|

|

|

|

|||||

|

|

|

Costco's great business model just delivered another record year.

Membership income drives profit growth, and there are some signs of a slowdown.

On Sept. 25, Costco Wholesale (NASDAQ: COST) reported completed financial results for its fiscal 2025. And the stock immediately dropped. To be clear, the drop for Costco stock was extremely modest at around 3%. But a drop of any size would seem to indicate that investors were unenthused with the company's financial results, at best. And at worst, they're concerned.

I believe that investors are leaning more toward the concerned side of the spectrum when it comes to Costco. As a retailer, same-store sales (or comparable sales) are an important metric. For the fourth quarter, the company's comparable sales were up 5.7%. That's good, but lower than expected.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Is this really a big deal for Costco investors with a long-term perspective? Here are some things for investors to consider.

Image source: Costco Wholesale.

Costco's business model is fascinating. The company is enormous, with net sales of $270 billion in its fiscal 2025 (which ended on Aug. 31). And it aims to be the low-cost leader. In fact, it barely makes a profit at all on its merchandise, considering its gross profit margin for merchandise is a paltry 11%. After figuring in additional operating expenses, profits are thin for Costco.

Costco's aim is for its members to save money, so don't expect it to raise prices to boost profits. Rather, the company makes its money by selling memberships for an annual fee.

In other words, Costco's existing customers could significantly increase their spending overnight, and it wouldn't make an outsized impact overall because merchandise gross margin is so low. The bulk of its profits would still be coming from its membership fees.

By choosing to do business this way -- charging a membership fee and selling stuff for cheap -- Costco tends to attract loyal customers, giving it a competitive edge over some other retailers.

Based on how the model works, revenue from membership fees is the most important metric for Costco, not comparable sales. That said, comparable sales aren't insignificant when thinking about membership trends.

Consider that Costco ended Q4 with 81 million total paid memberships. That was up 6.3% year over year. But remember that comparable sales were only up 5.7%. In other words, it would seem that most (if not all) of the comparable-sales gain came from new Costco members.

Furthermore, membership renewal rates slipped slightly for Costco. In Q4, the renewal rate was 90% and management said that newer members who have signed up online aren't renewing as well as other cohorts.

A pessimist would read these tea leaves and deduce that Costco members aren't increasing their spending and more are canceling than usual, pointing to a sales decline in the near future.

I think that's taking it too far. After all, Costco still delivered record financial results that were among the best in the business. But it perhaps helps explain why Costco stock didn't jump after its Q4 report.

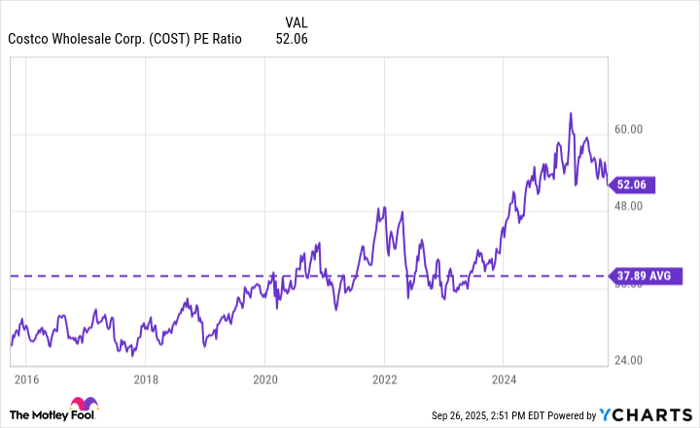

Many have likely already heard about the pricey valuation of Costco stock, but stick with me. As of this writing, it trades at over 50 times its earnings, which is close to its highest valuation ever and close to double the valuation of the S&P 500.

Data by YCharts.

I think almost everyone would agree that Costco stock isn't undervalued. So let's pretend that it's as fairly valued as it could possibly be. Assuming it's fairly valued, investors shouldn't expect the market to give it a higher valuation from here, but rather, they should expect the valuation to stay the same.

If the valuation for Costco stock stays the same over the next five years, then the share price will increase at the same rate as the company's earnings per share (EPS) -- that's how valuation works.

Seasoned investors know that the S&P 500 goes up around 10% annually on average, so Costco will need to grow profits at that rate to keep up with the market average. But can the company grow its EPS by 10% or more annually from here? It's a tall order.

Yes, Costco grew its full-year EPS by 10% in its fiscal 2025. But investors should keep in mind that the company raised the fee for its memberships during the fiscal year, which contributed to the increase. This is something that management does infrequently.

Putting it all together, Costco is growing memberships at a modest pace, and membership income is one of the biggest drivers of its overall profit. Assuming this modest growth continues, Costco stock could struggle to outperform the market in a best-case scenario. And in a worst-case scenario, the valuation would come down, dragging down the stock price.

In conclusion, Costco remains a great company, and its fiscal 2025 financial results proved it once again. But slow growth combined with a high valuation could lead to lower returns for investors.

Before you buy stock in Costco Wholesale, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Costco Wholesale wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $652,872!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,092,280!*

Now, it’s worth noting Stock Advisor’s total average return is 1,062% — a market-crushing outperformance compared to 189% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 29, 2025

Jon Quast has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Costco Wholesale. The Motley Fool has a disclosure policy.

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-19 | |

| Jul-19 | |

| Jul-19 | |

| Jul-18 |

Costco Gas Pumps Are So Popular the Retailer Is Building Stand-Alone Stations

COST

The Wall Street Journal

|

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite