|

|

|

|

|||||

|

|

|

Douglas Elliman is the fifth largest real estate brokerage company in the U.S., but it's a leader in the high-end luxury segment.

The company managed to grow its revenue during the first half of 2025, despite U.S. existing home sales hovering at a five-year low.

Douglas Elliman stock is trading at a rock-bottom valuation, which could pave the way for a threefold return (or more).

On Sept. 17, the U.S. Federal Reserve cut the federal funds rate (overnight interest rate) for the first time in 2025. According to the central bank's guidance, and Wall Street's estimates, there could be two more interest rate cuts before this year is over.

Lower interest rates are a massive tailwind for the real estate industry, because they increase consumers' borrowing power, which makes it much easier to buy a home. Douglas Elliman (NYSE: DOUG) is the fifth-largest residential real estate brokerage firm in the U.S., and its business could be on the cusp of a major growth phase if falling rates drive a surge in real estate transactions.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

I started accumulating Douglas Elliman stock earlier this year. It's trading at around $3 as I write this, but here's why I think it could be heading back to its 2021 record high of $11, and perhaps beyond.

Image source: Getty Images.

Douglas Elliman was founded in New York more than a century ago, and it now employs around 6,600 agents in 111 offices across the country, focusing on high-end real estate markets in New York City, the Hamptons, California, Florida, California, Texas, and more.

Douglas Elliman sold $36.4 billion worth of real estate in 2024, and it's on track to beat that in 2025 with $20.1 billion in transactions during the first half of the year alone. It's the go-to choice for sellers of luxury real estate, boasting an average transaction price of $1.9 million which is much higher than most of its competitors.

But Douglas Elliman isn't resting on its success. Earlier this year, the company launched its own in-house mortgage platform called Elliman Capital, which will help buyers access the financing they need to get deals over the line. This makes Douglas Elliman's service even more convenient, but it also unlocks an entirely new revenue stream for the company.

Douglas Elliman makes most of its money through its brokerage business, which takes a fee based on the sale price of each home. The company generated $524.7 million in total revenue during the first half of 2025, which was up 8% compared to the same period last year, despite U.S. existing home sales hovering around the lowest point in five years.

The fact Douglas Elliman is growing in such a tough real estate market is a testament to the strength of its brand. The company is also improving its bottom line by carefully managing costs to create a more sustainable business. It still lost $28.6 million during the first half of 2025 on a generally accepted accounting principles (GAAP) basis, but that was an improvement from its $43.1 million net loss from the year-ago period.

Plus, after stripping out one-off and non-cash expenses, Douglas Elliman actually delivered positive adjusted (non-GAAP) earnings before interest, tax, depreciation, and amortization (EBITDA) of roughly $260,000, which was a big swing from the $14.7 million adjusted EBITDA loss it generated in the year-ago period.

But it gets better, because the company also has a strong balance sheet with $136.3 million in cash on hand. It does have $50 million in convertible debt, but it probably won't have to repay the principal because the loan can be converted into stock at a price of $1.50 per share in 2029. Since Douglas Elliman stock currently trades at $3, the lender would be remiss not to take up the equity as things stand.

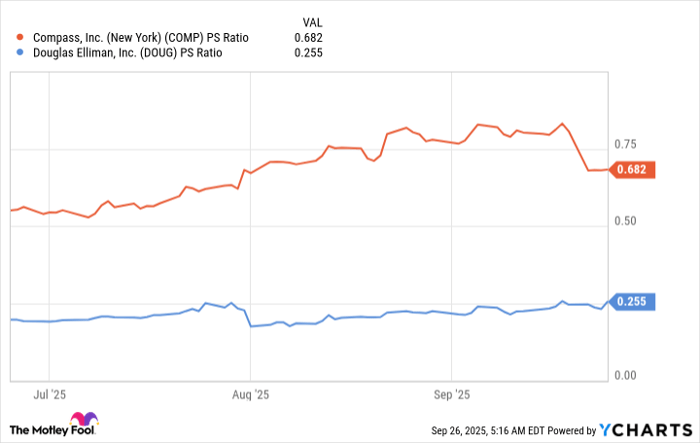

Douglas Elliman has a market capitalization of just $275 million, so the company's trailing 12-month revenue of $1.03 billion places its stock at a price-to-sales (P/S) ratio of just 0.26.

Its P/S ratio was more than three times higher during the last real estate boom in 2021, so if falling interest rates reignite home sales, I think investors are likely to rerate the stock's current valuation. However, there is also an argument that Douglas Elliman should be trading higher right now, regardless.

Compass (NYSE: COMP), which is America's largest residential real estate brokerage company, trades at a P/S ratio of 0.68, which is 172% higher than Douglas Elliman's P/S ratio. Compass stock deserves a premium because it's the market leader, but I would argue the valuation gap is too wide considering the quality of Douglas Elliman's business.

COMP PS Ratio data by YCharts

But that's not all. If we rewind back to July, residential real estate brokerage company Redfin was acquired by Rocket Companies (NYSE: RKT) for $1.75 billion, which translated to a P/S ratio of around 1.7 at the time. That is a substantial premium to where Douglas Elliman is trading.

Finally, Reuters reported that Douglas Elliman rejected a takeover bid valued at $5 per share earlier this year, so there is interest in the company even at a significant premium to where it's currently trading.

If the stock reclaims its 2021 record high of $11, its P/S ratio would still be below 1. Therefore, I think there's a real chance it happens over the next couple of years, as long as interest rates trend lower and the housing market recovers.

Before you buy stock in Douglas Elliman, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Douglas Elliman wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $652,872!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,092,280!*

Now, it’s worth noting Stock Advisor’s total average return is 1,062% — a market-crushing outperformance compared to 189% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 29, 2025

Anthony Di Pizio has positions in Douglas Elliman. The Motley Fool has positions in and recommends Rocket Companies. The Motley Fool has a disclosure policy.

| 8 hours | |

| 9 hours | |

| 10 hours | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite