|

|

|

|

|||||

|

|

|

PDD Holdings is a multinational commerce group that owns and operates a portfolio of businesses. The company aims to bring more people into the digital economy so that local communities and small businesses can benefit from increased productivity and new opportunities.

This e-commerce stock is displaying relative strength, widely outperforming the general market off the April lows. Increasing volume has attracted investor attention as buying pressure accumulates in this top-ranked stock.

A Zacks Rank #1 (Strong Buy), PDD Holdings is part of the Zacks Internet - Commerce industry group, which currently ranks in the top 16% out of approximately 250 industries. Because this group is ranked in the top half of all Zacks Ranked Industries, we expect it to outperform the market over the next 3 to 6 months.

Take note of the favorable characteristics for this group below. Stocks in this industry are relatively undervalued based on traditional valuation metrics. They are also projected to experience above-average earnings growth, which signifies a powerful combination that should lead to higher prices in the future.

Historical research studies suggest that approximately half of a stock’s price appreciation is due to its industry grouping. In fact, the top 50% of Zacks Ranked Industries outperforms the bottom 50% by a factor of more than 2 to 1.

It’s no secret that investing in stocks that are part of leading industry groups can give us a leg up relative to the market. By focusing on leading stocks within the top industries, we can dramatically improve our stock-picking success.

PDD operates Pinduoduo, an e-commerce platform which offers products in various categories such as agricultural produce, apparel, food and beverage, furniture and household goods, cosmetics, fitness items, and auto accessories.

PDD also conducts business under cross-border platform Temu, its international e-commerce arm that enables merchants to streamline their manufacturing and commercial operations. Temu is seen as a possible contender to Amazon in the United States.

PDD Holdings PDD has established a healthy track record of beating earnings estimates. The company exceeded the EPS mark in two of the past three quarters. Back in August, PDD reported second-quarter earnings of $3.08 per share, which marked a 61.3% surprise over the $1.91/share consensus estimate.

The leading e-commerce player delivered a 6.4% average earnings surprise over the last four quarters. Consistently beating earnings estimates is a recipe for success.

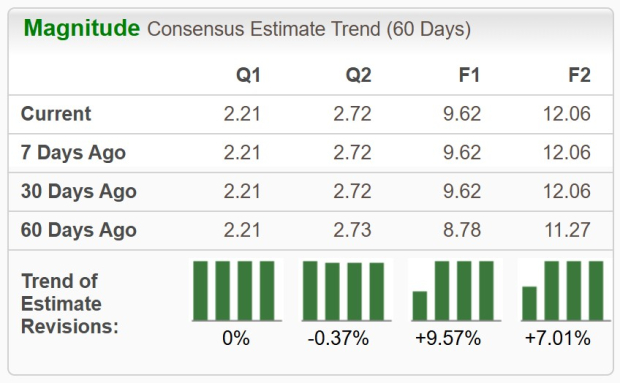

Analysts covering PDD are mainly in agreement and have been raising earnings estimates lately. Looking ahead to next year, EPS estimates have been increased by +7.01% in the past 60 days. The fiscal 2026 Zacks Consensus Estimate now stands at $12.06/share, reflecting potential growth of over 25% relative to this year. Revenues for the full year are projected to climb nearly 16% to $69.15 billion.

This market leader has seen its stock advance about 50% off the April lows. Only stocks that are in extremely powerful uptrends are able to experience this type of outperformance. This is the kind of stock we want to include in our portfolio – one that is trending well and receiving positive earnings estimate revisions.

Notice how both the 50-day (blue line) and 200-day (red line) moving averages are sloping up. The stock has been making a series of higher highs and recently hit a year-to-date high. With both strong fundamental and technical indicators, PDD stock is poised to continue its outperformance.

Empirical research shows a strong correlation between near-term stock movements and trends in earnings estimate revisions. As we know, PDD Holdings has recently witnessed positive revisions. As long as this trend remains intact (and PDD continues to deliver earnings beats), the stock will likely continue its bullish run.

We are beginning to see signs of emerging market equities turning the page on the last (nearly) two decades of underperformance. Emerging market valuations are simply much more attractive relative to domestic; for example, PDD trades at just 13.6 times forward earnings.

Backed by a leading industry group and history of earnings beats, it’s not difficult to see why PDD stock is a compelling investment. Robust fundamentals combined with an appealing technical trend certainly justify adding shares to the mix.

Recent positive earnings estimate revisions should also serve to create a ‘floor’ in terms of any sudden or unexpected downside moves. If you haven’t already done so, be sure to put PDD on your watchlist.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-14 | |

| Jul-13 | |

| Jul-10 | |

| Jun-16 | |

| Jun-09 | |

| May-28 | |

| May-28 | |

| May-27 | |

| May-27 | |

| May-27 | |

| May-27 | |

| May-27 | |

| May-27 |

Temu Owner PDD Posts Profit Miss Amid Fierce Competition in China

PDD -10.38%

The Wall Street Journal

|

| May-27 | |

| May-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite