|

|

|

|

|||||

|

|

|

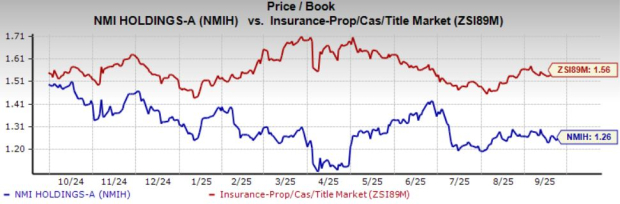

Shares of NMI Holdings, Inc. NMIH are trading at a discount compared to the Zacks Insurance - Property and Casualty industry. Its price-to-book value of 1.26X is lower than the industry average of 1.56X.

However, shares of other insurers such as American Financial Group, Inc. AFG and Kinsale Capital Group, Inc. KNSL are trading at a multiple lower than the industry average.American Financial is trading at 2.69 and Kinsale Capital is trading at 5.67. However,CNA Financial Corporation CNA is trading at a discount at 1.18.

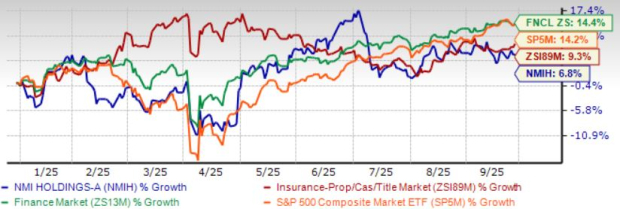

Shares of NMI Holdings have lost 6.8% year to date, underperforming its industry, the Finance sector, and the Zacks S&P 500 Composite’s growth of 9.3%, 14.4% and 14.2%, respectively, in the same time frame.

The insurer has a market capitalization of $3.1 billion. The average volume of shares traded in the last three months was 0.4 million.

The Zacks Consensus Estimate for NMIH’s 2025 earnings per share indicates a year-over-year increase of 9.3%. The consensus estimate for revenues is pegged at $698.5 billion. The consensus estimate for 2026 earnings per share and revenues indicates an increase of 3.8% and 4.7%, respectively, from the corresponding 2025 estimates. The expected long-term earnings growth rate is 7.1%.

The Zacks Consensus Estimate for both 2025 and 2026 earnings has increased 0.2% in the past 30 days.

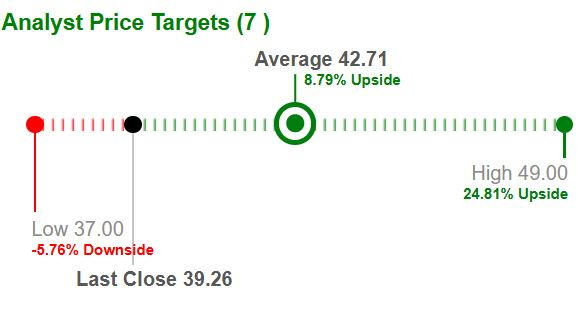

Based on short-term price targets offered by seven analysts, the Zacks average price target is $42.71 per share. The average suggests an 8.8% upside from the last closing price.

Return on equity (ROE) for the trailing 12 months was 14%, comparing favorably with the industry’s 6.1%. This reflects its efficiency in utilizing shareholders’ funds.

Return on invested capital in the trailing 12 months was 13%, better than the industry average of 5.9%, reflecting NMIH’s efficiency in utilizing funds to generate income.

NMI Holdings is steadily building long-term value by leveraging both favorable market conditions and disciplined execution. A strong housing market, growing reliance on private mortgage insurance, and steady opportunities to write new policies and expand insurance in force are creating a solid foundation. Together, these factors form the key organic drivers that continue to support the company’s growth path.

As favorable market forces set the stage, NMIH has been translating that momentum into a stronger market presence. The company is expanding its customer base, strengthening long-term partnerships and managing a portfolio focused on prime residential loans. Its emphasis on resilience, consistent profitability and client-focused growth continues to solidify its standing in the private mortgage insurance sector.

Building on its expanding market presence and strengthened partnerships, NMIH also focuses on cultivating a culture rooted in customer orientation and innovation. Coupled with disciplined portfolio growth and operational efficiency, this balanced approach bolsters profitability, reinforces capital strength, and underpins sustainable shareholder returns.

Even with strong organic growth, NMIH faces some challenges that could affect its profitability. Higher defaults across a larger policy base, along with portfolio seasoning and increased reserves per default outside disaster areas, have led to higher claim costs. In the future, a further rise in defaults could lead to higher claims and reserve needs, putting pressure on margins.

On top of this, competitive moves such as repricing, portfolio adjustments, or changes in underwriting to gain market share from government or private insurers may weigh on revenues and increase operating costs.

Along with rising claim costs and competitive pressures, NMI Holdings is facing a growing debt burden, which stood at $416 million as of June 30, 2025. Maintaining consistent debt servicing remains critical, as any disruption could weaken the company’s credit profile and restrict its financial flexibility.

Overall, NMI Holdings is supported by strong organic growth, a resilient housing market, and a customer-focused strategy that drives profitability and capital strength. However, rising claim costs, competitive pressures and a growing debt burden pose risks that could limit margins and financial flexibility.

Ongoing headwinds limit the potential for meaningful upside for NMI Holdings. It is therefore wise to adopt a wait-and-see approach on this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite