|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

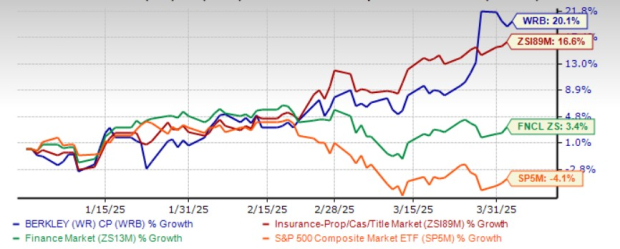

Shares of W. R. Berkley Corporation WRB have gained 29.1% year to date, outperforming its industry, the sector and the Zacks S&P 500 composite’s return in the same time frame.

W. R. Berkley shares are trading well above the 50-day moving average, indicating a bullish trend.

WRB, one of the nation’s largest commercial lines property casualty insurance providers, has a market capitalization of $26.7 billion. The average volume of shares traded in the last three months was nearly 2 million.

WRB shares are trading at a premium to the industry. Its price-to-book value of 3.16X is higher than the industry average of 1.66X.

Other insurers, such as Arch Capital Group ACGL, CNA Financial CNA and Cincinnati Financial CINF, are also trading at a premium to the industry.

Return on equity for the trailing 12 months was 20.6%, comparing favorably with the industry’s 8.3%. This reflects its efficiency in utilizing shareholders’ funds. It envisions a long-term target of 15%.

Also, return on invested capital (ROIC) has been increasing over the last few quarters while the company raised its capital investment over the same time frame. This reflects WRB’s efficiency in utilizing funds to generate income. ROIC in the trailing 12 months was 10%, better than the industry average of 6.4%.

W.R. Berkely operates in areas where it has a competitive advantage that is likely to accelerate growth. Thus, the insurer focuses on commercial lines, including excess and surplus lines, admitted lines and specialty personal lines.

Its insurance business is poised to grow on the strength of several new startup units in various business lines and the expansion of international business, which offers diversification benefits, rate increases, market dislocations and high retention.

As part of its international expansion, WRB is focused on venturing into attractive global markets and thus has operations in emerging markets of the United Kingdom, Continental Europe, South America, Canada, Scandinavia, Asia and Australia.

This insurer boasts more than 60 straight quarters of favorable reserve development on the strength of its prudent underwriting. W.R. Berkley maintains a solid balance sheet with sufficient liquidity and strong cash flows.

The Zacks Consensus Estimate for 2025 and 2026 earnings has moved 1 cent north each in the past 30 days, reflecting analyst optimism.

The Zacks Consensus Estimate for 2025 earnings is pegged at $4.34, suggesting an increase of 4.8% on 6.7% higher revenues of $14.4 billion. The consensus estimate for 2026 earnings is pegged at $4.72, suggesting an increase of 8.7% on 8.6% higher revenues of $15.7 billion.

The long-term earnings growth rate is expected to be 8.2%, better than the industry average of 7.6%.

Based on short-term price targets offered by 16 analysts, the Zacks average price target is at $66.56 per share. The average suggests a potential 4.6% downside from the last closing price.

Better pricing, reserving discipline, diversification benefits, momentum in international business, investment in alternative assets and consistent cash flow poise the insurer for growth.

W.R. Berkley has been hiking dividends since 2005. Its dividend yield of 0.5% appears attractive compared with the industry average of 0.3%, making it an attractive pick for yield-seeking investors. It also has a VGM Score of A.

WRB’s unfavorable leverage, as well as times interest earned, keeps us cautious. Rising expenses have been weighing on margins.

Thus, given its premium valuation, it is better to adopt a wait-and-see approach for this Zacks Rank #3 (Hold) stock in the near term. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-19 | |

| Feb-19 | |

| Feb-18 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite