|

|

|

|

|||||

|

|

|

Wayfair breezed past bottom-line estimates in its last two reports.

The company just reported its fastest revenue growth since 2021.

The business needs more improvement for the stock to go higher.

Few stocks were hit as hard in the post-pandemic shift as Wayfair (NYSE: W), the online home furnishings retailer. Wayfair benefited from multiple trends during the pandemic. First, e-commerce sales spiked as consumers took to online shopping instead of visiting stores, and the need to work and learn remotely drove a surge in demand for home furnishings. In general, spending on the home rose during the pandemic as consumers spent money on home improvement that otherwise might have gone to travel or entertainment.

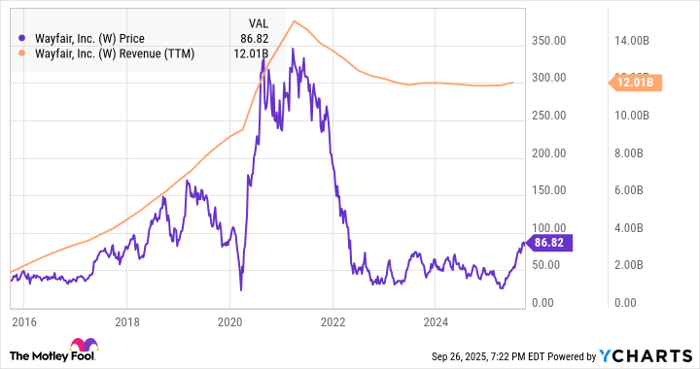

When the pandemic ended, those trends suddenly reversed, and Wayfair was left having overinvested to operate in an economy that no longer needed it. Since then, the stock has mostly chugged along well below its earlier peak. As you can see from the chart below, its revenue is still well below its peak during the pandemic, as it has essentially been flat since then.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Data by YCharts; TTM = trailing 12 months.

However, you'll notice on the right that Wayfair's stock price has started climbing in recent months. The stock is up 339% from its bottom in April to now, despite the threat of tariffs.

Since the April sell-off, the company has fended off concerns about tariffs and delivered a pair of strong earnings reports that show that the business may be finally hitting an inflection point after years of cutting costs and investing in technology in the post-pandemic era.

In its first-quarter earnings report, the company reported flat revenue at $2.7 billion, but delivered a significant improvement on the bottom line. It reported adjusted earnings per share of $0.10, up from a loss of $0.32 in the quarter a year ago.

Its second-quarter results were even stronger as the company reported its fastest revenue growth and highest profitability since 2021. Revenue rose 6% (including the impact of its exit from the German market) to $3.3 billion, which was well ahead of estimates at $3.12 billion.

Adjusted earnings per share jumped from $0.47 to $0.87, which beat the consensus at $0.33. For the third quarter, management predicted revenue growth in the low to mid-single digits.

Wayfair continues to tout market share gains, and it's opening large-scale stores, grabbing a piece of the brick-and-mortar retail market as well. The company opened one in the Chicago suburbs, and it seems to be pleased with the results since it already has three more planned. These are huge big-box stores, and the latest one, in Denver, is expected to be about 140,000 square feet.

Despite the momentum in the business, Wayfair still has a long way to go to reclaim the growth rate it had before the pandemic, and it may never get there.

It has established itself as the leading pure-play online retailer, but it still faces a wide range of competition, including from Amazon, IKEA, Williams-Sonoma, and other big-box and independent stores.

The home furnishings sector has struggled in the last few years for reasons similar to Wayfair. A sluggish housing market has also put a damper on the sector, as home purchases and relocations tend to trigger purchases of furniture.

Investors are hopeful that interest rate cuts from the Federal Reserve will lower mortgage rates and drive a recovery in stocks like Wayfair, but that will take time if it happens.

In some ways, the recovery in the stock is understandable as it looks to be moving past the doldrums of the last few years, but its valuation seems hard to justify, at least not without faster revenue growth.

The stock currently trades at a forward P/E above 40, and there are limitations to its margin improvement without faster revenue growth. If the housing market cooperates, Wayfair could deliver stronger growth, but until then, this rally looks like it has run its course.

Before you buy stock in Wayfair, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Wayfair wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $652,872!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,092,280!*

Now, it’s worth noting Stock Advisor’s total average return is 1,062% — a market-crushing outperformance compared to 189% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 29, 2025

Jeremy Bowman has positions in Amazon. The Motley Fool has positions in and recommends Amazon and Williams-Sonoma. The Motley Fool recommends Wayfair. The Motley Fool has a disclosure policy.

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 | |

| Feb-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite