to provide security for its AI agents and applications.

The opportunity from deals like these could be massive for CrowdStrike. Currently, the company believes there are 5 billion addressable assets (cloud workloads, endpoint devices, and human identities) available for it to protect.

However, management predicts that the rise of agentic AI alone could bring in more than 150 billion assets that will need to be secured, creating what CEO and co-founder George Kurtz believes is a "100x" opportunity.

Today, CrowdStrike is trading at 115 times free cash flow and 27 times sales, so the company will need to deliver significant growth to justify its valuation.

However, numerous research firms project that the market for agentic AI will grow roughly sevenfold between 2025 and 2030. If CrowdStrike can become the leader in this new niche (as it already has in its established cybersecurity specialties), it could quickly outgrow what looks like a lofty valuation today.

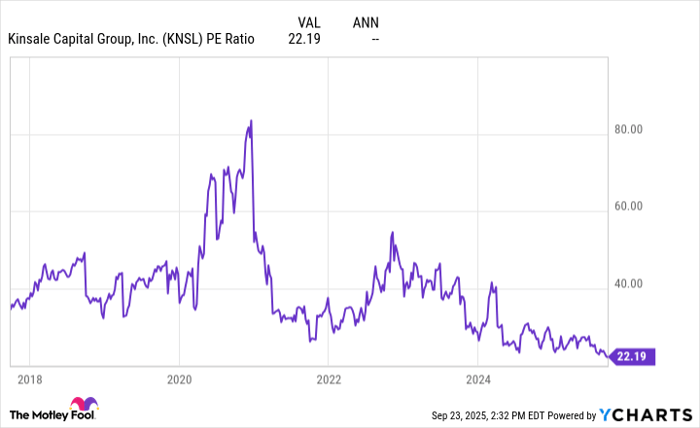

Whereas CrowdStrike's current valuation has a lot of optimism for the future baked into it, excess and surplus (E&S) insurer Kinsale Capital Group (NYSE: KNSL) is trading at the cheapest P/E ratios in its history.

KNSL PE Ratio data by YCharts.

Typically, bargain-bin valuations like these come alongside some pretty serious risks. But that doesn't appear to be the case with Kinsale.

While the company's growth in gross written premiums may have slowed to just 5% in the most recent quarter, earnings per share rose 28%. In fact, Kinsale's combined ratio remained strong at 76%, indicating that the company remains the most profitable insurer in the E&S niche. A combined ratio below 100% means that an insurance company is profitable on its underwriting, and Kinsale's mark of 76% is exceptional. For comparison, its closest peers in the E&S industry averaged a lofty 92% ratio between 2022 and 2024.

Kinsale achieves this unusual profitability by focusing on smaller E&S accounts with hard-to-assess risks -- a category of clientele that its massive insurance peers are less apt to pursue.

However, that doesn't mean that the industry's giants won't occasionally venture into Kinsale's E&S niche when the pricing looks right. Over the past few years, premiums for these types of policies have steadily increased, drawing the attention of larger insurers. As a result, there is now excessive price competition in the niche. That prompted Kinsale to pull back in certain areas, which resulted in the slowdown in premium growth.

Sometimes, when insurance juggernauts stampede into Kinsale's niche with deeply discounted prices, it only makes sense for it to stand back and preserve its profitability, rather than try to undercut them and risk underwriting clients at a loss.

CEO and founder Michael Kehoe gave an example of this at an investing conference in 2023, explaining:

We lost an account earlier this year. ... It was a firearms manufacturer. We quoted the renewal policy at a $170,000 premium. ... We lost that to an MGA [managing general agent] that wrote it for $57,000. ... They wrote it at the low price because they misclassified it. They considered it a sporting goods distributor instead of what the business actually did, which was manufacture firearms.

This story is an oversimplified way to show that investors shouldn't panic about Kinsale's decelerating premium growth. It operates in a cyclical industry, and pricing competition fluctuates over time.

Was it reasonable for the market to bid down Kinsale's share price in response to its slowing growth? Probably -- Kinsale's prior valuations had become lofty. However, it remains the best underwriter in the E&S space, and continues to capture market share steadily.

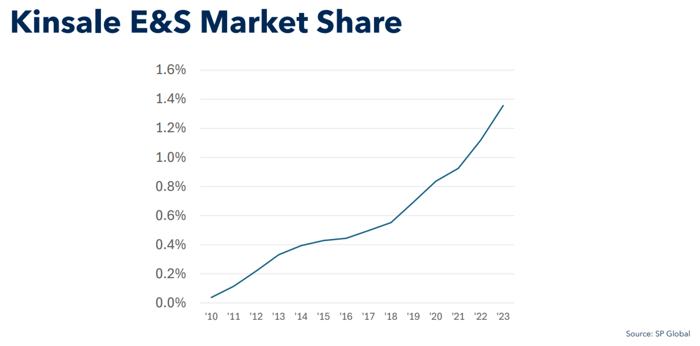

Image source: Kinsale Investor Presentation.

Despite that, Kinsale's market share in the E&S industry remains a mere 1.4%, leaving it with decades of growth potential ahead.

Should it maintain its status as the most profitable insurer in its niche, Kinsale will likely return to its market-beating ways, especially from today's once-in-a-decade low valuation.

Before you buy stock in CrowdStrike, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CrowdStrike wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $651,593!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,089,215!*

Now, it’s worth noting Stock Advisor’s total average return is 1,058% — a market-crushing outperformance compared to 188% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 22, 2025

Josh Kohn-Lindquist has positions in CrowdStrike and Kinsale Capital Group. The Motley Fool has positions in and recommends CrowdStrike, Kinsale Capital Group, and Salesforce. The Motley Fool has a disclosure policy.

| Jul-20 | |

| Jul-18 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite