|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Earlier this month, a judge ruled that Alphabet won't have to divest its Chrome browser.

Risks around a big breakup of the business have been weighing on the stock's valuation.

The company possesses plenty of attractive growth opportunities, ranging from artificial intelligence to the expansion of its robotaxi business, Waymo.

Whenever a publicly traded business faces a big risk or unknown, that can weigh on its valuation. For Alphabet (NASDAQ: GOOG)(NASDAQ: GOOGL), the tech giant that owns Google and YouTube, the big concern recently was that antitrust lawsuits would result in it being forced to sell off key parts of its business.

Although Judge Amit P. Mehta did rule earlier this month that the company has operated a monopoly in search, he did not impose the most severe consequences that federal regulators had asked for. Alphabet still faces a different antitrust case involving its ad tech, but investors were most worried about the possibility of it having to sell its Chrome browser or Android operating system. With those remedies apparently off the table, the stock rallied over the past few weeks. But was that just the start? Can it soar even higher?

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Image source: Getty Images.

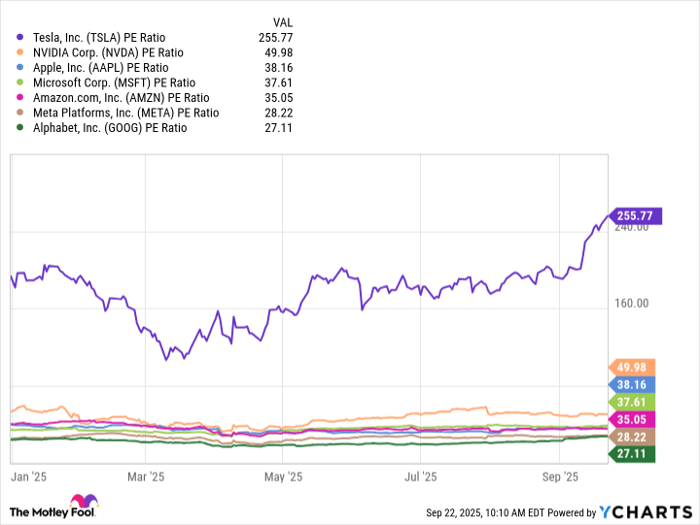

For a while now, Alphabet has been trading at a discounted valuation relative to its earnings. It hasn't been uncommon for it to trade at a price-to-earnings (P/E) multiple below 20, which is low when you consider the average stock on the S&P 500 trades at more than 25 times its trailing earnings.

Alphabet has routinely been one of the most undervalued "Magnificent Seven" stocks, and although it has been rallying recently, it's still the cheapest stock based on its P/E multiple, which currently sits at around 27.

PE Ratio of Magnificent Seven data by YCharts.

Alphabet's relatively modest valuation could attract interest from investors who are looking for potentially underrated artificial intelligence (AI) stocks, especially when you consider its growth potential.

Many investors have been worried about Alphabet's growth outlook, fearing the potential of AI chatbots to divert traffic away from websites and search products, which would cut into its ad revenue. Yet despite the rise of this new tech, its business has continued to generate solid results. Through the first half of 2025, Alphabet generated revenue of $186.7 billion, an increase of 13% from the same period last year. And its net income rose by 33% to $62.7 billion.

What's most exciting about the business, however, is what lies ahead. Its own AI chatbot, Gemini, has around 400 million monthly users. The huge advantage the company has over others in the AI space is that it can train its models on YouTube videos. Its video-generation model, Veo 3, features cutting-edge capabilities that make it easy to make AI-powered videos that are virtually indistinguishable from real videos. AI isn't a risk for Alphabet -- it's a massive opportunity.

And then there are its self-driving Waymo vehicles. Alphabet continues to expand its autonomous taxi business into new markets. Earlier this year, Waymo hit 10 million robotaxi trips, and there's a lot more growth to come. I've taken a couple of Waymo rides and can see that there's tremendous potential for this business.

Alphabet has a wealth of growth opportunities, which is why I believe that even if it had to sell off some parts of its business, that wouldn't necessarily be a bad thing for shareholders. Such a result could help it unlock a lot of value, and might result in investors looking more closely at the true worth of its individual business units.

Alphabet's market cap recently hit $3 trillion, and year to date, its shares are up over 30%. But there could be far more upside for the tech company in the long run, given how plentiful its growth opportunities are and how relatively undervalued it still is. For long-term investors, Alphabet should be a no-brainer growth stock to load up on right now.

Before you buy stock in Alphabet, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $651,593!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,089,215!*

Now, it’s worth noting Stock Advisor’s total average return is 1,058% — a market-crushing outperformance compared to 188% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 22, 2025

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 29 min | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite