|

|

|

|

|||||

|

|

|

Constellation Brands, Inc. STZ is scheduled to release second-quarter fiscal 2026 results on Oct. 6, 2025. The alcoholic beverage bigwig is expected to have recorded a decline in its top and bottom lines in the to-be-reported quarter.

The Zacks Consensus Estimate for the company’s fiscal second-quarter earnings is pegged at $3.37 per share, indicating a 21.9% decline from the year-ago quarter’s actual. The consensus mark has moved down 16.4% in the past 30 days. The consensus estimate for revenues is pegged at $2.5 billion, indicating a 15.8% decline from the prior-year quarter’s reported figure.

In the last reported quarter, the alcohol behemoth delivered a negative earnings surprise of 3.6%. Its bottom line beat estimates by 3.6%, on average, in the trailing four quarters.

Our proven model does not conclusively predict an earnings beat for Constellation Brands this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that is not the case here. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

Constellation Brands currently has an Earnings ESP of 0.0% and a Zacks Rank #5 (Strong Sell).

Constellation Brands’ beer portfolio remains the central growth driver, with Modelo, Corona and Pacifico sustaining strong brand health despite industry-wide softness. Management reaffirmed its beer revenue and margin outlook, supported by consumer loyalty — particularly among Hispanic buyers — and easier year-over-year comparisons heading into the summer. Innovation and premiumization through products like Oro, Sunbrew and Cheladas continue to attract younger demographics and broaden the brand base. These factors are expected to help offset softer industry depletion trends seen earlier in the year.

The wine and spirits business, which returned to growth at the end of fiscal 2025, is expected to contribute modestly through improved shipment volumes and international expansion, particularly in Canada. While management highlighted the beer business as the main engine, continued diversification through innovation in adjacent categories, including non-alcoholic beverages and RTD products, should support incremental top-line growth. Distribution gains and favorable price-pack architecture are also expected to bolster performance in the near term.

At the operational level, cost-saving initiatives and capacity expansions in Mexico remain critical. Management noted efficiency gains and highlighted premiumization momentum in traditional beers and flavored extensions. However, upcoming tariffs on aluminum are expected to create a $20 million headwind this fiscal year, equivalent to a 20 basis point margin drag. Elevated marketing spend, especially around live sports and seasonal promotions, reflects the company’s push to protect share and brand loyalty in a competitive landscape.

Finally, external pressures remain a key variable. Consumer caution amid inflation and slower discretionary spending continues to weigh on beer occasions, particularly for Hispanic households. Macroeconomic uncertainty, potential tariff shifts and regional factors, such as California’s mixed recovery following last year’s wildfires, could influence the results. While management remains confident in its full-year guidance, these headwinds are likely to continue pressuring margins in the to-be-reported quarter.

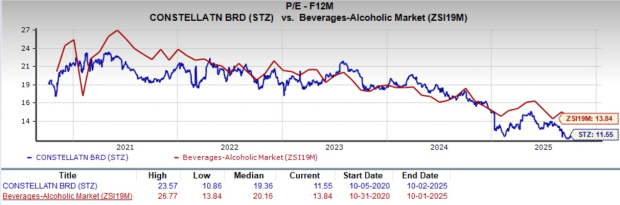

From a valuation perspective, Constellation Brands offers an attractive opportunity, trading at a discount relative to historical and industry benchmarks. With a forward 12-month price-to-earnings ratio of 11.55X, which is below the five-year high of 23.57X and the Beverages - Alcohol industry’s average of 13.84X, the stock offers compelling value for investors seeking exposure to the alcohol beverages space.

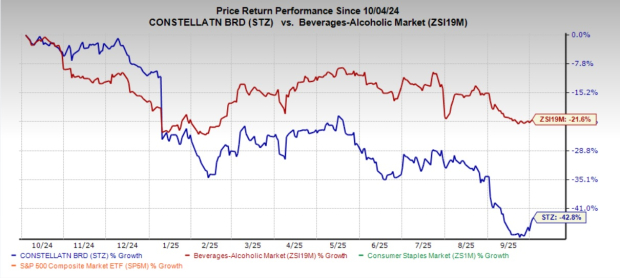

The recent market movements show that STZ shares have lost 42.8% in the past year compared with the industry's 21.6% decline.

Here are some companies, which, according to our model, have the right combination of elements to post an earnings beat this time around:

PepsiCo, Inc. PEP presently has an Earnings ESP of +0.49% and a Zacks Rank of 2. The company is expected to register top-line growth when it reports third-quarter 2025 results. The Zacks Consensus Estimate for quarterly revenues is pegged at $23.9 billion, which indicates a rise of 2.4% from the figure reported in the prior-year quarter. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for quarterly earnings has moved up by a penny in the past seven days. The consensus mark for PEP’s earnings indicates a decline of 1.7% from the year-ago quarter’s number. PEP delivered an earnings surprise of 1.01%, on average, in the trailing four quarters.

Celsius Holdings, Inc. CELH currently has an Earnings ESP of +5.88% and a Zacks Rank of 1. The Zacks Consensus Estimate for third-quarter 2025 EPS is pegged at 26 cents, which implies an increase from break-even earnings in the year-ago quarter. The consensus mark has moved down by a penny in the past 30 days.

The consensus mark for Celsius Holdings’ quarterly revenues is pegged at $699 million, which indicates growth of 163.2% from the figure reported in the prior-year quarter. CELH delivered a trailing four-quarter earnings surprise of 4.8%, on average.

Ollie's Bargain Outlet Holdings, Inc. OLLI currently has an Earnings ESP of +0.24% and a Zacks Rank of 2. The company is expected to register growth in its top and bottom lines when it reports third-quarter 2025 results. The Zacks Consensus Estimate for OLLI’s quarterly earnings has been unchanged in the past 30 days at 71 cents per share. The consensus estimate for earnings indicates 22.4% growth from the year-ago quarter's number.

The Zacks Consensus Estimate for Ollie’s quarterly revenues is pegged at $615.2 billion, implying a rise of 18.9% from the figure reported in the prior-year quarter. OLLI delivered an earnings surprise of 4.2%, on average, in the trailing four quarters.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-13 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-11 | |

| Mar-11 | |

| Mar-11 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite