|

|

|

|

|||||

|

|

|

Carnival Corporation CCL will give the latest glimpse into how cruise operators are faring with its third-quarter results approaching on Monday, September 29.

Despite lingering concerns about its debt load, Carnival’s turnaround story has been captivating as strong demand is allowing the company to avoid heavy discounting, boosting revenue and profit margins.

As the world’s largest cruise operator, Carnival is at the center of what has still been pent-up demand for cruise vacations following the pandemic. Expecting another record year for bookings, Carnival has reported occupancy levels of 104%, with demand surging past its capacity levels.

Even better, Carnival is set to be a prime beneficiary of lower rates, which have already helped with refinancing and reducing its pandemic-era debt.

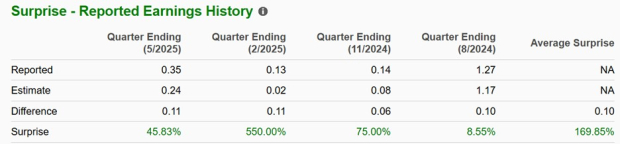

Based on Zacks' estimates, Carnival’s Q3 sales are thought to have increased 2% to what would be a quarterly record $8.07 billion. On the bottom line, Carnival’s earnings are expected to increase 4% to $1.32 per share, versus EPS of $1.27 in the comparative quarter.

Notably, Carnival has exceeded the Zacks EPS Consensus for 11 consecutive quarters with a very impressive average earnings surprise of 169.85% in its last four quarterly reports.

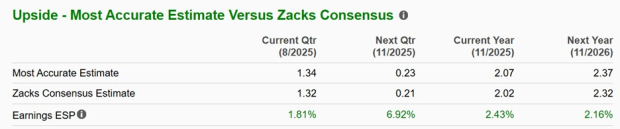

The Zacks ESP (Expected Surprise Prediction) indicates Carnival could once again exceed earnings expectations with the Most Accurate and recent estimate among Wall Street having Q3 EPS pegged at $1.34 and nearly 2% above the underlying Zacks Consensus.

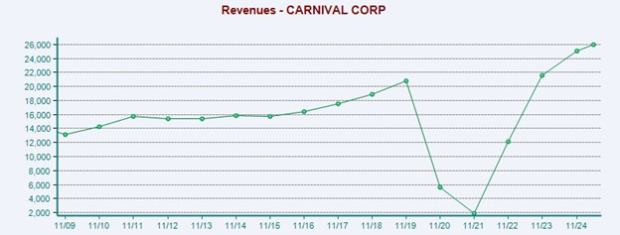

Carnival’s total sales are currently slated to expand 6% in fiscal 2025, with FY26 sales projected to stretch another 4% to $27.56 billion. While this lags the high single-digit outlook for Royal Caribbean Cruises RCL and also trails Norwegian Cruise Line’s NCLH top line growth trajectory, Carnival still brings in the most annual sales.

In terms of annual earnings, Carnival trails Norwegian, although both are far distant from Royal Caribbean’s immense profitability. That said, Carnival’s anticipated 42% EPS growth rate would lead the pack this year, with its annual earnings now expected to climb to $2.02 per share compared to $1.42 in FY24. This also tops its Zacks Leisure and Recreation Services Industry’s average EPS growth forecast of 14.3% and the benchmark S&P 500’s 15.96%.

However, Carnival’s projected FY26 EPS growth rate of 14.85% is expected to trail Norwegian, Royal Caribbean, and their Zacks industry peers, although this would still top the benchmark’s 13.64%. Over the last five years, Carnival’s 28.5% EPS growth rate has roughly matched Norwegian and has impressively topped the industry and S&P 500’s average, but Royal Caribbean has been in a league of its own with a rate of more than 200%.

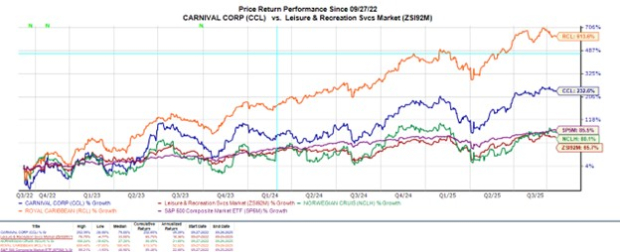

Year-to-date, Royal Caribbean’s stock gains of +40% have led the way. Carnival’s YTD return of more than +20% has also topped the broader indexes, with Norwegian shares down a lackluster 3%. More intriguing, in the last three years, Carnival and Royal Caribbean stock have posted industry and market-leading gains of over +230% and +600%, respectively.

Considering the strengthening outlook for the major cruise operators, Norwegian’s stock is starting to stand out as a buy-the-dip target at around $25 and 12X forward earnings.

Still, Carnival shares have remained attractive as well at $30 and 15.1X forward earnings. This offers a pleasant discount to Royal Caribbean stock, which trades near the Leisure and Recreation Services Industry average of 21X but has a hefty price tag of over $320 a share.

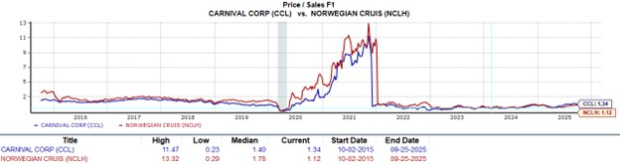

It's noteworthy that Carnival and Norwegian stock are trading under the optimum level of less than 2X forward sales compared to Royal Caribbean’s 5.1X.

Image Source: Zacks Investment Research

Carnival is certainly making the case for being the best cruise stock to invest in at the moment, with CCL sporting a Zacks Rank #2 (Buy). Norwegian stock also shares this favorable ranking, while Royal Caribbean lands a Zacks Rank #3 (Hold), as much of its upside potential appears to be priced in.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite