|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

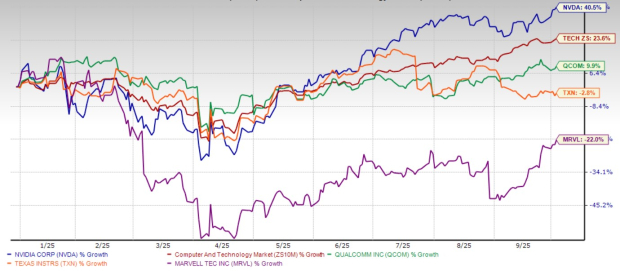

NVIDIA Corporation NVDA has had a remarkable run so far this year, with its shares hitting a new 52-week high of $191.05 on Thursday. The stock has been a key beneficiary of the artificial intelligence (AI) boom, which has driven strong demand for its graphics processing units (GPUs) and computing solutions.

Year to date, NVIDIA shares have soared 40.5%, outperforming the Zacks Computer and Technology sector’s growth of 23.6%. It has even outpaced major semiconductor companies, including QUALCOMM QCOM, Texas Instruments TXN and Marvell Technology MRVL. QUALCOMM’s stock has gained 9.9% year to date, while shares of Texas Instruments and Marvell Technology have fallen 2.8% and 22%, respectively.

This outperformance shows investors are becoming increasingly confident in NVIDIA’s long-term prospects, even in a volatile market shaped by trade conflicts and geopolitical risks. We believe this momentum is grounded in strong fundamentals, and NVDA’s long-term outlook justifies a hold position for now.

NVIDIA’s most powerful growth engine continues to be its Data Center business. In the second quarter of fiscal 2026, the segment generated $41.1 billion in revenues, representing 87.9% of total sales. This marked a staggering 56% year-over-year increase and 5% sequential growth.

The robust performance was mainly driven by higher shipments of the Blackwell GPU computing platforms that are used for the training and inference of large language models, recommendation engines and generative AI applications.

The demand for NVIDIA’s Hopper 200 and Blackwell GPU computing platforms has been a key catalyst as cloud providers and enterprises scale their AI infrastructure. Large cloud service providers contributed to the majority of Data Center revenues, indicating continued hyperscale investment in AI-driven computing.

With AI adoption accelerating across industries, NVIDIA's stronghold in data centers makes it a critical beneficiary of this trend. The company’s leadership in AI chip development positions it well for sustained revenue growth in this segment.

Despite ongoing macroeconomic challenges, geopolitical issues, and trade and tariff wars, NVIDIA’s financials remain rock solid. In the second quarter of fiscal 2026, revenues jumped 56% from the year-ago quarter, while non-GAAP earnings per share rose 54%.

The company reported a non-GAAP gross margin of 61%, maintaining profitability despite rising operational expenses. Non-GAAP operating income jumped 51% year over year to $30.17 billion, reflecting the company’s ability to convert strong revenue growth into bottom-line gains.

NVIDIA’s outlook for the third quarter of fiscal 2026 remains upbeat. The company expects third-quarter revenues to increase 55% year over year to $54 billion, reflecting continued momentum in AI-driven demand. The gross margin is expected to be strong at 73.5% despite increasing costs associated with ramping up Blackwell production.

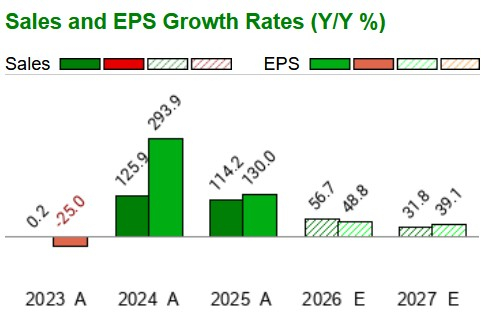

The Zacks Consensus Estimate for fiscal 2026 and 2027 indicates continued growth momentum for the company’s top and bottom lines.

NVIDIA’s cash flow generation also remains robust. It generated a free cash flow of $13.45 billion in the fiscal second quarter and $39.58 billion in the first half of fiscal 2026. The company ended the fiscal second quarter with $56.79 billion in cash, cash equivalents and marketable securities, up from $53.7 billion in the previous quarter.

This strong liquidity position enables NVIDIA to reinvest in research and development, expand manufacturing capabilities, and return capital to shareholders. In the fiscal second quarter, the company returned $244 million to its shareholders through dividend payouts and repurchased stocks worth $9.72 billion. In the first half of fiscal 2026, NVIDIA paid out $488 million in dividends and bought back shares worth $23.82 billion.

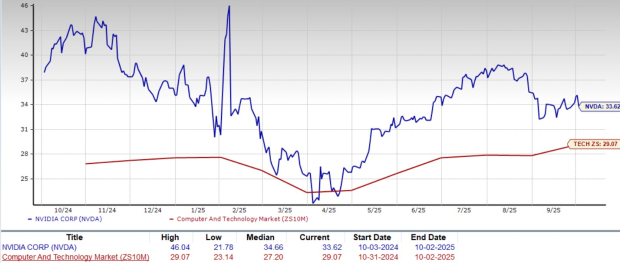

Valuation-wise, NVIDIA is overvalued, as suggested by the Value Score of D.

In terms of forward 12-month Price/Earnings (P/E), NVDA shares are trading at 33.62X, higher than the sector’s 29.07X.

Also, NVIDIA is trading at a higher P/E multiple than other major semiconductor players, including QUALCOMM, Marvell Technology and Texas Instruments. At present, QUALCOMM, Marvell Technology and Texas Instruments trade at P/E multiples of 14.2x, 27.14x and 29.28x, respectively.

NVIDIA’s strong fundamentals, dominant position in AI and impressive growth outlook make a compelling case for staying invested. While valuation is on the higher side, the company’s momentum, both operationally and financially, supports holding the stock.

NVIDIA carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 37 min | |

| 37 min | |

| 1 hour | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-20 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite