|

|

|

|

|||||

|

|

|

Lyft LYFT shares are among the cheaper ones in the Zacks Internet Services industry.

The company currently has a Value Score of B.

LYFT stock trades at a discount with a forward 12-month P/S of 1.22X compared with the industry’s 6.44X. Its valuation is cheaper than that of rival Uber Technologies UBER and fellow industry player DoorDash DASH. Uber Technologies and DoorDash currently have a Value Score of D and F, respectively.

Now, the question is whether it is worth buying the stock at the current price. Let us dig deeper to find out.

Gross Booking Growth: Lyft is benefiting from increased gross bookings. Gross bookings are improving mainly due to a growing active rider base, expansion into new markets and the success of the company’s customer-friendly "Price Lock" feature.

In the June quarter, gross bookings increased 12% year over year to $4.5 billion. This was the 17th consecutive quarter where Lyft demonstrated double-digit year-over-year growth in the key metric, demonstrating the resilience and momentum of the company’s customer-friendly strategy. For the third quarter of 2025, it expects gross bookings in the $4.65-$4.8 billion range, indicating 13-17% growth from the third-quarter 2024 actuals.

Price Lock Feature Performing Well: LYFT’s move to focus on less densely populated markets, such as Indianapolis, is paying off. Its Price Lock feature is also doing well. With the return-to-office mode gaining steam, there is a surge in weekday demand for ride-hailing services. To compete more effectively with rivals in the ride-hailing arena, Lyft has introduced a Price Lock feature. This feature allows users to bypass surge pricing during peak commuting hours. By locking in a commute price, they can save money. LYFT, like Uber, aims to establish a strong foothold in the highly promising robotaxi market through strategic partnerships.

Share Buyback Boost: Another area of confidence is LYFT’s buyback strategy. In a shareholder-friendly move, management announced earlier in the year an increase in its share repurchase program to $750 million from $500 million. In the second quarter of 2025, LYFT repurchased $200 million worth of stock. Strong cash flow generation allows it to remain committed to returning value to shareholders. LYFT’s cash flow generation was $993 million in the trailing 12 months at the end of the second quarter of 2025.

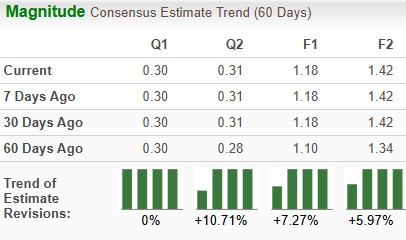

Zacks Estimates Northbound: The Zacks Consensus Estimate for LYFT’s 2025 and 2026 sales implies a year-over-year increase of 12.8% and 14.3%, respectively. The consensus mark for LYFT’s 2025 EPS and 2026 indicates a 24.2% and 19.9% year-over-year uptick, respectively. Moreover, the EPS estimates for fourth-quarter 2025, full-year 2025 and 2026 have been trending northward over the past 60 days.

Tariff Tensions Weighing on LYFT Stock: Concerns about the ongoing trade war are hurting Lyft’s prospects. Recently, U.S. markets have been marked by high volatility amid uncertainty surrounding the nation’s trade policy and growing concerns about a slowing economy. Fears of a slowdown in the economy are detrimental to LYFT, whose health is tied to that of the broader economy. This trade war is expected to result in a further increase in volatility and uncertainty going forward.

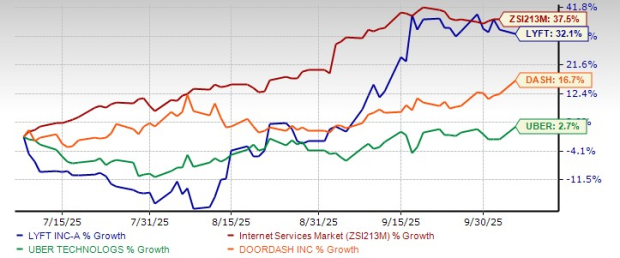

Due to this uncertainty, LYFT stock has underperformed its industry over the past three months. Lyft’s performance is, however, better than that of Uber and DoorDash.

Unimpressive Earnings History: Lyft missed the Zacks Consensus Estimate for earnings in two of the last four quarters, while beating the mark in the other two.

Lyft, Inc. price-eps-surprise | Lyft, Inc. Quote

LYFT’s High Debt Load is a Concern: We are also concerned about LYFT’s high debt levels, despite efforts to reduce them. The company’s times interest earned ratio was 4.9 at the end of the second quarter 2025, much lower than industrial levels. A lower times interest earned ratio often means that a company faces a greater risk of defaulting on its debt obligations. This implies serious financial problems.

Agreed that LYFT’s valuation is tempting, and it is likely to continue benefiting from strong gross bookings. Lyft’s ambitions to be a key player in the lucrative and emerging autonomous vehicle market also bode well. Lyft has inked quite a few deals in this respect. By adopting this approach, LYFT has avoided massive R&D costs associated with developing autonomous systems independently.

However, headwinds such as escalating debt and tariff-related uncertainty cannot be ignored. We believe that despite the tailwinds, it is still not an opportune time to buy this Zacks Rank #3 (Hold) stock. Investors should monitor the company’s developments closely for an appropriate entry point. For those who already own the stock, it will be prudent to stay invested.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour |

GoTo Foods announces former Roark Capital executive Brett Ubl as new CFO

UBER

Nation's Restaurant News

|

| 3 hours | |

| 4 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

New Uber-Joby Aviation Partnership To Bring Ride Sharing To The Skies

UBER

Investor's Business Daily

|

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite